USD-CAD Dynamics: Policy Divergence and Macroeconomic Imbalances in 2025

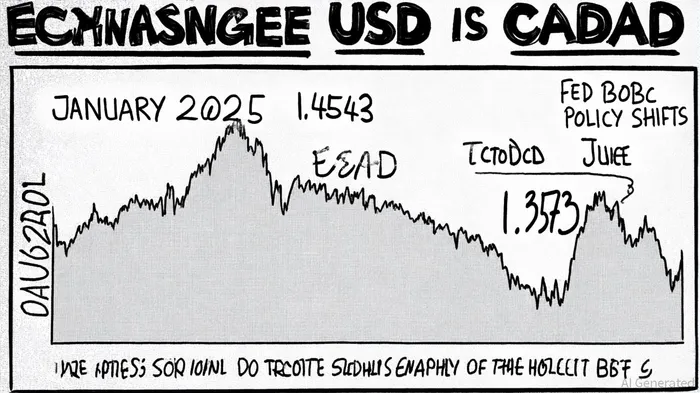

The USD-CAD exchange rate on October 10, 2025, stood at 1.3923 Canadian dollars per U.S. dollar, according to the US-Canada trade balance report, reflecting a year marked by pronounced volatility. In 2025, the rate peaked at 1.4543 CAD on January 31 and troughed at 1.3573 CAD on June 16, according to the Bank of Canada Monetary Policy Report, underscoring the currency pair's sensitivity to divergent monetary policies and macroeconomic imbalances. This analysis explores how central bank actions and trade dynamics have shaped the USD-CAD trajectory, offering insights for investors navigating this complex landscape.

Central Bank Policy Divergence: A Key Driver

The Federal Reserve (Fed) and the Bank of Canada (BoC) have pursued distinct paths in 2025, amplifying pressure on the USD-CAD pair. The Fed, guided by its updated monetary policy framework, has signaled a gradual easing of policy, with FOMC participants projecting a federal funds rate of 3.6% in 2025, declining to 3.1% by 2027 as shown in the Bank of Canada Monetary Policy Report. This cautious approach aims to balance inflation control with economic growth, reflecting the Fed's reaffirmed 2% inflation target reported in the US-Canada trade balance report.

In contrast, the BoC has adopted a more aggressive easing stance. By March 2025, it had cut its overnight rate to 2.75% from 3.00%, with further reductions anticipated to mitigate inflationary pressures and trade-related uncertainties, as reported by FocusEconomics. The BoC's July 2025 Monetary Policy Report acknowledged that inflation remains near its 2% target, despite trade tensions (Monetary Policy Report-July 2025, Bank of Canada). However, C.D. Howe Institute's Monetary Policy Council recommended a 2.50% rate by September 2025, suggesting continued divergence from the Fed's trajectory.

This policy asymmetry has direct implications for the USD-CAD exchange rate. A tighter Fed policy relative to the BoC typically strengthens the U.S. dollar, yet the Canadian dollar's resilience-partly due to its commodity-linked nature-has tempered this effect. For instance, the BoC's rate cuts in early 2025 coincided with a temporary weakening of the USD-CAD rate to 1.3573 CAD (Bank of Canada Monetary Policy Report), illustrating how divergent monetary stances can drive short-term volatility.

Macroeconomic Imbalances: Trade Deficits and Tariff Turbulence

The U.S.-Canada trade relationship, while deeply integrated, has introduced structural imbalances. In 2024, the U.S. posted a $73.6 billion trade deficit in goods with Canada, driven largely by energy exports-60% of U.S. oil imports originated from Canada, according to the US-Canada trade balance report. However, services trade, including U.S. exports of business and financial services, narrowed the overall deficit to an estimated $36–45 billion (US-Canada trade balance report).

The escalation of tariffs in 2025, however, has disrupted this equilibrium. By April 2025, tariffs on steel, aluminum, energy, and autos led to a 15.7% drop in Canadian goods exports to the U.S. and a 10.8% decline in U.S. goods imports, according to Statistics Canada. These measures added inflationary pressures in Canada, with counter-tariffs pushing inflation up by 0.6 percentage points (Bank of Canada Monetary Policy Report). Meanwhile, the U.S. Congressional Budget Office projected that tariffs and reduced immigration would cut 2025 GDP growth by 0.5 percentage points (C.D. Howe Institute publication).

Inflation differentials have further complicated the outlook. Canada's inflation has remained near its 2% target, supported by a stronger CAD and excess supply in key sectors (Bank of Canada Monetary Policy Report). The U.S., however, faces slightly higher inflation in the near term due to the removal of downward pressures from the consumer carbon tax (C.D. Howe Institute publication). These divergent inflation trajectories could influence the BoC's and Fed's policy decisions, with the former prioritizing rate cuts to offset trade-driven inflation and the latter maintaining a tighter stance to anchor expectations.

Investment Implications and Forward Outlook

For investors, the USD-CAD pair presents a nuanced interplay of policy and macroeconomic forces. The Fed's gradual easing and the BoC's more aggressive cuts suggest a potential for CAD strength in the medium term, assuming trade tensions ease. However, the U.S. dollar's safe-haven status and the persistent trade deficit could limit the CAD's upside.

A critical risk lies in the trajectory of U.S.-Canada trade relations. If tariffs persist or escalate, the CAD could face downward pressure due to reduced export volumes and inflationary shocks. Conversely, a resolution of trade disputes might bolster the CAD, particularly if it stabilizes commodity prices and restores cross-border commerce.

Conclusion

The USD-CAD exchange rate in 2025 has been shaped by a delicate balance of central bank policies and macroeconomic imbalances. While the Fed's cautious easing and the BoC's aggressive cuts have created a divergence in monetary trajectories, trade tensions and inflation differentials add layers of complexity. Investors must monitor both policy developments and trade dynamics, as these factors will likely dictate the pair's direction in the coming months.

Comentarios

Aún no hay comentarios