Is PROCEPT BioRobotics (PRCT) a Distressed Opportunity or a Cautionary Tale? Valuation Realism and Market Overreaction in Robotics-Aided Surgery

Revenue Growth and Operational Momentum

PROCEPT BioRobotics has demonstrated robust top-line growth in 2025. For Q2, the company reported revenue of $79.2 million, a 48% year-over-year increase, driven by strong U.S. system sales (51 robotic systems sold) and a 58% surge in handpiece and consumable revenue to $43.1 million, according to the company's Q2 2025 results (https://ir.procept-biorobotics.com/news-releases/news-release-details/procept-biorobotics-reports-second-quarter-2025-financial). International revenue also grew by 69% to $9.6 million, reflecting expanding global adoption. Gross margins improved to 65%, up from 59% in the prior year, due to higher average selling prices and operational efficiencies, the company noted. These metrics suggest a company gaining traction in its core markets.

However, profitability remains elusive. Operating expenses rose to $73.9 million, driven by investments in commercial expansion and R&D, resulting in a net loss of $19.6 million for the quarter, per the company's Q2 2025 results. While this represents an improvement from a $25.6 million loss in 2024, the Adjusted EBITDA loss of $8.0 million underscores the company's reliance on capital to sustain growth.

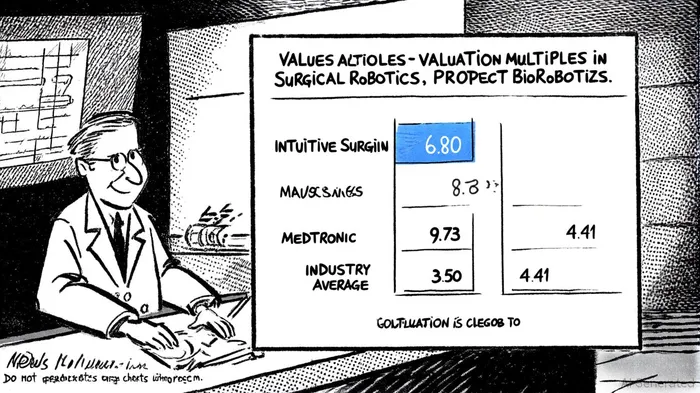

Valuation Metrics: A Tale of Two Realities

The company's P/S ratio of 6.80 is significantly higher than the surgical robotics industry's implied benchmark. For context, Intuitive Surgical's P/S ratio is 9.73 (Intuitive Surgical's P/S ratio), while Medtronic's Hugo system has a P/S ratio of 3.50. The broader medical devices industry has an average P/S ratio of 4.41 (industry P/S ratio), suggesting that PRCT's valuation is elevated relative to both peers and the sector.

This discrepancy raises questions about whether the market is pricing in PRCT's growth potential or overestimating its long-term prospects. Analysts project full-year 2025 revenue of $325.5 million, a 45% increase from 2024, but the company anticipates an Adjusted EBITDA loss of $35 million for the year, according to its Q2 filing. By contrast, Intuitive Surgical's Q2 2025 revenue of $2.44 billion (up 21.4% YoY) and its $206.6 billion market cap reflect a more mature business model with established profitability.

Market Overreaction and Structural Risks

The surgical robotics market is projected to grow at a compound annual growth rate (CAGR) of 15.62%, reaching $45.93 billion by 2034 (surgical robotics market projection). While this bodes well for the sector, PRCT's position as a niche player in benign prostatic hyperplasia (BPH) treatment via Aquablation therapy introduces unique risks. Short-seller Spruce Point Capital Management has criticized the company for overestimating its addressable market and questioned the scalability of its technology, which it argues primarily serves a narrow subset of patients with larger prostates (Spruce Point's critique).

Moreover, PRCT's balance sheet, while strong with $305.8 million in cash, faces headwinds from global tariffs that could reduce gross margins by $1–2 million in 2025, the company noted. The company's reliance on recurring revenue from consumables (now 55% of U.S. revenue) is a double-edged sword: while it ensures long-term cash flow, it also exposes PRCT to pricing pressures and competition from generic alternatives.

Investor Sentiment and Analyst Outlook

Despite these risks, investor sentiment remains cautiously optimistic. Wall Street analysts have assigned a "Moderate Buy" consensus, with an average price target of $74.88-implying an 88% upside from the current price (MarketBeat forecast). This optimism is partly fueled by PRCT's expanding U.S. hospital penetration and its international expansion plans. However, the stock's year-to-date return of -58.4% and a 12-month total shareholder return of -53.2% highlight the volatility inherent in high-growth, unprofitable companies, as noted in a recent Yahoo Finance analysis (https://finance.yahoo.com/news/procept-biorobotics-prct-evaluating-valuation-091232722.html).

A Balancing Act: Opportunity or Overreaction?

The key to assessing PRCT lies in reconciling its growth trajectory with its valuation. A P/S ratio of 6.80 implies that investors expect the company to achieve a revenue run rate of $325.5 million in 2025 and eventually transition to profitability. This is plausible if PRCT continues to gain market share in BPH and expands into adjacent indications. However, the company's current financials-negative EBITDA, weak ROE (-26.40%), and high operating leverage-suggest that profitability is years away, if achievable at all, according to the company's Q2 2025 disclosure.

In contrast, Intuitive Surgical's P/S ratio of 9.73 reflects a market that values its dominance in general surgery and its next-generation da Vinci 5 platform. Medtronic's lower P/S ratio (3.50) aligns with its diversified medical device portfolio and more conservative growth profile. PRCT's valuation appears to occupy a middle ground, but its lack of a clear path to profitability and the skepticism from short sellers like Spruce Point introduce significant uncertainty.

Conclusion: A Distressed Opportunity with Caveats

PROCEPT BioRobotics embodies the duality of the surgical robotics sector: it is a high-growth innovator with a compelling value proposition but also a company burdened by unprofitability and structural risks. For value investors, the stock may represent a distressed opportunity if the market overcorrects for its challenges, particularly if PRCT can demonstrate sustainable margin expansion and broader adoption of its technology. However, the current valuation of 6.8x sales appears to price in a level of success that is far from guaranteed, especially given the company's narrow therapeutic focus and the skepticism from short sellers.

In the end, the answer to whether PRCT is a distressed opportunity or a cautionary tale hinges on one question: Can the company scale its Aquablation therapy beyond a niche application and achieve profitability without sacrificing growth? Until that question is answered, the market remains a battleground between optimism and caution.

Comentarios

Aún no hay comentarios