Political Polarization and the Defense-Industrial Complex: Strategic Opportunities in a Fractured America

The United States stands at a crossroads of political polarization and security redefinition. President Donald Trump's 2025 designation of Antifa as a “major terrorist organization” has reignited debates about the boundaries of domestic counterterrorism and the role of the state in surveilling its citizens. While legal scholars swiftly dismissed the move as constitutionally untenable—given Antifa's decentralized, leaderless structure and the absence of a federal statute criminalizing domestic terrorism—the political symbolism has already begun to reshape policy priorities and market dynamics. For investors, this moment offers a unique lens to analyze how political rhetoric, even when legally constrained, can catalyze shifts in defense contracting, surveillance technology, and homeland security funding.

The Legal and Practical Limits of Designation

Trump's declaration, though legally infeasible, underscores a broader trend: the weaponization of counterterrorism frameworks to address domestic political adversaries. Antifa, as a loosely affiliated network of activists, lacks the hierarchical structure required for designation under U.S. law, which reserves such labels for foreign entities like ISIS or Al-Qaeda [1]. However, the administration's rhetoric has already prompted law enforcement agencies to recalibrate their focus. The FBI's domestic terrorism investigations, which quadrupled between 2013 and 2021, now face renewed pressure to prioritize left-wing extremism, even as the agency struggles with inter-agency coordination and outdated legal tools [2].

This shift is not without precedent. The post-9/11 expansion of the Department of Homeland Security (DHS) saw a 41% increase in defense contract obligations between 2015 and 2020, driven by investments in air and missile defense systems [3]. While Antifa's designation has not triggered a similar surge in defense spending, it has accelerated the adoption of surveillance technologies under the guise of “threat mitigation.” For instance, the airborne countermeasure system market—valued at $12.5 billion in 2023—is projected to grow at a 6.5% CAGR through 2032, driven by demand for systems like the ALE-47 dispenser to counter MANPADS and electronic attacks [4].

Surveillance Technology: A Double-Edged Sword

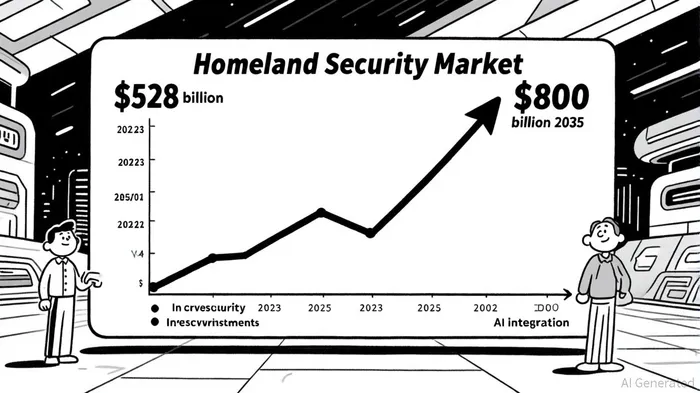

The surveillance technology sector, already booming at a 10% CAGR, is poised to benefit from the political climate. The U.S. homeland security market, valued at $528 billion in 2023, is expected to reach $800 billion by 2035, fueled by cybersecurity investments and AI-driven threat detection [5]. Trump's Antifa designation, while legally symbolic, has amplified calls for expanded surveillance of protests and activist networks. This has led to increased procurement of biometric identification systems, facial recognition software, and real-time data analytics tools by federal and state agencies.

However, the sector faces headwinds. U.S.-China trade tensions have disrupted supply chains for critical components like AI chips, raising production costs and delaying deployments [6]. Additionally, ethical concerns about privacy violations—exemplified by the 68% of U.S. workers reporting electronic monitoring in the workplace—risk regulatory pushback [7]. Investors must weigh these risks against the long-term growth potential of a sector increasingly entangled with political priorities.

Homeland Security: A New Frontier for Defense Contractors

The DHS's 2024 budget justification reveals a strategic pivot toward domestic threats, with expanded funding for the Targeted Violence and Terrorism Prevention Grant Program [8]. While no direct link exists between Antifa's designation and increased defense budgets, the political climate has incentivized contractors to rebrand existing capabilities as “domestic counterterrorism solutions.” For example, companies like Northrop GrummanNOC-- and L3HarrisLHX-- Technologies are now marketing cognitive electronic warfare systems—originally designed for military use—to local law enforcement agencies [9].

This trend is further amplified by the rise of Other Transaction Authority (OTA) agreements, which allow the Department of Defense to bypass traditional procurement processes for rapid R&D. In 2020, OTA spending surged by 29% in air and missile defense, reflecting a shift toward agile, innovation-driven contracts [10]. For firms specializing in AI, cybersecurity, or biometric surveillance, the window to secure OTA partnerships is narrowing.

Strategic Investment Opportunities

For long-term investors, the key lies in identifying sectors poised to benefit from policy inertia rather than direct legislative action. The airborne countermeasure and cybersecurity markets, with their high growth rates and bipartisan support, offer relatively stable opportunities. Similarly, firms developing AI-driven surveillance tools for “predictive policing” or crowd monitoring are likely to see sustained demand, despite ethical controversies.

However, caution is warranted. The legal and political challenges to Trump's Antifa designation—particularly First Amendment concerns—could lead to regulatory rollbacks or public backlash. Investors should prioritize companies with diversified revenue streams and a track record of navigating policy shifts.

Conclusion

Political polarization has transformed the U.S. defense and security sectors into arenas of ideological competition. While Trump's Antifa designation may lack legal teeth, its political resonance has already begun to reshape market dynamics. For investors, the challenge is to distinguish between fleeting rhetoric and enduring trends. The sectors most likely to thrive are those that align with both immediate policy priorities and long-term technological imperatives—particularly in cybersecurity, AI-driven surveillance, and agile defense contracting. In a fractured America, the winners will be those who can navigate the intersection of politics, technology, and capital with precision.

Comentarios

Aún no hay comentarios