Three Habits to Build Long-Term Wealth: Discipline, Rebalancing, and Time

The relentless pursuit of wealth creation often leads investors to chase the next big idea, the perfect timing, or the elusive “winning” stock. Yet, the most financially successful individuals—those who build true, enduring wealth—rely on principles that defy the noise of the markets. These principles are rooted in behavioral finance, historical data, and an understanding of human psychology. Let us explore three habits that separate the disciplined from the reactive, and the patient from the impulsive.

1. Disciplined Investing: The Power of Consistency Over Timing

The first habit is dollar-cost averaging (DCA)—a strategy that turns volatility into an ally. By investing fixed amounts at regular intervals, regardless of market conditions, DCA minimizes the emotional and financial risks of trying to “time” the market. Historical data reveals why this works:

- Over 97 years (1928–2025), the S&P 500 delivered a 9.96% annualized return, but inflation-adjusted returns (6.69%) show that compounding growth requires patience.

- A study tracking five hypothetical investors over 20 years (2003–2022) found that Matthew Monthly, who used DCA, ended with $124,248—third-highest behind only Peter Perfect (a mythical perfect market timer) and Ashley Action (who invested everything upfront). Crucially, even Rosie Rotten, who invested at annual peaks, outperformed Larry Linger, who stayed in cash.

Why It Works:

- Loss aversion drives many to delay investing after declines, but DCA forces participation in recoveries.

- Mental accounting tricks us into overvaluing “winning” stocks, but DCA avoids the trap of overconcentration.

Actionable Advice:

- Start early and automate contributions to retirement accounts or index funds.

- Avoid the illusion of control: No one consistently outperforms DCA without insider knowledge.

2. Rebalancing: The Quiet Engine of Diversification

The second habit is regular portfolio rebalancing, a practice that counteracts the natural drift toward risk concentration. Over time, markets reward a few winners disproportionately, leaving buy-and-hold portfolios exposed to sector or stock-specific risks. Rebalancing resets exposure, ensuring diversification persists.

- A rebalanced portfolio of 50 stocks, adjusted annually, had a 63% chance of outperforming the S&P 500 over 30 years. Even with transaction costs (80 basis points), this rose to 88%.

- The “Magnificent Seven” tech stocks (e.g., AppleAAPL--, Amazon) now account for 33.5% of the S&P 500's market cap, mirroring pre-dot-com bubble concentration. Rebalancing avoids overexposure to such clusters.

Why It Works:

- Mental accounting tempts investors to cling to “winning” stocks, ignoring rebalancing.

- Loss aversion makes sellers hesitate after declines, but rebalancing forces disciplined sales of overvalued assets.

Actionable Advice:

- Rebalance annually, trimming winners and adding to undervalued holdings.

- Simplify with a 4-Fund Strategy: U.S. Large-Cap Blend, U.S. Small-Cap Value, International Large-Cap Value, and International Small-Cap Blend.

3. Long-Term Compounding: Let Time Do the Heavy Lifting

The third habit is commitment to long-term compounding, a mathematical force that transforms small, consistent contributions into wealth.

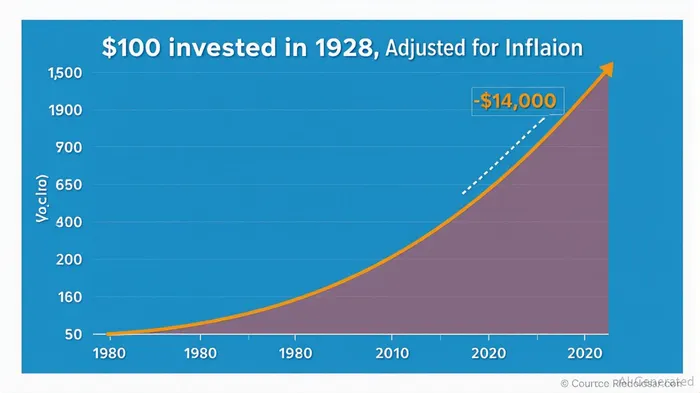

- A $100 investment in the S&P 500 in 1957 grew to $82,000 by 2025 (nominal) but retained $7,100 in inflation-adjusted purchasing power. The real lesson: time is the most powerful lever.

- The S&P 500's longest bull market (2009–2020) saw a 330% gain, but those who panicked during the 2008 crash missed the recovery.

Why It Works:

- Loss aversion drives short-term panic, but compounding requires ignoring noise.

- Mental accounting divides investments into “winning” and “losing” buckets, but compounding works best when left uninterrupted.

Actionable Advice:

- Avoid frequent trading. The average investor underperforms the S&P 500 by 1–2% annually due to timing errors.

- Think in decades, not years.

Conclusion: The Psychology of Wealth

The three habits—disciplined investing, rebalancing, and long-term compounding—are not rocket science. They are battle-tested strategies that leverage human psychology against itself. Loss aversion tempts us to avoid losses, but DCA and rebalancing turn that fear into discipline. Mental accounting tricks us into overvaluing “winners,” but rebalancing resets priorities.

The markets will always offer distractions—AI booms, crypto hype, geopolitical fears—but the path to wealth remains clear. Start early, stay consistent, and let time work for you. As the data shows, reactive decisions fade, but patience compounds.

In the end, the greatest wealth is built not by timing the market, but by mastering oneself.

Data queries and visualizations can be generated via platforms like FRED, Yahoo Finance, or Morningstar using the specified parameters.

Comentarios

Aún no hay comentarios