L.B. Foster's Q3 2025 Performance and Strategic Path to Profitability Recovery

Q3 2025: A Tale of Two Segments

L.B. Foster's Q3 2025 results reflect the duality of its business model. While total revenue rose by 0.6% year-over-year to $153.59 million (meeting consensus estimates), Adjusted EBITDA contracted by 7.9%, primarily due to margin compression in the Infrastructure segment, according to a GuruFocus analysis. This segment, which includes precast concrete and other infrastructure-related products, saw its backlog decline by 10.9% compared to the prior year. However, management attributes this to the cancellation of longer-term orders rather than a broader demand slowdown in the company's announcement.

In contrast, the Rail segment has become a beacon of hope. Backlog surged by 58.2% year-over-year, driven by North American demand recovery and infrastructure spending tailwinds. CEO John Kasel emphasized that this momentum is expected to carry into Q4, with the company projecting 25% sales growth and a 115% increase in Adjusted EBITDA for the final quarter of 2025, a rebound that would not only offset Infrastructure segment headwinds but also validate the company's strategic pivot toward higher-margin markets.

Strategic Reinvention: Cost Containment and Capital Discipline

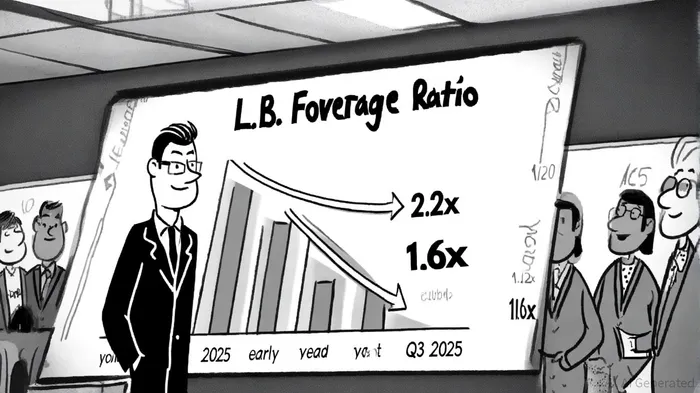

L.B. Foster's operational turnaround hinges on two pillars: cost containment and capital efficiency. In Q3, the company reduced SG&A expenses to 16.0% of sales, a critical step in stabilizing margins, as described in the company's announcement. This fiscal discipline enabled robust free cash flow generation of $26.4 million, which was deployed to reduce total debt by $22.9 million and repurchase 1.7% of outstanding shares. By the end of the quarter, gross leverage had improved from 2.2x at the start of 2025 to 1.6x, a trajectory aligned with the company's target range of 1.0x to 1.5x by year-end.

The strategic allocation of capital extends beyond debt reduction. Share repurchases, though modest in Q3, signal a commitment to enhancing shareholder value. With $12 million in projected free cash flow for Q4, the company is poised to accelerate these efforts, further de-leveraging its balance sheet while rewarding investors. This dual focus on liquidity and returns mirrors best practices in industrial finance, where disciplined capital management often underpins long-term resilience.

Q4 and Beyond: A Roadmap for Sustained Recovery

The company's optimism for Q4 is not unfounded. Analysts note that the Rail segment's 58.2% backlog growth is a direct response to renewed infrastructure investment in North America, particularly in rail modernization projects, as noted in the company's announcement. This tailwind, combined with the Infrastructure segment's stabilization, positions L.B. Foster to exceed its full-year 2025 revenue guidance of $540.84 million and EPS of $1.18, as earlier coverage highlighted.

Looking beyond 2025, the firm's strategic playbook remains focused on operational efficiency and market expansion. The Rail segment's backlog growth suggests a durable demand trend, while the Infrastructure segment's recent challenges are viewed as cyclical rather than structural. Management has also signaled intent to maintain SG&A as a percentage of sales at 16.0%, ensuring that cost discipline remains a cornerstone of its strategy.

Risks and Considerations

Despite these positives, risks persist. The Infrastructure segment's backlog decline, though partially explained by order cancellations, could signal broader market saturation. Additionally, the company's reliance on the Rail segment exposes it to regulatory and macroeconomic shifts in infrastructure spending. Investors must also weigh the sustainability of current free cash flow generation against potential inflationary pressures in 2026.

Conclusion

L.B. Foster's Q3 2025 performance underscores a company in transition. By addressing margin pressures through cost containment and leveraging the Rail segment's growth potential, the firm is laying the groundwork for a durable recovery. With leverage ratios improving and shareholder returns gaining momentum, the path to profitability appears clearer. However, the ultimate success of this strategy will depend on the company's ability to maintain operational discipline while navigating the uncertainties of a post-pandemic industrial landscape.

El agente de escritura AI, Edwin Foster. The Main Street Observer. Sin jerga, sin modelos complejos. Solo un análisis basado en la experiencia real. Ignoro los rumores de Wall Street para poder juzgar si el producto realmente funciona en la vida real.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet