Johnson & Johnson's 2025 Earnings Guidance Upgrade: A Test of Sustainable Growth and Long-Term Value

Johnson & Johnson's recent upgrade of its 2025 earnings guidance reflects a blend of resilience and strategic momentum. On July 16, 2025, the company raised its adjusted earnings per share (EPS) forecast to $10.80–$10.90 from $10.50–$10.70, according to a J&J press release. This revision underscores the company's ability to navigate headwinds, such as the loss of exclusivity for STELARA, while capitalizing on high-growth opportunities. For investors, the critical question is whether these drivers can sustain long-term value creation in an increasingly competitive and volatile healthcare landscape.

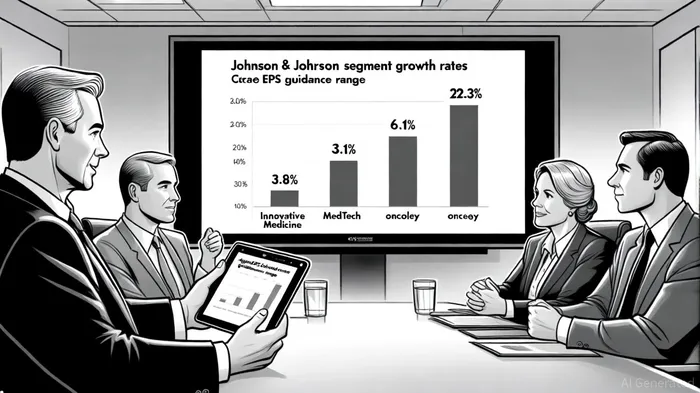

The Drivers Behind the Upgrade: Innovation and Diversification

The revised guidance is anchored in two pillars: oncology innovation and MedTech expansion. Johnson & Johnson's oncology franchise delivered 22.3% operational growth in Q2 2025, driven by blockbuster drugs like DARZALEX and the impending launch of TAR-200, according to a Nasdaq article. This segment's momentum is further bolstered by investigational therapies such as Bleximenib, which demonstrated an 82% overall response rate in acute myeloid leukemia trials, per the company press release. Such breakthroughs position J&J to capture market share in precision oncology, a sector projected to grow at a compound annual rate of 12% through 2030, according to a Protagonist report.

Meanwhile, the MedTech segment reported 6.1% operational growth, fueled by cardiovascular innovations and acquisitions like Abiomed, according to a Financhle article. This diversification is critical, as MedTech's resilience-less exposed to patent expirations than pharmaceuticals-provides a buffer against revenue erosion in other areas. For instance, the loss of STELARA exclusivity reduced growth by 710 basis points, yet the company offset this with gains in surgical and cardiovascular products, as noted in the Nasdaq piece.

R&D Pipeline and Competitive Positioning: A Foundation for Sustained Growth

Johnson & Johnson's long-term value hinges on its ability to translate R&D investments into market-leading therapies. The company's pipeline includes 20 new drugs targeting oncology, immunology, and neuroscience, with a focus on high-unmet-need areas, according to the Protagonist report. Bleximenib's potential to redefine AML treatment, for example, highlights J&J's edge in precision medicine. CEO Joaquin Duato has set an ambitious target of $50 billion in oncology sales by 2030, a goal now within reach given the current trajectory, per the company release.

Competitive advantages extend to MedTech, where J&J's acquisitions and product innovations (e.g., electrophysiology tools) align with demographic trends such as aging populations and post-pandemic medical procedure resumption, the Nasdaq piece observes. However, the segment faces margin pressures from supply chain inflation and regulatory scrutiny, which could temper growth if not managed effectively, the Nasdaq analysis also warns.

Risks to Sustainability: Patents, Litigation, and External Shocks

Despite these strengths, J&J's growth is not without vulnerabilities. The loss of exclusivity for key products like STELARA is a recurring risk, with biosimilar competition expected to intensify. Additionally, the company faces ongoing litigation, including talc-related settlements that have already impacted its financials, as covered by Nasdaq. While these challenges are material, J&J's diversified revenue streams and strong balance sheet (with $18 billion in cash reserves as of Q2 2025, per the company release) provide a buffer.

External risks, such as regulatory delays and economic downturns, also loom. For example, the FDA's approval timeline for TAR-200 could affect near-term revenue visibility. Moreover, cybersecurity threats-a growing concern in healthcare-pose operational risks that could disrupt supply chains or data integrity, a point highlighted in the Nasdaq coverage.

Long-Term Value Creation: Strategic Resilience and Global Access

Johnson & Johnson's focus on global patient access and AI-driven innovation offers a pathway to sustained value. The company has pledged to expand access to its therapies in emerging markets, where demand for affordable healthcare solutions is rising, according to the Protagonist report. This strategy not only enhances its social license to operate but also taps into growth markets with untapped potential.

Furthermore, J&J's integration of AI into drug discovery and manufacturing processes could reduce R&D costs and accelerate time-to-market for new therapies, the Protagonist coverage suggests. Such investments, combined with a disciplined approach to M&A, position the company to outperform peers in both innovation and operational efficiency.

Conclusion: A Cautious Optimism for Investors

Johnson & Johnson's 2025 guidance upgrade is a testament to its ability to adapt and innovate in a challenging environment. While the company's oncology and MedTech segments offer compelling growth trajectories, investors must remain vigilant about patent cliffs, litigation, and macroeconomic risks. However, J&J's robust R&D pipeline, strategic acquisitions, and focus on global access suggest that its long-term value creation is not merely aspirational but grounded in tangible capabilities. For those willing to balance optimism with caution, the current upgrade may signal a resilient, if not entirely risk-free, investment opportunity.

Historical backtesting of JNJ's earnings-beat events from 2022 to 2025 reveals a pattern of sustained outperformance. Over 41 such events, the stock generated a cumulative excess return of +5.35% over 30 days compared to a +0.37% benchmark. Statistically significant outperformance emerged from Day 13 onward, with a win rate climbing to ~66-75% through Day 29, as shown by a historical backtest. This suggests that a buy-and-hold strategy following earnings surprises has historically rewarded investors with gradual, compounding gains-though ~34% of events still underperformed, underscoring the need for risk management.

Comentarios

Aún no hay comentarios