Nigeria's Potential Eurobond Issuance and Its Strategic Implications for African Sovereign Debt Markets

In the post-pandemic era, African sovereign debt markets have become a battleground for balancing fiscal austerity with growth ambitions. Nigeria's planned Eurobond issuance in late 2025, alongside its recent $2.2 billion 2024 offering, offers a compelling case study of how emerging markets navigate inflationary pressures and shifting investor sentiment. For international investors, the question is not merely whether to invest in Nigeria but how its trajectory compares to peers like Zambia and Ghana-and what this reveals about the broader risks and rewards of African debt.

Nigeria's Eurobond Landscape: A Tale of Reform and Resilience

Nigeria's 2025 Eurobond, with a 7.625% coupon and November 2025 maturity, has traded near par ($99.526) as of December 2024, reflecting investor confidence in its near-term safety according to an IMF report. This contrasts with longer-dated Nigerian bonds, which trade at higher yields and lower prices, underscoring market skepticism about medium-term risks, as noted in the same IMF report. The government's push to return to the Eurobond market in late 2025-potentially raising $2.3 billion for refinancing and budget support-follows policy prescriptions outlined in an AfronomicsLaw brief and is underpinned by structural reforms: fuel subsidy removal, foreign exchange liberalization, and a current account surplus of 6.9% of GDP in 2025, figures highlighted by the IMF report.

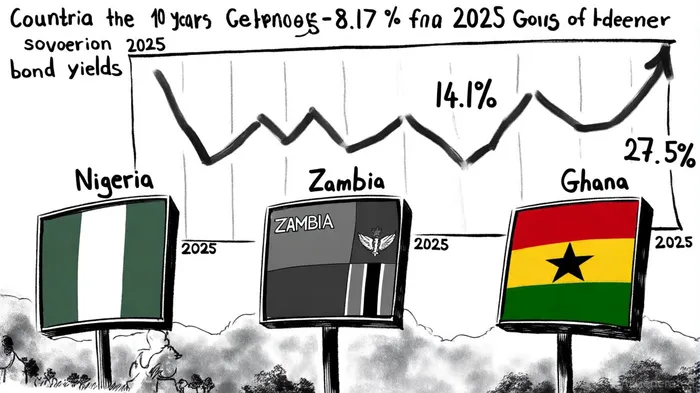

The International Monetary Fund (IMF) has noted these reforms as "credible," though it cautions that Nigeria's debt-to-GDP ratio remains elevated at 28% (IMF). Crucially, the anticipation of a U.S. Federal Reserve rate cut in September 2025 has lowered global borrowing costs, making Nigeria's Eurobond yields more attractive. As of July 2025, Nigeria's 10-year bond yields had fallen to a three-year low of 8.17%, down from over 11% in April 2025, a trend tracked in The Marketbrain piece. This decline mirrors broader investor optimism, with the 2024 Eurobond oversubscribed at $9 billion against a $2.2 billion target, also reported by The Marketbrain piece.

Comparative Analysis: Nigeria vs. Zambia and Ghana

Nigeria's relative success in stabilizing its debt profile contrasts sharply with its neighbors. Zambia, still technically in "Selective Default" status, has seen its restructured Eurobonds trade at spreads implying a de facto B+ rating, despite official ratings remaining below investment grade, according to The Marketbrain piece. This divergence reflects market anticipation of Zambia's fiscal consolidation, including a 4.5% Q1 2025 GDP growth and a projected debt-to-GDP decline to 100% by 2025. However, Zambia's 14.1% inflation rate in June 2025-compared to Nigeria's 22.97% in May 2025, as reported by Marketnewsng-highlights the fragility of its recovery.

Ghana, meanwhile, faces a more dire scenario. Its 2035 Eurobonds traded at 73.3 cents on the dollar in March 2025, reflecting investor anxiety over a $9 billion energy debt burden by 2027, a point emphasised in the AfronomicsLaw brief. Despite a new government pledging fiscal discipline, Ghana's 27.5% 10-year bond yield, reported by Marketnewsng, remains a stark warning of the costs of delayed reforms. Nigeria's lower yields and stronger current account position it as a relative safe haven in a region where debt sustainability remains a critical concern (IMF).

Risks and Rewards in a Volatile Environment

For investors, Nigeria's Eurobond offers a unique blend of risk mitigation and reward potential. On the reward side, the country's structural reforms-backed by a Moody's upgrade from Caa1 to B3, reported by Marketnewsng-have improved credit metrics. The proposed $2.3 billion issuance, partly via a Sukuk with Islamic credit enhancement, is detailed in the AfronomicsLaw brief and could further diversify investor bases. Additionally, Nigeria's near-term Eurobond (maturing in November 2025) provides liquidity in a market where longer-dated instruments are perceived as riskier (IMF).

Yet risks persist. First, inflation remains stubbornly high, and a delayed Fed rate cut could reverse capital inflows. Second, Nigeria's reliance on oil exports (accounting for 90% of foreign exchange earnings, per the IMF report) exposes it to commodity price shocks. Third, the proposed $2.3 billion borrowing must be weighed against a $20 billion regional interest bill for African external debt in 2025, a pressure highlighted by Marketnewsng, which strains fiscal space.

Strategic Implications for African Debt Markets

Nigeria's experience underscores a broader trend: the shift from multilateral to commercial borrowing in Africa. As noted in the AfronomicsLaw brief, countries like Ghana and Zambia now service over 60% of external debt to private creditors. This shift complicates debt restructuring, as seen in Ghana's protracted negotiations with bondholders. Nigeria's use of Eurobonds to refinance maturing debt-rather than relying solely on multilateral lenders-reflects a pragmatic but precarious strategy.

For investors, the key is to differentiate between countries with credible reform agendas (Nigeria) and those trapped in austerity cycles (Ghana). Nigeria's near-term Eurobond, with its shorter maturity and lower yield, offers a hedge against the volatility of longer-dated African debt. However, the broader lesson is that African sovereign bonds remain a high-risk, high-reward asset class, where macroeconomic discipline and commodity price dynamics are decisive.

Conclusion

Nigeria's 2025 Eurobond issuance is more than a domestic fiscal maneuver-it is a microcosm of the challenges facing African sovereign debt markets. While the country's reforms and favorable timing (ahead of a potential Fed rate cut) make it an attractive proposition, investors must remain vigilant about inflationary pressures and commodity dependence. In a post-pandemic world where inflation sensitivity dominates, Nigeria's relative stability offers a rare but not risk-free opportunity in the emerging markets arena.

Comentarios

Aún no hay comentarios