Strategic Positioning in Global Equities Amid US-China Trade Easing

The US-China trade conflict, now in its seventh year, has entered a phase of cautious de-escalation. After a dramatic spike in tariffs in early 2025—reaching 245% on Chinese imports by the US and 125% on American goods by China—the two sides have agreed to a fragile truce, reducing tariffs to 30% and 10%, respectively[1]. This temporary pause, extended until November 2025, has injected a degree of stability into global markets, though underlying tensions persist. For investors, the challenge lies in navigating the uncertainty while capitalizing on emerging opportunities in a reshaped global economy.

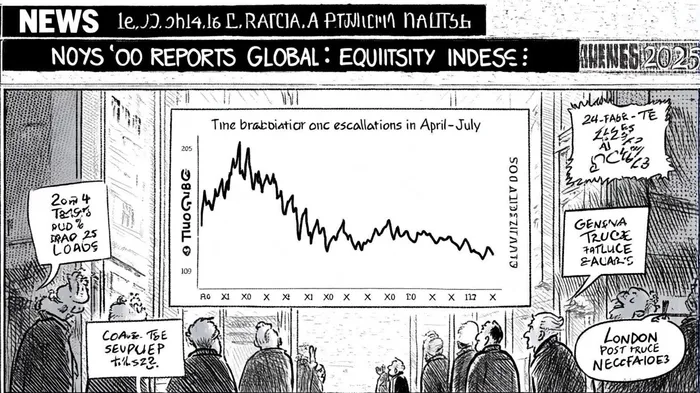

The Market Impact of Tariff Volatility

The recent trade tensions have left an indelible mark on equity markets. In April 2025, as tariffs surged to unprecedented levels, global indices experienced sharp corrections. The Hang Seng Index, for instance, fell over 2% in a single session, reflecting heightened risk aversion[5]. Chinese equities, particularly those in export-dependent sectors, faced significant headwinds, with China's share of US imports declining from 22% in 2018 to 14% in 2023[3]. However, the truce agreements in May and July 2025 have provided a degree of relief. Chinese indices like the FTSE China A50 have shown improved valuations and profitability compared to previous trade disputes, suggesting a partial recovery of investor confidence[3].

The resilience of certain sectors—such as Financials and Technology—has been notable. UBSUBS-- and Goldman SachsGS-- have upgraded their outlooks for China's market, citing growth in AI and semiconductor industries[5]. This shift underscores the importance of sectoral diversification in mitigating trade-related risks.

Strategic Positioning Amid Fragile Easing

The current truce offers a window for strategic positioning, but it is not without caveats. First, the reduction in tariffs has not resolved deeper structural issues, such as China's export controls on rare earth minerals or US restrictions on advanced technology transfers[1]. Second, legal challenges to Trump's tariff authority, including a federal court ruling questioning the scope of IEEPA powers[6], suggest that the legal and political landscape remains fluid.

Investors must therefore balance optimism with caution. Diversification into regions less exposed to US-China tensions—such as Southeast Asia—has emerged as a key strategy[5]. Vietnam, Indonesia, and Japan, for example, have seen targeted US tariffs (20-40%) as part of a broader effort to deter trade diversion[6]. While this complicates supply chains, it also creates opportunities in markets adapting to the new normal.

The Role of Geopolitical Narratives

Beyond tariffs, the trade conflict has evolved into a geopolitical contest. Both nations are leveraging economic tools to advance strategic objectives, from securing critical mineral supplies to dominating next-generation technologies[4]. This dimension adds complexity to market analysis. For instance, China's PMI data, which signals labor market strains and growth moderation[6], must be interpreted alongside its broader geopolitical ambitions.

Investors should also monitor the durability of the truce. While the 90-day extensions have provided breathing room, the absence of a comprehensive resolution means that renewed escalations remain a risk. The London negotiations in June 2025, which addressed rare earth supply chains and student visas[4], are a positive step, but their implementation will be critical.

Conclusion: Navigating Uncertainty with Discipline

The US-China trade conflict is a defining feature of the current global economic landscape. While the recent truce has eased immediate pressures, the path forward remains fraught with uncertainty. For equity investors, the key lies in disciplined strategic positioning: favoring resilient sectors, diversifying geographically, and maintaining liquidity to capitalize on volatility.

As the November 2025 deadline approaches, the focus will shift to whether the two sides can move beyond temporary fixes to address systemic imbalances. Until then, markets will remain sensitive to every diplomatic signal, tariff adjustment, and geopolitical development. In this environment, patience and adaptability will be the hallmarks of successful investment strategies.

Comentarios

Aún no hay comentarios