The Credit Scoring Shake-Up: FICO's Disruption and TransUnion's Strategic Reckoning

The credit scoring industry, long characterized by its oligopolistic stability, has been thrown into disarray by Fair Isaac Corporation's (FICO) October 2025 launch of the Mortgage Direct License Program. This move, which allows mortgage lenders and tri-merge resellers to access FICOFICO-- Scores directly from the company-bypassing credit bureaus like TransUnion-has upended traditional revenue streams and forced a reevaluation of competitive dynamics. For TransUnionTRU--, the implications are profound, both strategically and financially.

FICO's Disruption: A Direct Challenge to Credit Bureau Margins

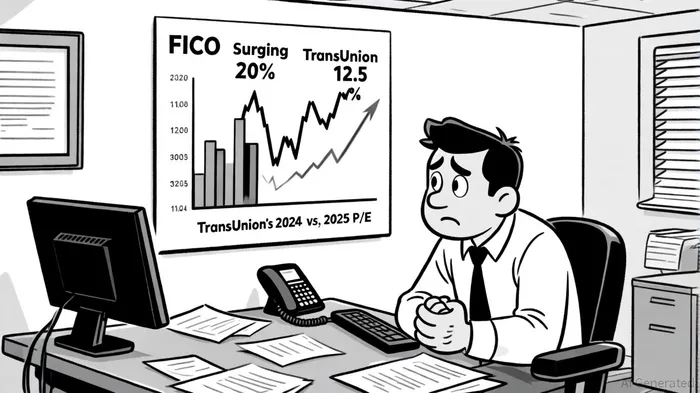

FICO's new pricing model offers two options: a performance-based structure with a $4.95 per-score fee and a $33 funded-loan fee, or a flat $10 per-score rate. By eliminating the mark-ups historically added by credit bureaus, FICO has directly targeted the intermediary role of companies like TransUnion. According to a Reuters report, this shift could reduce credit bureau earnings by 10% to 15%. The market reacted swiftly: FICO's shares surged over 20%, while TransUnion's stock plummeted 12.5% on October 2, 2025, according to a FinancialContent report.

The move aligns with regulatory pressures for greater transparency in mortgage lending. FHFA Director Bill Pulte praised the initiative as a step toward "greater competition and cost efficiency" in a Times article. However, TransUnion has criticized FICO's approach, arguing that the new pricing structure "undermines recent efforts to reduce costs for consumers" and ignores the data infrastructure provided by credit bureaus in a TransUnion statement.

TransUnion's Strategic Counterplay: Diversification and Innovation

Faced with a shrinking margin in its core mortgage scoring business, TransUnion has pivoted toward international expansion, technological modernization, and product diversification. A key move was the $560 million acquisition of Trans Union de Mexico, which is expected to generate $145 million in revenue and $70 million in Adjusted EBITDA in 2024, as reported in a CanvasBusinessModel article. This acquisition cements TransUnion's position in Latin America, where international operations now contribute 35% of total revenue, according to a product strategy guide.

Simultaneously, the company has invested heavily in its OneTru platform, a digital infrastructure aimed at improving operational efficiency and enabling AI-driven analytics. These investments are projected to yield $200 million in free cash flow improvements by 2026, as Monexa projected. TransUnion has also launched TrueView AI, an advanced credit scoring tool that integrates alternative data sources, and MyTransUnion, a consumer portal offering credit monitoring and identity protection, detailed in the Q2 2025 earnings transcript. These innovations aim to reposition TransUnion as a data-driven insights provider rather than a mere score intermediary.

Valuation Implications: A Market in Reassessment

The financial impact of FICO's disruption is evident in TransUnion's valuation metrics. As of October 2025, its P/E ratio has fallen sharply from 63.25 in 2024 to 20.31, reflecting investor skepticism about its ability to maintain margins, per Macrotrends data. Its market capitalization has also declined from $18.069 billion in 2024 to $14.32 billion in 2025, according to MarketScreener valuation. Analysts warn that the 10–15% earnings erosion from FICO's direct licensing model could persist unless TransUnion successfully monetizes its non-credit offerings.

Yet, TransUnion's Q2 2025 results suggest resilience. The company reported $1.14 billion in revenue, a 10% year-over-year increase, and raised full-year guidance to 6–7% growth in its Q2 2025 results. Non-credit products now account for 45% of total revenue, up from 30% in 2020, according to TransUnion's Q2 2025 CIIR. This diversification, coupled with disciplined capital allocation (including $47 million in share repurchases in 2025, per a Panabee report), provides a buffer against sector-specific shocks.

Historical data on TransUnion's earnings performance further underscores its potential to deliver value. A backtest of TRU's stock performance following earnings beats from 2022 to 2025 reveals that 72% of such events delivered positive returns within 30 days, with an average cumulative return of +6.5%-significantly outperforming the benchmark's +0.3%-as noted in an MPA Magazine article. This suggests that the market has historically rewarded TransUnion's ability to exceed expectations, even amid sector headwinds.

The Path Forward: Navigating a Fragmented Landscape

For investors, the key question is whether TransUnion can sustain its strategic pivot. Its focus on AI, international markets, and non-credit services offers a plausible path to offsetting FICO's disruption. However, the company's success will depend on its ability to innovate faster than its peers and capture value in emerging verticals such as digital identity verification and auto loan risk assessment. TransUnion's advocacy for a "system that benefits all market participants" in a TransUnion statement may yet position it as a collaborator in this new ecosystem, but the road ahead remains fraught with uncertainty.

In the short term, TransUnion's stock appears undervalued relative to its long-term growth prospects. Yet, the company's ability to execute its transformation will determine whether this undervaluation is a buying opportunity or a warning sign. As the credit scoring industry redefines itself, the battle between intermediaries and direct providers will likely shape the sector's trajectory for years to come.

Comentarios

Aún no hay comentarios