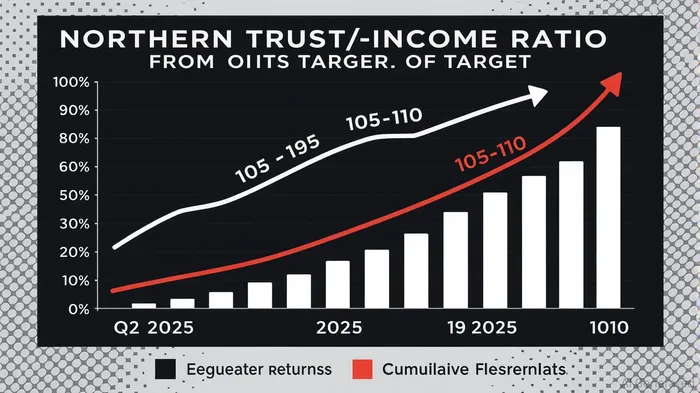

Northern Trust's Strategic Momentum and Shareholder Returns: A Case for Capital Appreciation

Northern Trust Corporation (NTRS) has emerged as a compelling case study in the delicate balance between operational efficiency and shareholder returns. In Q2 2025, the firm reported a 8% year-over-year revenue increase to $2 billion, driven by organic growth in asset servicing and wealth management[1]. More striking, however, was its strategic focus on reducing the cost-to-income ratio—a metric that stood at 115 in Q2 2025 but is targeted to fall to 105–110 in the medium term[2]. This ambition reflects a broader industry trend toward leveraging scale and technology to enhance profitability, a strategy Northern Trust's CEO, Mike O'Grady, has described as prioritizing “independence and scale over size”[1].

The company's operational leverage is evident in its expense management. Noninterest expenses in Q2 2025 fell 7.6% year-over-year to $1.416 billion, despite a 4.8% increase in expenses when excluding notable items[2]. This duality—reducing costs while maintaining growth—positions Northern TrustNTRS-- to achieve its revised return on equity (ROE) target of 13–15%[1]. Such efficiency gains are not merely arithmetic; they are structural, underpinned by investments in talent, technology, and product expertise[1]. For instance, the firm's record net interest income of $615.2 million in Q2 2025, supported by $122.4 billion in average deposits, underscores its ability to monetize operational scale[2].

Equally compelling is Northern Trust's capital return strategy. In Q2 2025 alone, the firm returned $485.6 million to shareholders through a combination of share repurchases and dividends—a sum exceeding its net income for the period[2]. This aggressive approach is underpinned by a robust capital position, with a common equity tier one (CET1) ratio of 12.2%, well above regulatory requirements[2]. The dividend increase of 7% to $0.75 per share in Q2 2025 further signals confidence in earnings sustainability, particularly given a payout ratio of 0.32%, which leaves ample room for reinvestment[3].

Critics may note the absence of granular 2024–2025 share repurchase data beyond the Q2 2025 figure. However, historical context provides reassurance: in 2023, Northern Trust repurchased $669 million of shares, completing its 2021 authorization[4]. The firm's commitment to monthly redemptions under its repurchase program suggests a disciplined approach to capital allocation[4]. When combined with its 5.67% dividend yield (as of September 2025), this strategy creates a dual incentive for long-term investors[3].

The interplay between operational efficiency and capital returns is where Northern Trust's value proposition crystallizes. By reducing its cost-to-income ratio, the firm enhances profitability, which in turn fuels higher dividend payouts and repurchase capacity. This virtuous cycle is further reinforced by its focus on technology investments, which not only drive efficiency but also future-proof its asset servicing and wealth management platforms[2].

For investors, the case for Northern Trust rests on its ability to harmonize these two pillars. While the cost-to-income ratio remains above its target range, the trajectory is clear. Similarly, while share repurchase figures for 2024–2025 are not fully disclosed, the Q2 2025 performance demonstrates a willingness to prioritize shareholder value even in periods of strong earnings. In an era where capital discipline is paramount, Northern Trust's strategic momentum offers a rare alignment of operational rigor and investor-friendly policies.

Comentarios

Aún no hay comentarios