The Fragile Foundation of U.S. Inflation Metrics: Politicalization and Market Implications

The credibility of U.S. core inflation metrics has become a focal point of economic and political debate in 2025, as the Bureau of Labor Statistics (BLS) faces unprecedented scrutiny. The agency's recent leadership changes, coupled with methodological challenges, have raised urgent questions about the reliability of data that underpin Federal Reserve policy and global market positioning. For investors, the implications are clear: a fractured statistical foundation risks distorting inflation expectations, complicating central bank decisions, and amplifying market volatility.

The BLS in the Crosshairs

The BLS, long regarded as a nonpartisan arbiter of economic reality, has become a lightning rod for political controversy. President Donald Trump's abrupt removal of Erika McEntarfer, the BLS commissioner, following a weak July 2025 jobs report—marked by a historically large downward revision—has intensified concerns about politicization. The subsequent nomination of E.J. Antoni, a Heritage Foundation economist and architect of Project 2025, has further eroded confidence. Antoni's public criticism of BLS methodologies and his alignment with a conservative policy agenda suggest a potential shift in the agency's operational independence.

This politicization is not merely symbolic. The BLS's role in compiling the Consumer Price Index (CPI) and employment data is foundational to the Federal Reserve's inflation targeting strategy. Yet, the agency's credibility is now entangled with political narratives, as seen in Trump's accusations of “rigged” data. Such claims, though baseless, resonate in a climate where trust in institutions is already fragile.

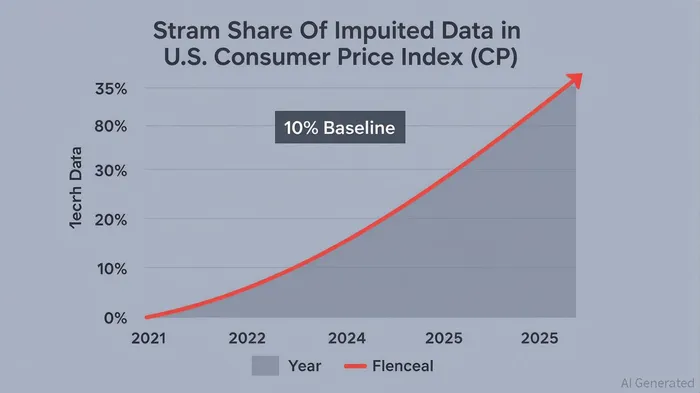

The Imputation Dilemma

Compounding these concerns is the BLS's growing reliance on statistical imputation to fill data gaps. Budget cuts and declining survey response rates—now below 45%—have forced the agency to impute 35% of CPI data in 2025, up from 10% in 2021. While imputation is a standard statistical tool, its overuse introduces volatility and uncertainty. For instance, “different cell imputation,” which borrows data from unrelated geographic areas, risks distorting regional price trends. This methodological shift, combined with reduced sample sizes, has made inflation metrics more susceptible to revision and less reflective of real-time economic conditions.

The Federal Reserve's June 2025 Monetary Policy Report acknowledges these challenges, noting that inflation has eased but remains uneven. Core PCE prices, at 2.5%, hover above the 2% target, while alternative measures like the trimmed mean PCE suggest inflation may stay elevated. Yet, the Fed's reliance on BLS data is now clouded by methodological doubts. If imputed data overstates or understates price trends, the Fed's policy response could misalign with actual economic conditions, risking either premature easing or unnecessary tightening.

The Fed's Adaptive Strategy

Faced with this uncertainty, the Federal Reserve has adopted a multi-pronged approach to validate its policy decisions. Officials like St. Louis Fed President Alberto Musalem have emphasized cross-checking BLS data with alternative sources, including private-sector surveys, administrative records (e.g., unemployment insurance claims), and real-time indicators like consumer spending analytics. The Beige Book, a qualitative assessment of economic conditions, has also gained prominence as a counterbalance to statistical volatility.

However, the Fed's ability to navigate this landscape is not without limits. Minneapolis Fed President Neel Kashkari's assertion that “economic reality cannot be faked” underscores a philosophical stance: businesses and households will ultimately reveal the true state of the economy through hiring, spending, and wage trends. Yet, in a world where data is increasingly politicized, the Fed must contend with the risk of delayed or distorted signals.

Investment Implications

For investors, the erosion of data credibility demands a recalibration of risk management strategies. Three key considerations emerge:

Hedging Against Inflation Uncertainty: With inflation expectations diverging between short-term (5.1% in June 2025) and long-term (2.8%) measures, investors should prioritize assets that protect against volatility. Treasury Inflation-Protected Securities (TIPS), commodities like gold, and real estate investment trusts (REITs) offer asymmetric upside in a high-uncertainty environment.

Diversifying Data Sources: The rise of alternative data—such as real-time hiring platforms, consumer foot traffic analytics, and supply chain metrics—provides a more granular view of economic activity. Hedge funds and asset managers are already allocating capital to these tools, with the global alternative data market projected to grow from $18.74 billion in 2025 to $135.8 billion by 2030.

Positioning for Policy Shifts: The Fed's potential rate cuts in September 2025 (85% probability) and beyond could drive a rotation into cyclical sectors like industrials and consumer discretionary. However, investors should remain cautious, as a delayed policy response to inflation could reignite volatility.

Conclusion

The U.S. inflation data landscape in 2025 is defined by a fragile interplay of political pressures, methodological challenges, and institutional resilience. While the Federal Reserve's adaptive strategies offer a buffer, the politicization of the BLS threatens to undermine the very foundation of economic policymaking. For investors, the path forward lies in hedging against uncertainty, diversifying data inputs, and maintaining a disciplined focus on long-term fundamentals. In an era where trust in data is eroding, the ability to navigate ambiguity will separate prudent investors from the rest.

Comentarios

Aún no hay comentarios