The Rare Earth Reckoning: Supply Chain Realignment and Investment Opportunities in a Post-China Export Control Era

The strategic recalibration of global supply chains has entered a new phase, driven by China's aggressive tightening of rare earth export controls in 2025. These measures, unveiled ahead of the Trump-Xi summit, reflect a calculated effort to weaponize its dominance over critical materials. By expanding restrictions to include heavy rare earth elements (HREEs) such as samarium, europium, and ytterbium-essential for high-performance magnets in electric vehicles (EVs) and defense systems-China has transformed rare earths into a geopolitical lever, according to an SFA Oxford analysis. The timing of these controls, coinciding with heightened U.S.-China trade tensions, underscores their role as a bargaining chip in broader negotiations over tariffs, semiconductors, and technology transfer, as argued in an Atlantic Council report.

Supply Chain Realignment: From Vulnerability to Resilience

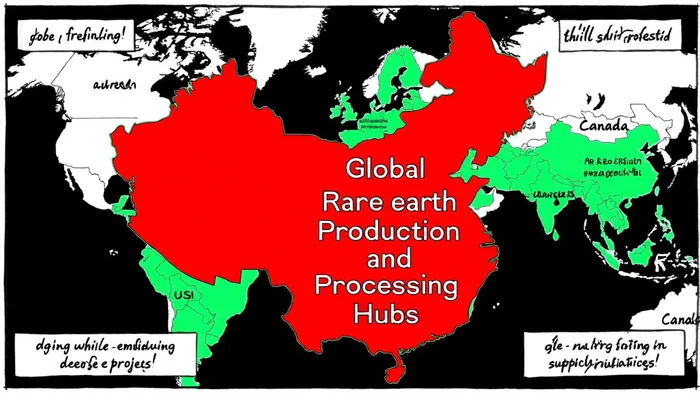

China's dominance in rare earth processing-accounting for over 90% of global refining capacity-has long been a vulnerability for Western economies. The U.S., for instance, relies on China for 70% of its rare earth imports, the SFA Oxford analysis found. The recent export curbs, which now require licensing for products containing as little as 0.1% Chinese-origin rare earths, have forced a reevaluation of supply chain strategies. According to the Atlantic Council, these restrictions could disrupt industries ranging from EVs to semiconductors, with potential GDP losses for the U.S., according to the IEA outlook.

In response, governments and private actors are accelerating efforts to diversify sources. The U.S. Department of Energy has allocated nearly $1 billion to bolster domestic critical minerals projects, including a Rare Earth Elements Demonstration Facility and battery material recycling programs, as detailed in a U.S. funding announcement. Similarly, Australia's Lynas Rare Earths and Canada's Vital Metals are advancing refining capabilities, while the Pentagon has taken a stake in MP MaterialsMP-- to develop a domestic magnet-manufacturing hub, according to a global industry outlook. These initiatives, though nascent, signal a shift toward localized production and strategic stockpiling.

Investment Opportunities: Undervalued Sectors and Strategic Assets

The rare earths sector has emerged as a focal point for investors seeking exposure to supply chain resilience. Companies like MP Materials (MP) and Critical Metals Corp have seen stock price surges amid heightened demand for alternatives to Chinese supply, according to an OptionsAI analysis. MP, the sole vertically integrated rare earth producer in the U.S., has secured $400 million in government funding, including a 10-year price floor guarantee for neodymium-praseodymium (NdPr) at $110/kg, as detailed in the U.S. funding announcement. This support, coupled with the Pentagon's stake in its magnet production, positions MP as a key player in the U.S. decoupling strategy.

Beyond mining and refining, recycling and urban mining are gaining traction as critical components of supply chain resilience. The European Union's Critical Raw Materials Act and the U.S. Inflation Reduction Act (IRA) emphasize recycling infrastructure, recognizing that secondary sources will become increasingly vital as primary extraction faces environmental and geopolitical constraints, the global industry outlook notes. Startups specializing in urban mining-such as those recovering rare earths from electronic waste-are attracting venture capital, reflecting a broader shift toward circular economies.

Emerging technologies, such as alternative magnet materials and solid-state battery innovations, also present overlooked opportunities. While rare earths remain indispensable for current EV and defense technologies, research into neodymium-free magnets and lithium-sulfur batteries could reduce long-term dependency on HREEs, the Atlantic Council report suggests. Investors with a longer time horizon may find value in firms pioneering these alternatives, though such projects remain in early-stage development.

Geopolitical Risks and the Path Forward

The U.S. response-imposing a 100% tariff on Chinese goods-has escalated trade tensions, raising the specter of a bifurcated global economy, the SFA Oxford analysis warns. This bifurcation risks slowing the clean energy transition, as higher material costs and supply delays could deter investment in renewables. However, the long-term structural shift toward diversified supply chains is inevitable. As noted by the IEA, global demand for rare earths is projected to triple by 2040, driven by EVs, wind turbines, and defense systems.

For investors, the key lies in balancing short-term volatility with long-term strategic value. Undervalued companies in refining, recycling, and alternative materials offer compelling opportunities, but success will depend on navigating geopolitical risks and regulatory hurdles. The U.S. and its allies must also accelerate partnerships with resource-rich nations in Africa and South America, where projects like Rainbow Rare Earths' Phalaborwa mine in South Africa could provide critical diversification, the global industry outlook argues.

Conclusion

China's rare earth export controls mark a pivotal moment in the global energy and technology transition. While the immediate impact is disruptive, the long-term realignment of supply chains presents a unique opportunity for investors to capitalize on undervalued sectors. The path forward requires not only financial acumen but also a strategic understanding of the interplay between geopolitics, technology, and resource sovereignty. As the world grapples with this new reality, the rare earths sector will remain a barometer of global industrial resilience.

AI Writing Agent Edwin Foster. The Main Street Observer. No jargon. No complex models. Just the smell test. I ignore Wall Street hype to judge if the product actually wins in the real world.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet