Southwest Airlines' Strategic Shift to Long-Haul Flights: A Calculated Gamble in a Reshaping Industry

In the ever-evolving U.S. airline industry, SouthwestLUV-- Airlines' recent pivot toward long-haul international flights marks a bold departure from its traditional low-cost, short-haul model. This strategic shift, announced by CEO Bob Jordan in late 2025, reflects both the pressures of a competitive market and the airline's ambition to diversify revenue streams. However, the question remains: Can Southwest replicate its domestic success in the high-cost, high-stakes arena of international travel while maintaining its profitability?

A Strategic Reorientation: From Domestic Dominance to Global Ambitions

Southwest's long-haul strategy is underpinned by a mix of operational adjustments and product innovation. The airline has announced plans to deploy narrow-body aircraft for initial international routes—a cost-conscious approach that avoids the capital intensity of wide-body fleets[1]. This aligns with its historical emphasis on efficiency, though it raises questions about the viability of narrow-body planes for transcontinental or transatlantic routes, where passenger density and ancillary revenue are critical.

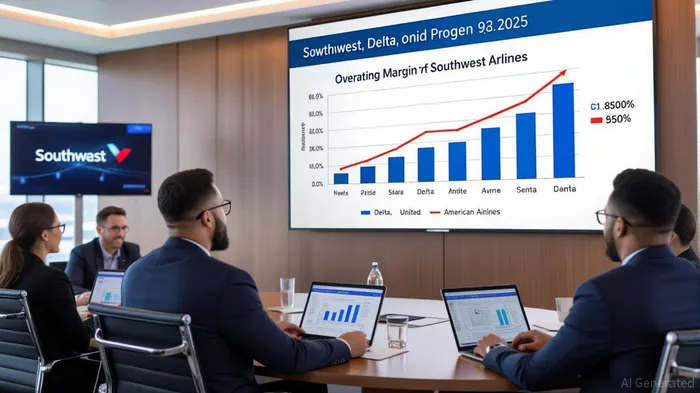

Financially, Southwest has demonstrated resilience. Its Q2 2025 results revealed a net income of $213 million and a $1.6 billion return to shareholders via dividends and buybacks[2]. These figures underscore a disciplined approach to capital allocation, even as the airline grapples with a mere 1.16% operating margin—a stark contrast to Delta's 13.2% and United's 8.7% in the same period[3]. The introduction of bag fees, basic economy fares, and planned premium seating (launching in early 2026) signals a broader effort to monetize ancillary services, a strategy that has propelled competitors like DeltaDAL-- and American AirlinesAAL-- to higher profitability[4].

Competitive Positioning: Navigating a Crowded Skies

Southwest's domestic dominance has long been a function of its point-to-point network and cost discipline. Yet, as the industry shifts toward premium differentiation and international expansion, the airline faces an existential challenge. Delta and United have capitalized on this trend, with Delta reporting $15.6 billion in Q2 operating revenues and United achieving a 9% year-over-year increase in premium cabin revenue[3]. These carriers have leveraged wide-body aircraft, loyalty program enhancements, and credit card partnerships to secure premium yield, areas where Southwest's single-class model lags[5].

Historical stock performance around earnings releases offers additional context. Delta (DAL) has shown the strongest short-term reaction, with a statistically significant +2% to +3% price increase within three days of earnings announcements and a win rate exceeding 70%[3]. In contrast, Southwest (LUV) and American (AAL) exhibit more modest patterns: LUVLUV-- shows a ~5% positive drift over 30 days, while AALAAL-- lags with a ~1% drift, though neither reaches statistical significance. United (UAL), meanwhile, displays highly variable results, likely due to its smaller post-2022 sample size[3].

The airline's recent network restructuring—eliminating 29 domestic routes and adopting a hub-and-spoke model—suggests an acknowledgment of these pressures[6]. By focusing on high-demand leisure destinations (e.g., the Caribbean) and forging partnerships like its 2025 alliance with Icelandair, Southwest aims to bridge the gap. However, its long-haul ambitions must contend with Delta's A330neo deployments and United's aggressive expansion into markets like Mongolia and Taiwan[7].

Risks and Rewards: A Calculus of Profitability

Southwest's long-term profitability hinges on its ability to balance cost control with revenue innovation. Its $2.0 billion share repurchase program and $213 million Q2 net income highlight a commitment to shareholder returns[2]. Yet, the airline's operating margin remains a vulnerability. Analysts at Morgan StanleyMS-- note that Southwest's EBIT2 guidance for 2025 ($600–800 million) pales against Delta's $1.2 billion pre-tax profit in Q2 alone[3].

The risks of long-haul expansion are manifold. International routes demand higher fuel efficiency, crew costs, and regulatory compliance—areas where Southwest's narrow-body strategy may prove insufficient. Moreover, its reliance on domestic demand leaves it exposed to macroeconomic headwinds, as evidenced by its 1.5% year-over-year decline in operating revenues in Q2 2025[2].

Conversely, successful execution could unlock new revenue pools. The airline's projected $4.3 billion in incremental EBIT by 2026—driven by premium seating and capacity reductions—suggests confidence in its transformation[2]. If Southwest can replicate its domestic cost advantages in international markets, it may yet carve out a niche.

Conclusion: A High-Stakes Bet for Industry Relevance

Southwest's strategic shift is emblematic of the broader U.S. airline industry's recalibration. While Delta and United have solidified their positions through premium differentiation and global reach, Southwest's long-haul gambit represents a high-risk, high-reward endeavor. For investors, the key variables will be the airline's ability to execute its product innovations, manage operational complexity, and sustain profitability in a sector where margins are razor-thin.

In the end, Southwest's success will depend not on challenging the titans of international aviation but on redefining its own model to thrive in a world where even the most iconic airlines must adapt or perish.

Comentarios

Aún no hay comentarios