KeyCorp's Earnings Outlook and Strategic Positioning in a Shifting Interest Rate Environment

The regional banking sector is navigating a complex landscape shaped by tightening credit conditions, rising competition, and the lingering effects of high interest rates. KeyCorpKEY-- (KEY), a mid-sized player with a strong regional footprint, has demonstrated resilience in this environment, leveraging strategic initiatives and operational discipline to outperform peers. This analysis evaluates KeyCorp's earnings outlook and long-term positioning, drawing on recent financial performance, competitive dynamics, and industry trends.

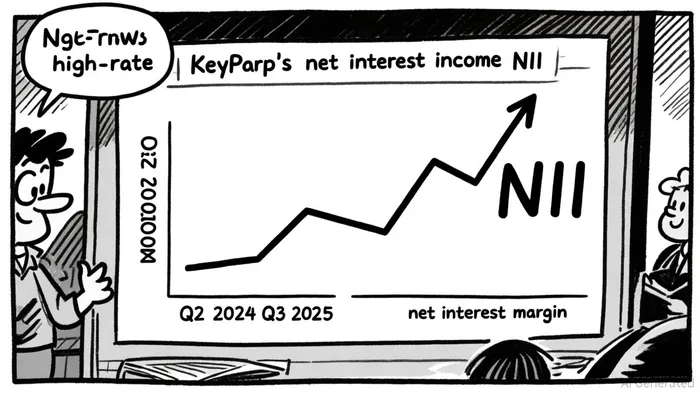

Earnings Resilience: NII Growth and NIM Expansion

KeyCorp's financial performance in Q2 2025 underscores its ability to adapt to a high-rate environment. Net interest income (NII) surged by 27.9% year-over-year to $1.15 billion, driven by a 62-basis-point expansion in the net interest margin (NIM) to 2.66%[2]. This outperforms the broader industry, where many regional banks struggle with margin compression due to lagging deposit rate adjustments. Management has raised full-year NIM guidance to 2.75% by late 2025, reflecting confidence in continued funding cost reductions and asset yield stability[1].

Fee-based revenue further bolsters earnings resilience. Non-interest income grew by 10% year-over-year in Q2 2025, fueled by investment banking and mortgage servicing activities[5]. Analysts project this trend to accelerate in Q3 2025, with NII expected to reach $1.18 billion, a 22.4% year-over-year increase. This diversification reduces reliance on traditional interest income, a critical advantage as interest rate volatility persists.

Loan Growth Challenges and Strategic Adjustments

While KeyCorp's NII growth is robust, loan dynamics remain mixed. Commercial loan balances rose by 5% year-to-date in Q2 2025, driven by demand in commercial real estate and corporate lending[5]. However, consumer loan runoff-particularly in auto and credit card portfolios-has led to a projected 2%-5% decline in average loan balances for 2025[2]. This aligns with broader industry trends, as regional banks grapple with weaker consumer credit demand amid tighter monetary policy.

KeyCorp's response has been to prioritize higher-margin commercial segments. For instance, its KeyVAM platform, a fintech-powered virtual account management solution, has processed nearly $9 billion in transactions since October 2024, enhancing fee income and client retention[1]. This strategic pivot toward commercial banking mitigates the drag from consumer loan declines and positions the bank to capitalize on corporate treasury management opportunities.

Strategic Positioning: Digital Transformation and Capital Flexibility

KeyCorp's long-term growth potential hinges on its ability to innovate and scale. A $2.8 billion capital injection from Scotiabank in 2025 has strengthened its balance sheet, elevating capital ratios and providing flexibility for strategic acquisitions or organic expansion[1]. This infusion aligns with a broader industry trend, as regional banks seek to enhance scale and efficiency in the face of fintech competition and regulatory pressures[3].

Digital transformation remains a cornerstone of KeyCorp's strategy. Collaborations with fintech partners like Qolo have enabled the bank to integrate advanced treasury solutions, while investments in AI-driven credit scoring and fraud detection improve operational efficiency[1]. These initiatives are critical in an era where customer expectations increasingly favor seamless digital experiences. According to a report by PwC, 78% of banking executives in 2025 cite digital transformation as a top priority, underscoring its role in competitive differentiation[4].

Competitive Dynamics and Risk Management

KeyCorp's Q2 2025 performance highlights its competitive edge. Revenue grew by 19.73% year-over-year, far outpacing the 2.34% industry average, while net income surged 41.97% compared to a contraction in peer earnings[2]. Its net margin of 22.98% also exceeds the industry average, reflecting superior cost management and pricing power[2]. However, rising credit risks-particularly in commercial real estate-pose challenges. The provision for credit losses increased by 16.9% quarter-over-quarter in Q2 2025, as management cited macroeconomic uncertainties[2].

To mitigate these risks, KeyCorp has adopted a cautious approach to credit underwriting. For example, it has extended loan maturities and utilized synthetic risk transfers (SRTs) to offload potential defaults in commercial real estate portfolios[3]. While SRTs introduce systemic interconnectedness, they allow KeyCorp to preserve capital while managing exposure to volatile sectors like office real estate.

Long-Term Outlook: Balancing Growth and Efficiency

KeyCorp's strategic initiatives position it well for long-term growth, but challenges remain. Rising operating expenses-driven by technology investments and personnel costs-could temper profitability in the near term. Non-interest expenses are projected to rise by 3.7% in 2025, a reversal of the 5.8% decline in 2024[5]. However, the bank's focus on fee-based revenue and digital efficiency gains should offset these pressures over time.

In a sector where regional banks are increasingly competing with fintechs for market share, KeyCorp's partnerships and AI integration provide a distinct advantage. As stated by Deloitte in its 2025 financial services predictions, banks that embrace embedded finance and customer-centric digital platforms will dominate the next decade[4]. KeyCorp's KeyVAM platform and embedded banking strategies align with this vision, enabling it to capture a larger share of the commercial banking market.

Conclusion

KeyCorp's earnings resilience in a high-rate environment, coupled with its strategic focus on digital transformation and capital optimization, positions it as a compelling long-term investment. While near-term challenges-such as loan runoff and credit risk-persist, the bank's proactive approach to diversification, technology, and risk management enhances its ability to navigate a shifting landscape. For investors, KeyCorp exemplifies how regional banks can thrive by balancing innovation with operational discipline in an era of uncertainty.

Comentarios

Aún no hay comentarios