Dynex Capital Inc: A Beacon of Resilience in a Challenged Mortgage REIT Sector

The recent upgrade of Dynex CapitalDX-- (DX) by Keefe, Bruyette & Woods (KBW) from a $12.50 to $13.00 price target, while maintaining an "Outperform" rating, reflects a nuanced optimism in a sector grappling with macroeconomic headwinds. This adjustment, a 4% increase in the anticipated stock value, underscores KBW's confidence in Dynex's ability to navigate the volatile mortgage REIT landscape, according to a KBW upgrade. To understand the significance of this upgrade, one must examine both the sector's broader dynamics and Dynex's unique positioning within it.

Sector-Wide Challenges and Opportunities

The mortgage REIT sector in 2025 faces a dual challenge: declining earnings and heightened interest rate risks. According to J.P. Morgan research, U.S. mortgage REITs have seen a 31% annual decline in earnings over the past three years, while their price-to-earnings (P/E) ratio has ballooned to 26.2x-well above the 3-year average of 18.6x. This disconnect between valuation and performance highlights investor skepticism about the sector's ability to sustain returns in a high-rate environment. Compounding these issues, leverage-a traditional lever for REITs-has become a double-edged sword as rising borrowing costs compress net interest margins.

Yet, within this turbulence, pockets of resilience emerge. Firms like Starwood Property Trust and AGNC Investment Corp. have adapted by diversifying their portfolios and refining hedging strategies. For instance, AGNC's focus on government-backed mortgage-backed securities has allowed it to maintain a 14.6% dividend yield despite a 5.3% decline in tangible book value, as an Investing.com analysis notes. Such adaptability suggests that while the sector's fundamentals are strained, strategic agility can still unlock value.

Dynex Capital: A Case of Strategic Differentiation

Dynex's recent performance exemplifies this strategic agility. The company's disciplined "raise and deploy" model has driven a 50% year-over-year expansion of its Agency MBS portfolio to $14 billion, supported by $560 million in new capital raised at a premium to book value, according to a BeyondSpx analysis. This growth has translated into robust net interest income, which surged to $23.1 million in Q2 2025 from $17.1 million in the prior quarter. Such operational strength is rare in a sector where net losses are increasingly common.

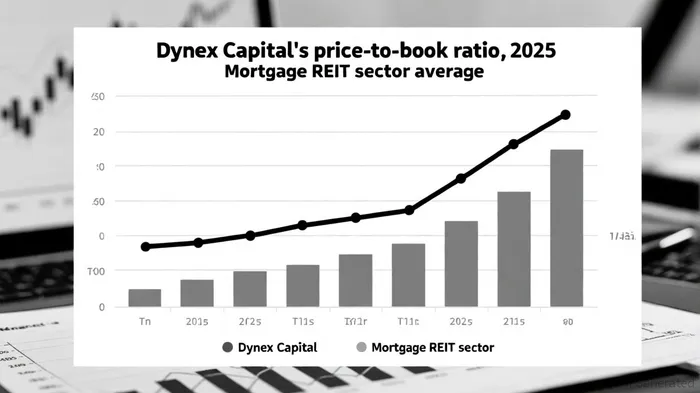

Valuation metrics further highlight Dynex's appeal. While the sector trades at an average P/B ratio of 3.02, Dynex's P/B stands at a mere 1.1, suggesting significant undervaluation relative to peers, as a Nasdaq article reports. This discount is even more striking when juxtaposed with its 16% dividend yield-a figure that dwarfs the sector's median yield of 10.9% (Nasdaq). For income-focused investors, this combination of low valuation and high yield is compelling, particularly in a market where traditional fixed-income alternatives offer paltry returns.

The KBW Upgrade: Justified by Fundamentals?

KBW's upgraded price target for Dynex-from $12.50 to $13.00-aligns with broader analyst sentiment, as the stock now carries a consensus 12-month target of $13.00 and a "Moderate Buy" rating (KBW). This optimism is grounded in Dynex's ability to generate mid-teens to low-20s returns on equity (ROEs) from newly acquired positions, despite a $16.3 million derivative loss in Q2 2025. Management's emphasis on a capital structure prioritizing common equity issuance also signals a commitment to preserving shareholder value amid volatile hedging costs.

However, risks remain. Dynex's book value per share has declined from $12.56 to $11.95 since year-end 2024, reflecting the dilutive impact of its aggressive capital-raising strategy. Investors must weigh this against the company's long-term growth prospects and its capacity to sustain its 15.7% annualized dividend yield.

Conclusion: A Calculated Bet in a Cyclical Sector

The KBW upgrade of Dynex Capital is not merely a vote of confidence in the company but a tacit acknowledgment of its superior risk management in a sector defined by volatility. While mortgage REITs face structural challenges-particularly in a high-rate environment-Dynex's strategic focus on high-yielding Agency RMBS, disciplined leverage, and shareholder-friendly capital policies position it as a standout. For investors willing to navigate the sector's cyclical nature, Dynex offers a rare blend of income potential and valuation appeal.

As the Federal Reserve's policy trajectory remains uncertain, the mortgage REIT sector will likely continue to experience turbulence. Yet, as the adage goes, "a falling knife can sometimes be caught"-and in this case, Dynex Capital may just be the right candidate.

Comentarios

Aún no hay comentarios