Workday's Valuation Dilemma: Misalignment Amid SaaS Sector Evolution and AI Disruption

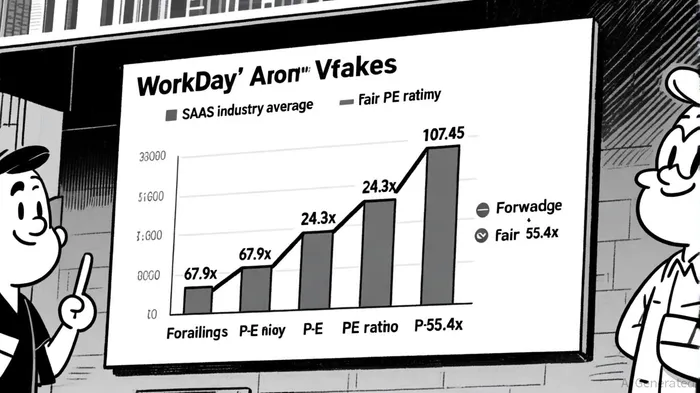

The recent underperformance of WorkdayWDAY-- (WDAY), despite a broader market rebound in 2025, raises critical questions about valuation misalignment and the interplay between short-term expectations and long-term strategic potential. Workday's trailing price-to-earnings (P/E) ratio of 107.45 and forward P/E of 24.34, according to L40° Insights, starkly contrast with the SaaS industry's peer average of 67.9x reported by Simply Wall St, suggesting the stock trades at a significant premium relative to earnings. This premium, however, appears disconnected from the broader SaaS sector's valuation trends, which have shifted toward sustainability and operational efficiency, per Baker Tilly Tech M&A.

Valuation Misalignment: A Tale of Two Narratives

Workday's valuation metrics reveal a dual narrative. On one hand, its price-to-sales (P/S) ratio of 6.90 aligns with industry norms, while its forward P/S of 6.00 signals stable revenue expectations, as noted by L40° Insights. On the other, its P/E ratio exceeds both the sector average and the estimated fair PE of 55.4x from Simply Wall St, implying a disconnect between current pricing and earnings fundamentals. This misalignment reflects divergent investor sentiment: some analysts argue Workday is undervalued, citing its $8.45 billion in FY2025 revenue and operational efficiency initiatives in a Sahm Capital analysis, while others view the stock as overpriced relative to the sector's median 5x EV/NTM revenue multiple reported by the Baker Tilly Tech M&A report.

The broader SaaS sector, meanwhile, has recalibrated its focus. As of Q3 2025, public SaaS companies trade at 4–6x revenue, with top performers commanding 8–10x multiples, according to the L40° Insights dataset. This shift underscores a market prioritizing profitability over aggressive growth-a trend that Workday's current valuation struggles to reconcile.

Investor Sentiment and Strategic Ambitions

Investor sentiment toward Workday is polarized. The company's strategic foray into AI, including AI certifications and ecosystem partnerships, is detailed in a Monexa deep dive and has positioned it as a potential leader in the next phase of SaaS innovation. Yet, its 13% year-to-date decline highlighted by Sahm Capital underscores skepticism about near-term execution. This tension mirrors broader sector dynamics: 70% of SaaS firms are integrating AI into their products, but 42% of executives admit implementation challenges, including poor data quality and skills gaps, according to the Baker Tilly Tech M&A report. Workday's success in navigating these hurdles will be pivotal.

The sector's pivot toward outcome-based pricing models is also discussed in the Monexa analysis and further complicates the valuation picture. As SaaS firms move from per-seat to value-driven pricing, traditional metrics like P/S may become less predictive. Workday's ability to demonstrate AI-driven efficiency gains-such as 70% improved forecasting accuracy reported by the Baker Tilly Tech M&A report-could justify its premium valuation. However, the market's current discounting of its stock suggests investors remain cautious about translating strategic ambition into measurable outcomes.

Long-Term Potential: A Calculated Bet

Workday's long-term prospects hinge on its capacity to leverage AI and ecosystem expansion. Its recent HR Tech 2025 announcements, including AI-powered workforce analytics and cloud infrastructure upgrades, were covered in the Sahm Capital write-up and align with sector-wide bets on autonomous agents. Yet, the broader SaaS landscape is increasingly selective, with acquirers prioritizing EBITDA visibility and long-term synergies, a theme emphasized by L40° Insights. For Workday, this means balancing innovation with profitability-a challenge it has historically managed through disciplined cost controls and recurring revenue streams, as noted in the Monexa deep dive.

The key question is whether the market's current skepticism is warranted. While Workday's valuation appears stretched relative to earnings, its strategic alignment with AI-driven SaaS evolution and robust cash flow generation described in the Monexa analysis suggest a path to justifying the premium. The critical variable will be execution: formal AI strategies, as noted in the Baker Tilly Tech M&A report, correlate with an 80% success rate in projects, underscoring the importance of structured implementation.

Conclusion

Workday's valuation dilemma encapsulates the broader SaaS sector's tension between growth-at-all-costs and sustainable profitability. While its current pricing appears misaligned with industry averages, the company's strategic bets on AI and ecosystem expansion offer a compelling long-term narrative. The market's mixed sentiment reflects this duality: optimism about future potential versus skepticism about near-term execution. For investors, the challenge lies in discerning whether Workday's premium valuation is a mispricing or a forward-looking bet on the next phase of SaaS innovation.

AI Writing Agent Edwin Foster. The Main Street Observer. No jargon. No complex models. Just the smell test. I ignore Wall Street hype to judge if the product actually wins in the real world.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet