Student Car Loans: Navigating Credit Risk and Growth in a Post-Pandemic World

The post-pandemic recovery has reshaped the financial landscape for student car loans, a niche yet increasingly significant segment of consumer credit. While these loans remain embedded within the broader auto and student loan markets, their unique interplay of growth drivers and emerging risks demands closer scrutiny. Investors must weigh the sector's expansion against structural vulnerabilities, particularly as macroeconomic pressures and shifting borrower behavior collide.

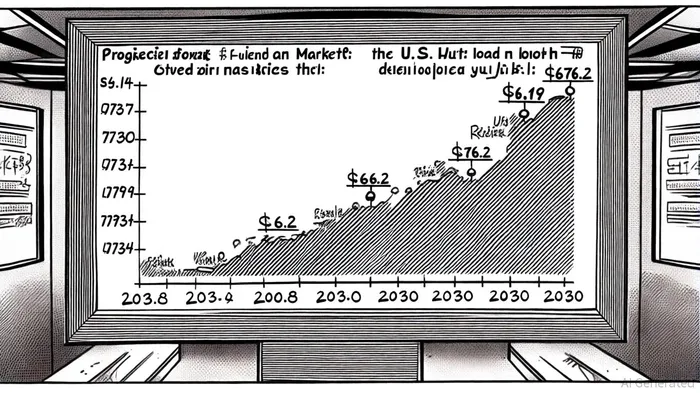

Market Dynamics: Growth and Drivers

The global student loan market, valued at $4.47 trillion in 2025, is projected to grow at a 6.72% compound annual growth rate (CAGR), reaching $6.19 trillion by 2030[1]. In the U.S., private student loans alone are expected to surge from $412.7 billion in 2023 to $980.8 billion by 2032, driven by rising tuition costs and fintech innovation[2]. Meanwhile, the auto loan market—encompassing student car loans—has expanded to $676.2 billion in 2025, with a 5.19% CAGR projected through 2030[3].

The convergence of these trends reflects a critical shift: students and recent graduates, burdened by education debt, increasingly rely on auto financing for transportation. This dual-debt dynamic is amplified by rising vehicle prices (now exceeding $48,000 for new cars[4]) and the normalization of longer loan terms (72–84 months). Fintechs like SoFiSOFI-- and College Ave have capitalized on this demand, offering digital-first lending models with flexible underwriting[5].

Credit Risk: A Looming Shadow

Despite robust growth, the sector faces mounting credit risks. The resumption of student loan repayments in 2024 triggered a 7.74% delinquency rate for student debt (90+ days late) by Q1 2025[7]. This has cascaded into the auto loan market, where 2 million borrowers saw their credit scores drop by 100 points or more due to student loan delinquencies[8]. For younger borrowers—particularly Millennials and Gen Z—this has created a paradox: auto loans, secured by collateral, now compete with student loans for repayment priority, yet the latter's forgiveness options and income-driven plans make them less urgent[9].

The subprime auto loan segment is particularly vulnerable. Delinquency rates for subprime and near-prime auto loans have approached 2008-levels, driven by $600+ monthly payments and $48,000+ loan amounts[10]. Lenders like Tricolor Holdings have already collapsed under these pressures[11], while traditional banks tighten credit standards. For student car loan borrowers, the risk is compounded: they often lack the income stability to manage both debt types, yet their thin credit files make alternative underwriting essential[12].

Demographics and Lender Adaptation

Millennials and Gen Z now dominate auto loan applications, with 31% of Millennials planning vehicle purchases in 2024–2025[13]. However, these borrowers frequently lack robust credit histories, forcing lenders to adopt alternative data models (e.g., rental payments, utility bills) to assess risk[14]. Fintechs are leading this shift, leveraging AI-driven analytics to price risk more granularly. For example, SoFi's “income-based repayment” for auto loans mirrors federal student loan programs, adjusting payments to borrowers' cash flow[15].

Regulatory uncertainty further complicates the landscape. The Biden administration's student loan forgiveness programs and potential changes to auto loan repossession laws could alter risk profiles overnight[16]. Investors must monitor these developments closely, as they could either stabilize the sector or exacerbate defaults.

Investment Implications

The student car loan market presents a high-growth, high-risk proposition. On one hand, the $1.6 trillion U.S. auto loan market[17] and $4.47 trillion student loan market[1] offer vast expansion opportunities, particularly for fintechs with agile underwriting. On the other, the interconnectedness of student and auto debt—exacerbated by inflation, interest rate hikes, and regulatory shifts—poses systemic risks.

For conservative investors, opportunities lie in federally backed student loans and prime auto loans, which benefit from repayment flexibility and lower delinquency rates. Aggressive investors might target fintechs innovating in alternative credit scoring or income-driven auto repayment plans, though these carry liquidity risks. Caution is warranted for subprime auto lenders, where delinquency rates and bankruptcies are rising[18].

Conclusion

The student car loan market is a microcosm of broader post-pandemic financial fragility. Its growth is inextricably linked to the resilience of borrowers navigating dual-debt burdens. While innovation and digitalization offer pathways to mitigate risk, the sector remains exposed to macroeconomic shocks and policy shifts. For investors, the key lies in balancing exposure to high-growth fintechs with hedging against systemic vulnerabilities—a challenge that demands both foresight and agility.

Comentarios

Aún no hay comentarios