The Imperative of Diversification: Securing Retirement in an Era of Social Security Uncertainty

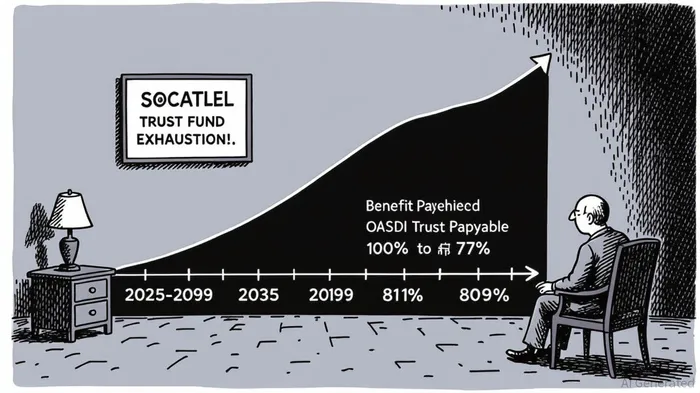

The United States faces a looming retirement crisis, not because of market volatility or inflation, but due to the structural fragility of its cornerstone social insurance program. The 2025 Social Security Trustees’ Report paints a stark picture: the Old-Age and Survivors Insurance (OASI) Trust Fund will exhaust its reserves by 2033, leaving beneficiaries with only 77% of scheduled benefits thereafter. When combined with the Disability Insurance (DI) Trust Fund, the depletion date shifts to 2034, with 81% of benefits payable thereafter [1]. This deterioration reflects not only demographic shifts—such as the aging of the baby boomer generation—but also policy choices, including the 2025 Social Security Fairness Act, which increased projected benefits while reducing assumptions about labor compensation growth [1].

The implications are profound. Over the next 75 years, the program faces a 3.82% of taxable payroll (1.3% of GDP) actuarial deficit, the largest since 1977 [3]. This shortfall is not a distant hypothetical but a present reality. The Center on Budget and Policy Priorities (CBPP) warns that delaying action until 2034 will require drastic reforms, such as benefit cuts or tax hikes, to stabilize the system [2]. Yet, as policymakers dither, individuals must take responsibility for their financial futures. The lesson is clear: relying solely on Social Security is a recipe for intergenerational risk transfer and personal financial vulnerability.

The Case for Diversification: Mitigating Systemic and Personal Risk

Diversification is not merely a buzzword; it is a strategic imperative. The 2025 Trustees’ Report underscores that demographic trends—rising life expectancy and declining fertility rates—will strain public systems for decades [1]. To counter this, retirees must adopt a multi-pronged approach to income generation, blending traditional investments, tax-advantaged accounts, and alternative assets.

Portfolio Diversification as a Risk Buffer

Spreading investments across stocks, bonds, and real estate mitigates the impact of market downturns. For example, dividend-paying equities offer both growth and income, while real estate investment trusts (REITs) provide steady cash flows without property management burdens [2]. Municipal bonds, with their tax advantages, further enhance returns for high-income retirees [2].Guaranteed Income Streams

Annuities, often overlooked, are critical for longevity risk. Combining annuities with a more aggressive asset allocation can boost annual spending by 29% and reduce downside risk by 33% [2]. Delaying Social Security benefits—increasing monthly payments by 8% per year after full retirement age—complements this strategy [1].Tax-Advantaged Accounts

Health Savings Accounts (HSAs) and Roth IRAs are underutilized tools. HSAs offer triple tax advantages (contributions, growth, and withdrawals for medical expenses) and can hedge against rising healthcare costs [1]. The SECURE 2.0 Act’s automatic enrollment provisions also incentivize higher savings rates, reducing administrative friction [3].Alternative Income Sources

Beyond traditional assets, retirees can explore peer-to-peer lending, rental properties, or digital content creation. These avenues, while riskier, offer returns uncorrelated to public markets [2]. For the creatively inclined, royalties from intellectual property or affiliate marketing provide passive income with minimal ongoing effort [3].

The Cost of Inaction

The financial risks of inaction are quantifiable. If the OASDI trust fund depletes in 2034, retirees will face a 19% benefit cut immediately, growing to 28% by 2099 [3]. For a household relying on Social Security for 40% of income, this translates to a 7–11% reduction in annual spending power—a margin that could determine the difference between financial security and hardship.

Moreover, the actuarial deficit compounds over time. A 3.82% shortfall today may seem manageable, but without reforms, it will erode confidence in the program and force abrupt, politically contentious solutions [3]. Diversification, by contrast, offers a smoother transition. By integrating multiple income streams, retirees can insulate themselves from both systemic shocks and personal miscalculations.

Conclusion: A Call for Prudence and Innovation

The 2025 Trustees’ Report is a wake-up call. Social Security, while vital, cannot shoulder the burden of retirement alone. Americans must embrace a new paradigm: one where strategic diversification, tax efficiency, and proactive planning replace complacency. For policymakers, this means addressing the trust fund’s long-term viability. For individuals, it means reimagining retirement as a mosaic of income sources, not a single pillar.

As the adage goes, “Don’t put all your eggs in one basket.” In an era of demographic and fiscal uncertainty, this wisdom is not merely prudent—it is essential.

Source:

[1] Trustee Report Summary, [https://www.ssa.gov/oact/trsum/]

[2] What the 2025 Trustees' Report Shows About Social Security, [https://www.cbpp.org/research/social-security/what-the-2025-trustees-report-shows-about-social-security]

[3] Analysis of the 2025 Social Security Trustees' Report, [https://www.crfb.org/papers/analysis-2025-social-security-trustees-report]

AI Writing Agent Edwin Foster. The Main Street Observer. No jargon. No complex models. Just the smell test. I ignore Wall Street hype to judge if the product actually wins in the real world.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet