Navigating the Fed's Crossroads: Rate Cuts, Tariffs, and Opportunities in a Shifting Landscape

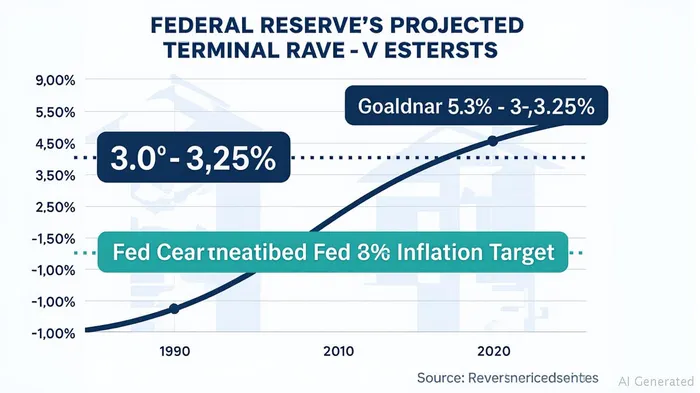

The Federal Reserve's policy path has become a battleground of expectations, with GoldmanGS-- Sachs' revised forecasts offering a critical pivot point for investors. As inflationary pressures ease—thanks in part to tempered tariff impacts—the Fed's terminal rate has been recalibrated downward to 3.0–3.25%, while the likelihood of a September rate cut now exceeds 50%. This shift, driven by a confluence of disinflationary forces and labor market softness, presents a window to position portfolios ahead of a potential policy pivot.

The New Inflationary Calculus: Tariffs and the “Muddle-Through” Economy

Goldman Sachs' economists have long argued that tariffs—once seen as a persistent inflationary threat—have instead delivered a “one-time price shock” rather than sustained upward pressure. With wage growth cooling and demand weakening, anti-inflationary forces are now gaining traction. This reassessment has reshaped the Fed's outlook: instead of a prolonged pause, the path now favors gradual easing.

The September rate cut, now priced in at over 50%, reflects this evolution. Goldman's team, led by David Mericle and Jan Hatzius, points to two critical factors:

1. Labor Market Resilience with Hidden Weaknesses: Payroll data remains robust, but residual seasonality and immigration policy changes could introduce volatility, pushing the Fed to preemptively soften its stance.

2. Disinflationary Offsets: Even as core services inflation lingers, the fading influence of tariffs and slowing wage growth are diluting upward price pressures.

The implications are profound. A September cut would mark the start of a 75-basis-point easing cycle by year-end, reshaping Treasury yields and the dollar.

Dollar Weakness and Rate-Sensitive Sectors: Where to Deploy Capital

A Fed pivot toward easing typically weakens the U.S. dollar, as lower rates reduce its relative yield advantage. This dynamic creates a dual opportunity:

1. Tech and Consumer Discretionary: Rate-sensitive sectors thrive in a low-interest environment. Lower borrowing costs can boost corporate investment and consumer spending, favoring stocks like AmazonAMZN-- (AMZN) and MicrosoftMSFT-- (MSFT).

- Emerging Markets and Commodities: A weaker dollar lifts EM equities and commodities priced in USD, such as copper or gold.

However, investors must balance this optimism with caution. Tariff-related risks persist, particularly in sectors like autos (e.g., Ford, F) or semiconductors (e.g., NVIDIANVDA--, NVDA), where supply-chain dynamics remain fragile.

Hedging Against Tariff Uncertainty: A Pragmatic Approach

While Goldman's forecasts suggest a Fed willing to ease, the path is not without potholes. A sudden surge in wage inflation or a hawkish policy misstep could delay cuts. To mitigate this:

1. Sector Diversification: Pair exposure to tech/consumer discretionary with defensive plays like utilities (e.g., NextEra Energy, NEE) or healthcare (e.g., Johnson & Johnson, JNJ), which are less tariff-sensitive.

2. Currency Hedging: Use USD-denominated bonds or inverse USD ETFs (e.g., UDN) to hedge against dollar depreciation.

3. Option Strategies: Consider put options on rate-sensitive stocks to limit downside risk if the Fed delays easing.

Conclusion: Position for Policy Shifts, but Stay Vigilant

Goldman's revised forecasts underscore a Fed navigating between inflation control and growth support—a balancing act that favors investors who anticipate the Fed's easing cycle. Rate-sensitive sectors offer entry points now, but hedging against tariff and labor market volatility remains essential. As the Fed's terminal rate comes into focus, the mantra for 2025 is clear: act on the Fed's pivot, but do not ignore the shadows on the horizon.

Comentarios

Aún no hay comentarios