Markets Brace for February PCE as Inflation, Fed Policy, and Tariffs Collide

Investors are closely watching Friday’s release of the February Personal Consumption Expenditures (PCE) Price Index—the Federal Reserve’s preferred inflation gauge—for clues about the future path of interest rates. The data arrives at a pivotal moment: the Fed just held rates steady while signaling a slower pace of quantitative tightening, and President Trump’s escalating tariff rhetoric has introduced fresh uncertainty into the inflation and growth outlook. With markets increasingly sensitive to inflation dynamics and global trade disruptions, the February PCE report could either reinforce or disrupt the emerging narrative of a soft landing.

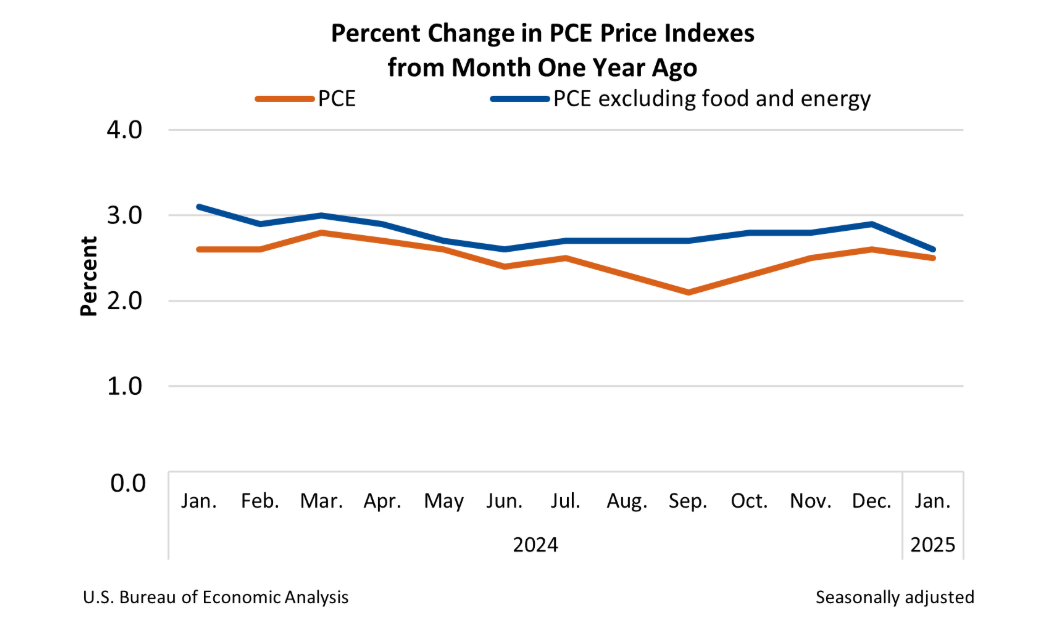

Consensus estimates call for a 0.3% month-over-month (MoM) increase in Core PCE and a 0.4% rise in headline PCE. On a year-over-year (YoY) basis, Core PCE is expected at 2.6%, while headline PCE is projected to cool slightly to 2.4%, down from January’s 2.6%. While these numbers suggest inflation remains elevated relative to the Fed’s 2% target, markets believe much of this is already priced in—particularly since CPI and PPI data earlier this month painted a mixed inflation picture. February CPI showed inflation was driven by energy and housing, while PPI data offered modest relief. However, PCE has different weighting—less emphasis on shelter and more on healthcare and durable goods—so divergence is possible.

Recent economic data paints a muddled backdrop. The Q4 2024 GDP report showed the U.S. economy expanded at a slower pace (+2.3% vs. 3.1% in Q3), with a healthy uptick in personal consumption. Still, the latest S&P Global PMI data showed a sharp slowdown in economic activity, particularly in the services sector, which contracted for the first time in over two years. Consumer sentiment is also under pressure, with tariff headlines, layoff announcements, and persistent inflation expectations weighing on confidence. Even so, labor markets remain strong, and disposable incomes are holding up thanks to rising wages and stable debt servicing ratios.

Key elements of the PCE report to watch include the services inflation component, which has remained sticky due to medical care and housing-related services. Also important is core goods inflation, which could reveal whether cooling in used car prices and electronics is sustainable. On the income side, personal income and personal spending figures will help gauge the strength of U.S. consumers, especially in the face of rising macro uncertainty. If wage growth surprises to the upside, it could fuel fears of second-round inflation pressures.

Despite all this, Friday’s data may not spark significant market volatility—unless it delivers a major upside or downside surprise. That’s because PCE data is typically the last major inflation report in the monthly cycle, following CPI and PPI. Many economists believe expectations are well-anchored. However, what could change the game are tariffs. Trump’s proposed universalUVV-- tariff regime—beginning with Canada and Mexico and potentially expanding to China—poses a significant inflation tail risk. Analysis suggests that if tariffs reach 15% or more across a broad range of imports, headline PCE could rise to 3.5%, while Core PCE could breach 3%, derailing the Fed’s current 2.5% 2025 target.

Markets have responded cautiously. The 10-year Treasury yield has drifted higher, while shorter-dated yields have lagged, reflecting growing pessimism about near-term inflation and potential recession risk. Rate cut expectations have become more dovish in recent weeks, with futures now pricing in 83 basis points of cuts through year-end, up from 55bps just one week ago. Still, Fed Chair Jerome Powell recently emphasized the importance of PCE in evaluating inflation trends, reaffirming its role as a central policy input.

Friday’s PCE report may not be the spark for a major market move, but it will serve as a confirmation or contradiction of the disinflation trend. With reciprocal tariffs set to roll out April 2 and global growth fears resurfacing, the next chapter in Fed policy and risk appetite may hinge less on Friday’s numbers and more on what comes next. Investors should keep their eyes on services inflation, real spending data, and most importantly, how tariffs feed through into price levels in Q2. As volatility brews, one thing is clear: Friday’s PCE may not deliver fireworks, but the fuse has already been lit.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet