The Auto Finance Crisis: Unmasking Systemic Vulnerabilities and Fraud in 2025

The U.S. auto finance industry is teetering on the edge of a systemic collapse, driven by a perfect storm of escalating fraud, economic fragility, and regulatory complacency. According to a Point Predictive report, auto lenders faced an estimated $9.2 billion in fraud loss exposure in 2024-a 16.5% year-over-year increase and the highest figure in history. This surge is not merely a byproduct of individual misconduct but a symptom of deeper structural weaknesses in lending practices, exacerbated by technological innovation in the hands of fraudsters.

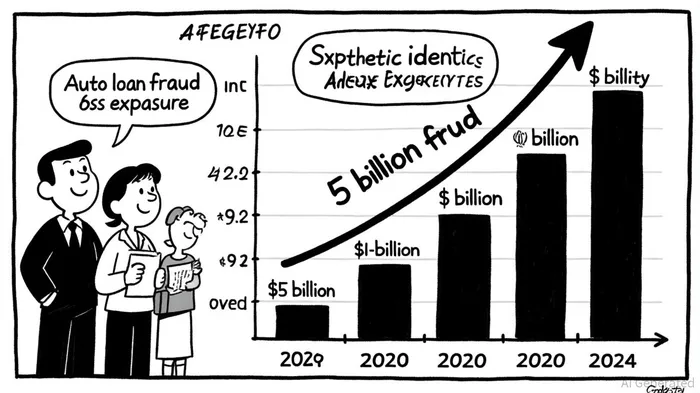

The Escalating Fraud Crisis

First-party fraud now accounts for 69% of systemic risk in auto finance, with income and employment misrepresentation alone contributing $3.9 billion to total losses, according to Point Predictive. Credit washing-a practice where borrowers manipulate their credit histories to appear more creditworthy-has surged by 162% year-over-year, while synthetic identity fraud has grown to 88 basis points, nearly double the 2020 rate, as reported by Frank on Fraud. These tactics are increasingly sophisticated: criminal networks now use AI-generated deepfakes and synthetic identities to bypass identity verification systems, with discussions about AI-driven fraud tools rising 644% on platforms like Telegram, Point Predictive adds.

The Federal Trade Commission (FTC) data underscores the gravity of the situation. In Q1 2025 alone, 21,400 complaints were filed regarding fraudulent auto loans-a 43% increase compared to the full year of 2024 (reported by Frank on Fraud). These scams often involve fake dealership websites and social media listings, preying on consumers' trust in digital marketplaces. For instance, Brooklyn resident Steven Simon discovered his identity had been stolen to co-sign an unauthorized lease, highlighting how fraudsters exploit vulnerabilities in credit reporting systems, as CBS News reported.

Systemic Vulnerabilities in Auto Finance

Beyond fraud, the auto finance sector is grappling with broader economic pressures. Auto loan balances have ballooned to $1.7 trillion, with 82% of buyers paying above market value during the pandemic-era buying frenzy, Point Predictive finds. As these vehicles depreciate, negative equity has become rampant: some borrowers now owe $10,000–$14,000 more than their cars are worth, Point Predictive warns. This imbalance is compounded by rising monthly payments-$750 for new cars and $540 for used-placing immense strain on households as pandemic-era stimulus and forbearance programs expire, according to an OpenLending analysis.

Delinquency rates have reached record levels, with the 60+ day delinquency rate hitting 1.38% in Q1 2025, exceeding the 2009 peak of 1.33%, as noted in a USA Today report. Subprime delinquencies are particularly alarming, reaching 6.6% in January 2025-the highest since 1994, the OpenLending analysis adds. Repossessions are also surging, with 1.73 million vehicles repossessed in 2024, the highest rate since the financial crisis, the USA Today piece reports. These trends reflect a sector where traditional recovery models are obsolete; lenders now face a lopsided portfolio structure marked by high risk, low volume, and inadequate tools to mitigate losses, Point Predictive argues.

The Perfect Storm: Fraud and Economic Pressures

The convergence of fraud and economic fragility creates a self-reinforcing cycle of risk. For example, dealerships inflating car values and falsifying employment details have increased lenders' default risk by up to 500%, Point Predictive estimates. Meanwhile, early payment defaults-often a harbinger of fraud-have risen 25% over two years, with 70% of these cases involving misrepresentation, the OpenLending analysis finds. Bust-out fraud, where borrowers max out credit lines with no intention of repayment, has also increased by 26%, reflecting broader financial desperation, Point Predictive reports.

Regulatory oversight has further eroded confidence. Agencies like the Consumer Financial Protection Bureau (CFPB) and FTC have scaled back enforcement of predatory lending practices, leaving borrowers and lenders alike exposed, the USA Today piece contends. This regulatory vacuum has emboldened fraudsters and dealerships alike, creating an environment where unethical behavior thrives.

Mitigation Strategies and the Path Forward

To navigate this crisis, lenders must adopt advanced fraud detection tools and agile data strategies. Point Predictive's AutoPass™ and IEValidate™, for instance, leverage AI-driven analytics to reduce early payment defaults by 40–60% while streamlining approvals, Point Predictive notes. Similarly, real-time tracking and early intervention are critical for managing asset movement in a volatile market, the USA Today analysis suggests.

Investors, however, must remain cautious. The auto finance sector's systemic vulnerabilities-ranging from inflated loan balances to regulatory neglect-pose long-term risks that extend beyond fraud. While technological solutions offer partial relief, they cannot address the root causes of economic strain and misaligned incentives. A comprehensive overhaul of lending practices, coupled with stronger regulatory scrutiny, is essential to prevent a repeat of the 2008-style collapse.

In the absence of such reforms, the auto finance industry will continue to hemorrhage value, with borrowers, lenders, and investors bearing the brunt of a crisis that was long in the making.

Comentarios

Aún no hay comentarios