U.S. Fiscal Uncertainty and the Fragility of Global Debt Markets

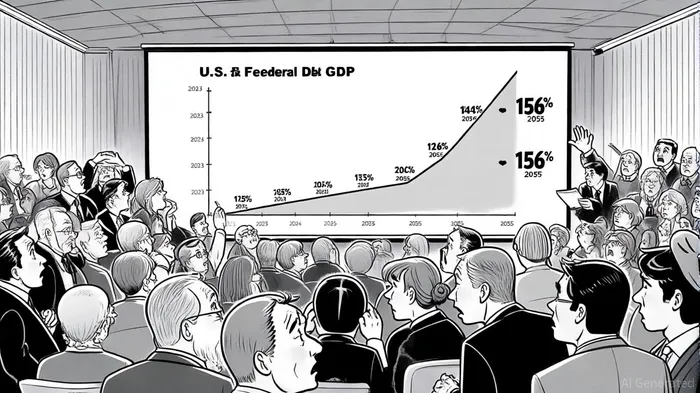

The United States' fiscal trajectory has become a defining source of global economic instability. As the federal debt-to-GDP ratio surges toward 125% by 2034 and 156% by 2055, the implications for high-yield and emerging market debt are profound. Fiscal uncertainty, driven by escalating deficits, political gridlock, and the compounding costs of servicing a bloated debt load, has created a ripple effect across global capital markets. Investors in high-yield bonds and emerging market debt now face a landscape where U.S. policy volatility is not just a background risk but a central determinant of returns and defaults.

The High-Yield Debt Conundrum

High-yield bond markets, long sensitive to shifts in credit conditions, have borne the brunt of U.S. fiscal uncertainty. According to a report by Moody'sMCO--, the average default risk for U.S. public companies reached 9.2% at the end of 2024—the highest level since the global financial crisis[4]. This surge coincides with the Congressional Budget Office's (CBO) projection that federal debt held by the public will rise to 117% of GDP over the next decade[2]. The Federal Reserve has noted that trade and economic policy uncertainties have historically led to delayed corporate investment and tighter credit conditions[1], exacerbating the fragility of leveraged firms.

The mechanism is clear: as fiscal uncertainty rises, investors demand higher risk premiums for high-yield debt. Credit spreads have widened accordingly, with the average yield on junk bonds climbing to 6.5% in mid-2025, up from 4.8% in early 2023[1]. This tightening of credit conditions is further compounded by the Hutchins Center Fiscal Impact Measure, which found that fiscal policy reduced U.S. GDP growth by 0.4 percentage points in Q2 2025, primarily due to declining federal purchases[5]. For high-yield issuers, the combination of higher borrowing costs and weaker economic growth creates a dangerous feedback loop, increasing the likelihood of defaults and downgrades.

Emerging Markets: A Double-Edged Sword

Emerging markets face a more complex interplay of risks and opportunities. On one hand, U.S. fiscal uncertainty has amplified capital outflows and currency depreciation. Research from the Dallas Fed highlights that each percentage point increase in the U.S. debt-to-GDP ratio raises long-term interest rates by 3 basis points[3], a dynamic that reverberates globally. For instance, the U.S. dollar weakened significantly in 2025, driven by slower growth, rising deficits, and policy uncertainty[4]. This depreciation prompted European investors to reallocate capital away from U.S. assets, exacerbating downward pressure on the dollar and reshaping global investment flows[4].

On the other hand, the global macroeconomic environment has shown unexpected resilience. Anticipated Federal Reserve rate cuts in 2025 have eased financial conditions, providing some relief to emerging markets. Capital Group's analysis notes that countries with strong fiscal frameworks and flexible monetary policies—such as India and Indonesia—have navigated this turbulence more effectively than peers with weaker institutions[5]. However, the spillover effects of U.S. fiscal policy remain severe. A study published in Emerging Markets Review found that tightening U.S. monetary policy, when paired with heightened policy uncertainty, leads to heterogeneous spillovers: reduced output growth, lower inflation, and significant currency depreciation in vulnerable economies[3].

The Fiscal “Precipice” and Market Implications

The bond market itself has become a fiscal “check” on U.S. spending, with yields rising as a signal of growing investor skepticism. Reuters reports that if U.S. borrowing costs remain elevated, interest payments on the national debt could exceed 30% of federal revenue, pushing the country closer to a fiscal precipice[3]. This dynamic has already strained global markets, as political instability in countries like France and Japan—combined with their own fiscal profligacy—has led to rising bond yields and increased sovereign risk[5].

For investors, the lesson is clear: diversification and hedging are no longer optional. High-yield bonds and emerging market debt, while historically offering higher returns, now require careful scrutiny of macroeconomic linkages. The Federal Reserve's own analysis underscores that trade policy uncertainty (TPU) has caused firms to delay supply chain adjustments and avoid market expansion[1], a trend that will likely persist until fiscal clarity emerges.

Conclusion

U.S. fiscal policy uncertainty has become a systemic risk, reshaping the risk-return profiles of high-yield and emerging market debt. While the Federal Reserve and global policymakers have taken steps to mitigate fallout—such as anticipated rate cuts and fiscal stimulus—the underlying fragility remains. Investors must navigate this landscape with a dual focus: hedging against U.S. fiscal volatility while identifying emerging markets with robust fundamentals. As the Hutchins Center warns, the cost of inaction is rising[5]. In an era of interconnected capital flows, fiscal prudence is no longer a national concern but a global imperative.

Comentarios

Aún no hay comentarios