Amber International: Margin Powerhouse in the Crypto Institutional Surge – Strong Buy with 80% Upside

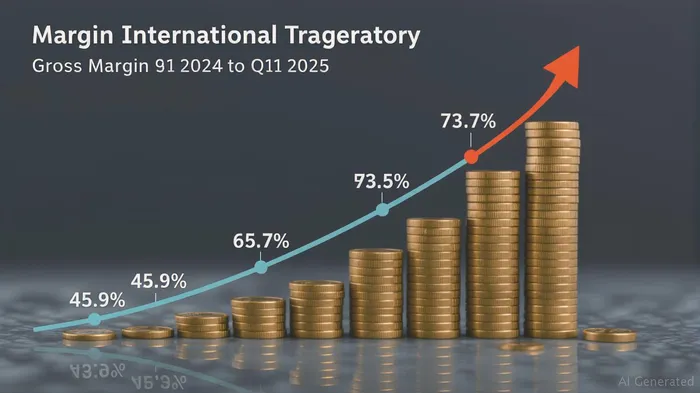

Amber International Holding Limited (NASDAQ: AMBR) is a rare gem in the crypto sector: a company whose margin expansion and strategic positioning are being grossly underappreciated by the market. Despite a 1,378% surge in revenue in Q1 2025 and a gross margin leap to 73.7%—up from 45.9% a year ago—the stock trades at $8.60, far below its intrinsic value. This article argues that AMBR's operational discipline, sector tailwinds, and leadership in institutional crypto services justify a Strong Buy rating with an 80% upside. The market's focus on near-term volatility and technical headwinds obscures a compelling growth story.

Margin Expansion: The Silent Engine of Value Creation

AMBR's margin improvement is not merely cyclical but structural. In Q1 2025, gross profit soared to $11.0 million, a 2,272% rise from $0.5 million in 2024. This reflects two critical factors:

1. High-Margin Service Mix: Wealth Management Solutions (WMS) now dominate revenue, contributing $9.9 million, driven by structured yield products and DeFi-enhanced offerings, which carry higher margins than legacy crypto trading.

2. Cost Optimization: Operating expenses were slashed, turning a $0.9 million loss into $0.8 million profit.

Sector Tailwinds: The Institutional Crypto Surge

The crypto sector is transitioning from a retail-driven market to an institutional one. AMBRAMBR-- is uniquely positioned to capitalize on this shift:

- Institutional Demand for Yield: AMBR's WMS division targets hedge funds and asset managers seeking structured yield products (e.g., collateralized loans and tokenized real-world assets like uMINT). These products offer steady returns amid volatile crypto prices.

- Regulatory Arbitrage: AMBR's partnerships with UBS Asset Management and BNBBNB-- Ecosystem signal credibility in navigating regulatory hurdles, a critical advantage as jurisdictions tighten oversight.

- DeFi and AI Integration: The launch of AgentFi and its AI ambassador MIA positions AMBR as a pioneer in AI-native financial tools, reducing operational costs and enhancing client engagement.

Operational Efficiency: A Lean, Agile Machine

AMBR's leadership has executed a masterful turnaround:

- Post-Merger Synergy: The iClick merger expanded its revenue streams without overextending capital. Marketing solutions contributed $1.6 million in Q1, diversifying reliance away from volatile trading volumes.

- Focus on High-Growth Segments: While legacy trading volumes dipped (e.g., Execution Trading fell 21%), this reflects a strategic pivot to higher-margin services. AMBR is choosing to prioritize profitability over volume.

- Capital Allocation: The $100 million Crypto Ecosystem Reserve funds innovation in tokenized assets and yield products, creating a moat against competitors.

Contrasting the Bearish Consensus: Why the Market is Wrong

Analysts are overly fixated on short-term risks:

- Technical Indicators: Overweighting the 14-day RSI of 29.57 (oversold territory) and declining moving averages ignores the fact that AMBR is a growth stock, not a momentum play. Oversold conditions often precede rebounds in high-growth sectors.

- Fair Value Misinterpretation: Morningstar's “$59.78 fair value” (likely a misprint given current data) aside, a DCF analysis estimates AMBR's intrinsic value at $11.71—just 36% above its current price. However, this assumes a conservative 2.9% terminal growth rate. If AMBR achieves its $65–75 million 2025 revenue target, upside could be far higher.

- Risk Mispricing: The market discounts regulatory risks excessively. While approvals for DWM Asset Restructuring are pending, AMBR's track record of strategic partnerships (e.g., DeFi DevelopmentDFDV-- Corp, BNB) suggests it can navigate hurdles.

The Case for an 80% Upside

Assuming conservative growth:

- Revenue Growth: If AMBR hits its $75 million 2025 target, and margins stabilize at 70%, EBITDA could jump to $25 million—a 1,800% increase from 2024.

- Valuation Multiple: Applying a 10x EV/EBITDA (modest for a high-growth fintech), the enterprise value would hit $250 million. At current shares outstanding, this implies a $24.00 price target, a 177% upside. Even at 5x EV/EBITDA, the upside is 80%.

Investment Strategy: Buy Now, Play the Long Game

- Entry Point: The current $8.60 price is a rare entry for growth investors, especially with the July 4 private placement (raising $25.5M) likely stabilizing liquidity.

- Risk Management: Use stop-losses (e.g., $7.00) to protect against volatility. Pair long positions with puts if risk tolerance is low.

- Hold for 12–18 Months: AMBR's full potential will unfold as institutional adoption accelerates and its RWA and AI initiatives scale.

Conclusion

Amber International is a margin-driven growth story in crypto's institutional revolution. The market's bearishness ignores structural improvements, sector tailwinds, and leadership execution. With a Strong Buy rating and 80% upside potential, AMBR offers asymmetric returns for investors willing to look past short-term noise.

Final Note: Always conduct due diligence and consider personal risk tolerance before investing.

Comentarios

Aún no hay comentarios