Poland's Monetary Easing and Fiscal Challenges: Strategic Entry Points for Equity and Fixed-Income Investors

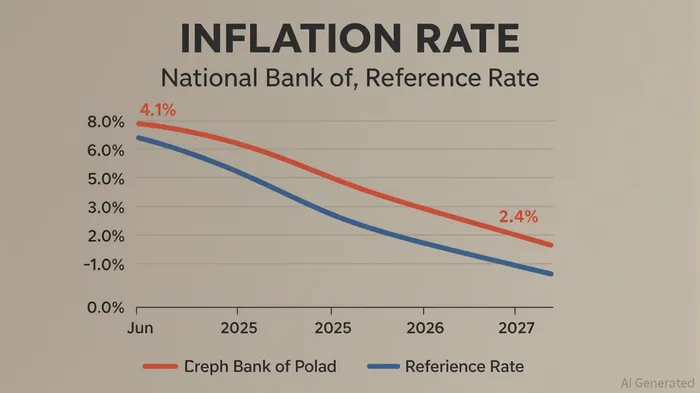

The National Bank of Poland (NBP) has embarked on a measured easing cycle, cutting its benchmark interest rate by 25 basis points in July 2025 to 5.00% annually, reflecting a growing confidence that inflation will stabilize near its target. This decision followed a downward revision of inflation forecasts to 4.0% year-on-year for 2025, from 4.9% in March, and a projection of 3.1% in 2026 and 2.4% in 2027 [3]. While June 2025 inflation rose slightly to 4.1%, still above the 3.5% upper target, the NBP emphasized that further easing is contingent on incoming data, suggesting a flexible but cautious approach [4]. For investors, this signals a potential window for equity and fixed-income opportunities, as monetary accommodation could stimulate growth while fiscal pressures create volatility.

Poland’s fiscal landscape, however, remains a double-edged sword. The general government deficit is projected to narrow marginally to 6.4% of GDP in 2025 from 6.6% in 2024, driven by sustained spending on defense, social programs, and infrastructure [1]. Yet, public debt is expected to rise to 65.3% of GDP by 2026, reflecting the cumulative impact of high deficits and EU-funded projects [2]. This fiscal fragility is compounded by political polarization, which has delayed meaningful consolidation. The 10-year government bond yield, at 5.56% in late August 2025, reflects investor concerns about debt sustainability [1]. For fixed-income investors, this suggests a trade-off: higher yields offer returns but come with risks tied to fiscal slippage and potential rating downgrades.

Equity investors may find strategic entry points in sectors benefiting from EU-funded infrastructure projects and robust private consumption. The Polish economy is forecast to grow by 3.3% in 2025, supported by a stable labor market (unemployment projected at 2.8% by 2026) and a rebound in investment [1]. Sectors such as construction, utilities, and consumer goods could outperform, particularly as the NBP’s easing cycle lowers borrowing costs. However, fiscal challenges—such as rising debt and political gridlock—introduce uncertainty, necessitating a balanced portfolio that hedges against potential volatility.

For fixed-income investors, the NBP’s easing trajectory and the projected decline in inflation present opportunities. If inflation remains below the 3.5% target, the NBP may continue cutting rates, potentially boosting bond prices. Yet, the risk of a fiscal shock—such as a sudden rise in borrowing costs or a downgrade of Poland’s credit rating—cannot be ignored. A diversified approach, combining shorter-duration bonds and inflation-linked instruments, could mitigate these risks while capitalizing on the current yield environment.

In conclusion, Poland’s monetary and fiscal dynamics create a complex but navigable landscape for investors. The NBP’s easing cycle and the outlook for falling inflation offer tailwinds for equities and fixed-income markets, while fiscal challenges demand caution. Strategic entry points exist for those who can balance the potential rewards of growth and yields against the risks of fiscal fragility.

Source:[1] Economic forecast for Poland - Economy and Finance [https://economy-finance.ec.europa.be/economic-surveillance-eu-economies/poland/economic-forecast-poland_en][2] Poland: political polarisation, high deficits strain fiscal ... [https://scoperatings.com/ratings-and-research/research/EN/178966][3] In a surprise move, the National Bank of Poland cut interest rates [https://think.ing.com/articles/polands-nbp-cuts-interest-rates-next-decision-not-until-september/][4] Poland Interest Rate [https://tradingeconomics.com/poland/interest-rate]

Comentarios

Aún no hay comentarios