Ghana's Economic Renaissance: Sovereign Debt and Equity Plays in Africa's New Growth Story

The International Monetary Fund's recent approval of Ghana's fourth review under its Extended Credit Facility (ECF) marks a pivotal moment for the West African nation. After years of fiscal strain, currency volatility, and debt overhang, Ghana has emerged as a poster child for macroeconomic stabilization in Sub-Saharan Africa. With a projected 4.0% GDP growth in 2025, improving debt metrics, and structural reforms unlocking value in key sectors, the country is poised to attract a new wave of investment. For investors seeking high-risk-adjusted returns in frontier markets, Ghana presents a compelling opportunity—one where disciplined policy reforms are converging with rising reserves and credible institutions to create a durable turnaround.

The IMF's Seal of Approval: Fiscal Discipline and Debt Sustainability

The IMF's progress review underscores Ghana's adherence to stringent fiscal targets, a critical step toward rebuilding investor confidence. The government's commitment to achieving a 1.5% of GDP primary fiscal surplus in 2025, up from 0.5% in 2024, reflects a hard-won fiscal responsibility framework. This includes audits to resolve 2024 fiscal slippages, expenditure rationalization, and protections for social safety nets. Crucially, the IMF's blessing ensures continued disbursements under the $3 billion ECF program, with $367 million released in July 2025 alone.

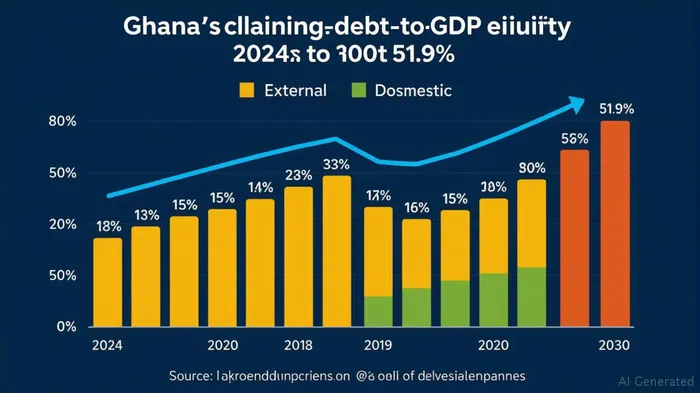

The debt restructuring process has also advanced significantly. Gross public debt is projected to fall from 78% of GDP in 2024 to 51.9% by 2030, driven by a decline in external debt (from 44.5% to 33.4% of GDP) and progress in aligning terms with creditors under the G20 Common Framework. By 2025, Ghana has eliminated external arrears, a milestone that reduces default risk and opens the door for sovereign debt to regain its appeal.

Macro Stabilization Fuels Sectoral Growth Opportunities

Ghana's stabilization is not merely a fiscal exercise; it is a catalyst for growth in sectors ripe for investment. Three areas stand out:

Mining and Commodities: Ghana is Africa's second-largest gold producer and a top cocoa exporter. With gold prices near record highs and the mining sector contributing 6.3% to GDP in 2024, companies like AngloGold AshantiAU-- and local firms such as Golden Star Resources are beneficiaries of stable policies and rising reserves. The Bank of Ghana's rebuilding of foreign exchange reserves to 3.3 months of imports by 2025—surpassing the IMF's 3-month target—reduces currency risk for miners.

ICT and Financial Inclusion: Ghana's tech sector is booming, fueled by mobile money adoption (penetration at 75%) and a youthful, digitally native population. Companies like MTN Ghana and Ecobank, which dominate telecoms and banking, are well-positioned to capitalize on rising digital payments and fintech innovation.

Infrastructure and Construction: Public-private partnerships (PPPs) are accelerating road, port, and energy projects. The government's focus on resolving energy sector arrears—critical to reducing fiscal drag—creates opportunities in utilities, while infrastructure upgrades will lower logistics costs for manufacturers and exporters.

The Investment Case: Sovereign Debt and Equity Plays

For investors, Ghana's turnaround presents two distinct avenues:

Sovereign Debt: A Post-Restructuring Bargain

Ghana's sovereign bonds, once shunned due to debt restructuring uncertainty, now offer a compelling entry point. The completion of Eurobond exchanges and elimination of external arrears by 2025 removes a major overhang. With inflation projected to fall to 8.0% by 2026 from 17.3% in 2025, real yields on Ghanaian bonds are likely to rise. Investors should target long-dated debt with maturities beyond 2030, benefiting from the declining debt-to-GDP trajectory and improved creditworthiness.

Equity: Sector-Specific Winners

Equities in mining, ICT, and infrastructure offer higher risk-adjusted returns but require sectoral discernment. Investors should prioritize:

- Mining stocks: Exposure to gold and cocoa via Ghanaian firms or multinationals with local operations.

- Telecoms and banking: Firms like MTN Ghana and Ecobank, which benefit from rising digital adoption and stable macro conditions.

- Infrastructure funds: PPP projects in energy and transportation, though due diligence on contractual terms is essential.

Risks and the Path Ahead

Ghana's journey is not without hurdles. Persistent energy sector inefficiencies, election-related fiscal pressures, and global commodity price volatility pose risks. Investors must monitor the energy sector reform timeline and ensure the government maintains fiscal discipline amid 2028 elections.

Conclusion: A New Dawn for Patient Capital

Ghana's stabilization is no flash in the pan. The IMF's validation, coupled with structural reforms and rising reserves, signals a durable shift toward macroeconomic health. For investors, the convergence of improving fundamentals, credible institutions, and sectoral dynamism creates a rare frontier market opportunity. Sovereign debt, once a liability, is now a gateway to asymmetric risk-reward, while equities in mining, tech, and infrastructure offer growth catalysts. As Ghana's economy rebalances, the rewards for patient capital are clear—but the window for entry is narrowing.

Invest wisely.

Comentarios

Aún no hay comentarios