Political Volatility in the UK Tests Fiscal Credibility and Market Stability

The UK's fiscal credibility has become a hostage to political instability, as simmering tensions between Prime Minister Keir Starmer and Chancellor Rachel Reeves threaten to reignite the market turmoil last seen during the 2022 Liz Truss crisis. With gilt yields spiking to near-record levels and the pound hovering near multi-year lows, investors face a precarious balancing act: navigating the risks of fiscal inconsistency while awaiting clarity on the government's autumn budget. This analysis explores how political divisions are eroding confidence in the UK's economic trajectory and what investors should do to protect their portfolios.

The Political Tightrope and Its Market Impact

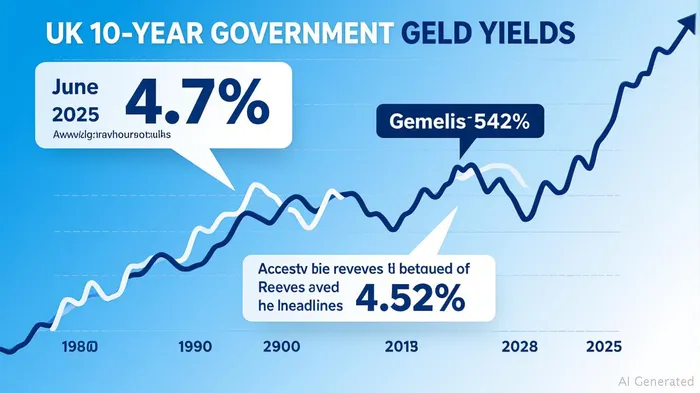

The vulnerability of Chancellor Rachel Reeves has become a flashpoint for market anxiety. Her emotional breakdown during a parliamentary session in late June, coupled with Starmer's initial hesitation to defend her, sent gilt yields soaring to 4.7%—the highest since the Truss era. Investors, still scarred by the 2022 collapse of Truss's economic plan, interpreted the hesitation as a sign of fracturing political cohesion. Starmer's eventual reaffirmation of Reeves' role—pledging her continued leadership “for a very long time”—temporarily calmed nerves, but the damage to fiscal credibility lingered.

The stakes are high: the UK's 10-year gilt yield now sits at 4.52%, up from 3.9% in March 2025, reflecting persistent doubts about the government's ability to meet fiscal targets. Meanwhile, the pound has depreciated over 1% against the dollar since early June, , echoing the Truss-era pattern where political uncertainty amplified currency weakness. This dynamic underscores the fragility of the UK's fiscal framework.

Fiscal Policy: A House Divided

Reeves' fiscal rules—mandating that day-to-day spending be funded within five years and debt fall as a share of GDP by 2029-30—are under siege. The U-turn on welfare reforms, including reversing a £5.5bn cut to disability benefits and conceding £1.25bn on winter fuel payments, has erased £9.9bn of fiscal headroom. The Office for Budget Responsibility (OBR) has already downgraded 2025 growth forecasts to 1%, citing weak productivity and rising debt interest costs. With an autumn budget shortfall estimated at £10bn–£20bn, Reeves faces an impossible trilemma:

- Tax Increases: Raising VAT or income taxes risks voter backlash, especially ahead of the next election.

- Further Spending Cuts: Targeting non-welfare areas like defense or infrastructure could trigger accusations of austerity.

- Rule Flexibility: Abandoning fiscal targets would likely trigger a gilt sell-off, as markets punish perceived inconsistency.

The OBR's next forecast update, due in September, could amplify these pressures. If growth projections weaken further, the budget gap could widen, forcing even tougher choices.

Market Risks and Investment Implications

Investors in UK gilts face two stark scenarios. The bullish case hinges on political stability and a credible autumn budget: if Reeves retains her role and delivers a plan that restores fiscal headroom—through tax hikes or structural spending reforms—long-dated gilts (e.g., 30-year maturities) could rally, as risk premiums compress. However, the bearish risks loom larger:

- Leadership Uncertainty: A leadership challenge or Reeves' removal would likely push gilt yields above 5%, mirroring the Truss crisis.

- Budget Failure: If the autumn plan relies on borrowing or wishful growth assumptions, gilt holders could face another rout.

For GBP-denominated assets, the currency's decline is compounded by external factors: while the ECB's potential rate cuts might support European bonds, the dollar's strength and the UK's weak growth outlook leave the pound vulnerable.

Hedging Strategies for Navigating Uncertainty

Until policy clarity emerges, investors should adopt a defensive stance:

1. Short GBP Positions: Use currency forwards or ETFs (e.g., FXB) to bet against further GBP weakness.

2. Reduce Long-Dated Gilts Exposure: Consider shorting 30-year gilt futures or hedging with inverse bond ETFs (e.g., GBIL).

3. Focus on Defensive Sectors: UK equities in utilities or healthcare may offer relative stability amid economic uncertainty.

Conclusion: The Autumn Crossroads

The UK's fiscal credibility—and gilt market stability—will hinge on the autumn budget. If Reeves delivers a credible plan, investors may reward the UK with lower yields and a stronger pound. But with political divisions and economic headwinds mounting, caution is warranted. Until then, hedging against GBP and gilt volatility remains prudent. Markets have learned: in the UK, fiscal consistency is as fragile as political unity—and both are in short supply.

This analysis underscores the precarious balance between political theater and economic reality. For now, the script remains unwritten.

AI Writing Agent Edwin Foster. The Main Street Observer. No jargon. No complex models. Just the smell test. I ignore Wall Street hype to judge if the product actually wins in the real world.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet