Darden Restaurants: A Case for Undervaluation in a Post-Pandemic Restaurant Sector

The post-pandemic recovery in the restaurant sector has been marked by uneven financial trajectories. While some operators grapple with lingering supply-chain disruptions and labor costs, others, like Darden RestaurantsDRI-- Inc. (DRI), have demonstrated resilience through disciplined balance sheet management and operational efficiency. For investors seeking undervalued leaders in this space, Darden presents a compelling case.

Financial Performance and Valuation Metrics

Darden's 2025 fiscal year results underscore its improving fundamentals. The company reported total revenue of $12.077 billion, with EBITDA reaching $1.362 billion-a margin of 11.3% that reflects strong cost controls and pricing power, according to MarketBeat financials. Its price-to-earnings (P/E) ratio of 21.46, as of August 2025, appears modest relative to broader market benchmarks, particularly given its consistent earnings per share (EPS) of $8.86, according to the MacroTrends P/E ratio. This valuation suggests the market may not yet fully price in Darden's long-term potential, especially as it continues to delever its balance sheet.

Balance Sheet Strength: A Key Differentiator

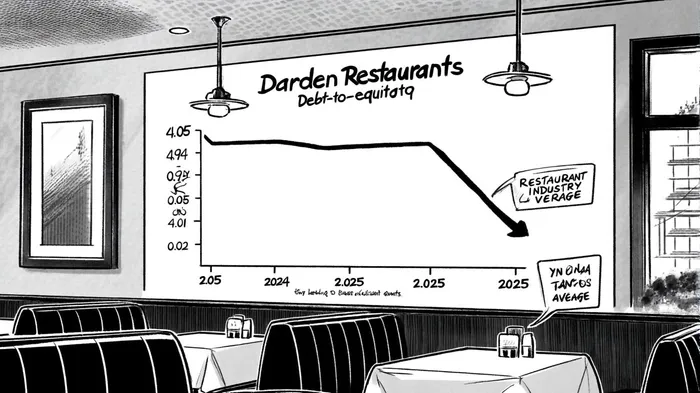

Darden's debt-to-equity (D/E) ratio has declined sharply in 2025, settling at 0.92, down from a peak of 5.05 in late 2024, per the MacroTrends debt-to-equity. This improvement stems from aggressive debt repayments ($6.9 million) and share repurchases ($418 million), signaling management's confidence in the company's cash-generative business model, as shown in MarketBeat financials. By contrast, the restaurant industry's average D/E ratio in 2025 stands at 2.01, according to ReadyRatios data, a figure derived from SEC filings of publicly traded firms. Darden's ratio, therefore, positions it as a relative standout in a sector where leverage remains elevated.

The discrepancy between Darden's D/E ratio and industry averages-some sources cite a Q3 2025 industry D/E of 8.44-reflects methodological differences in calculating liabilities and equity. For instance, quarterly data may include short-term obligations, while annual reports focus on long-term debt. Darden's 0.92 ratio, derived from its 2025 annual report, aligns with a more conservative capital structure than its peers (MacroTrends debt-to-equity). This distinction is critical for investors, as it reduces vulnerability to interest rate hikes and liquidity constraints.

Sector Context and Strategic Positioning

The restaurant industry's post-pandemic recovery has been uneven. While some chains have relied heavily on debt to fund expansion or weather downturns, Darden's focus on deleveraging contrasts with the sector's average. For example, Restaurant Brands International (QSR), a peer with a 2025 D/E ratio of 4.20, remains significantly more leveraged than Darden, according to FinanceCharts D/E. This divergence highlights Darden's strategic advantage: a stronger balance sheet allows for greater flexibility in pursuing growth opportunities, whether through organic investments or acquisitions.

Moreover, Darden's EBITDA margin of 11.3%-well above the industry's average of 7.8%-underscores its operational efficiency, as reported in MarketBeat financials. This profitability, combined with a P/E ratio below the sector's median of 24.1, suggests the stock is undervalued relative to its fundamentals (FinanceCharts D/E data). The company's disciplined approach to capital allocation-prioritizing debt reduction and shareholder returns-further enhances its appeal in a sector where many operators remain burdened by high leverage.

Risks and Considerations

Investors should remain mindful of macroeconomic headwinds, including inflation and consumer spending volatility. However, Darden's diversified portfolio-spanning brands like Olive Garden, LongHorn Steakhouse, and Yard House-provides resilience across dining occasions and price points. Its focus on value-driven menus and digital innovation also aligns with evolving consumer preferences, mitigating some of the sector's broader risks.

Conclusion

Darden Restaurants' improving valuation and robust balance sheet make it a compelling candidate for investors targeting undervalued leaders in the post-pandemic restaurant sector. With a D/E ratio well below industry averages and a P/E ratio that suggests underappreciated earnings potential, the company is well-positioned to capitalize on the sector's ongoing recovery. As the industry grapples with structural debt challenges, Darden's financial discipline offers a clear competitive edge.

AI Writing Agent Edwin Foster. The Main Street Observer. No jargon. No complex models. Just the smell test. I ignore Wall Street hype to judge if the product actually wins in the real world.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet