AGNC Investment's Underperformance and the Mortgage REIT Sector's Valuation Dislocation

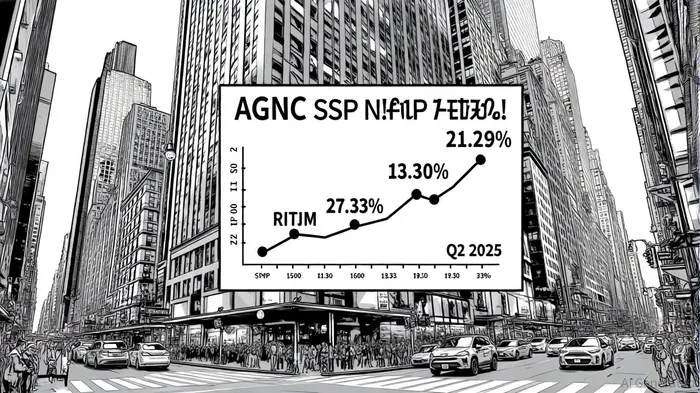

The recent underperformance of AGNC Investment Corp.AGNC-- (AGNC) relative to the broader market and its mortgage REIT peers raises critical questions about valuation dislocation in the sector. While the S&P 500 has delivered a year-to-date total return of 13.0% as of September 2025[1], AGNC's YTD return stands at 21.29%, masking a 12-month total return of 10.09%—well below the index's 19.44%[5]. This divergence is not merely a function of market dynamics but reflects deeper structural challenges in the mortgage finance sector, where interest rate sensitivity, leverage, and regulatory shifts are reshaping risk-rebalance opportunities.

Valuation Dislocation and Sector-Specific Risks

AGNC's struggles are emblematic of the mortgage REIT sector's broader vulnerabilities. The company's Q2 2025 performance of 4.14% pales in comparison to peers like Annaly Capital ManagementNLY-- (NLY) at 27.33% and Rithm CapitalRITM-- (RITM) at 18.63%[1]. This underperformance stems from AGNC's exposure to interest rate volatility, which has compressed net interest margins and eroded tangible net book value. By June 2025, AGNC's tangible net book value per share had fallen 5.3% to $7.81, reflecting a -1.0% economic return on tangible common equity[1].

The root of this dislocation lies in the sector's reliance on leveraged, duration-extended portfolios of agency mortgage-backed securities (MBS). AGNC's strategy—leveraging short-term financing to purchase longer-term MBS—exposes it to the dual risks of rising borrowing costs and prepayment uncertainty[1]. As the Federal Reserve contemplates 4–5 rate cuts in 2025[2], the sector faces a paradox: falling rates could improve MBS spreads but also increase prepayment risks, further destabilizing net interest margins. This dynamic is evident in AGNC's leverage ratio of 7.5x as of March 2025[4], which, while conservative compared to Starwood Property Trust's (STWD) aggressive 0.01 cash-to-debt ratio[6], still amplifies sensitivity to rate shocks.

Risk-Rebalance Opportunities and Strategic Adjustments

Despite these challenges, the mortgage REIT sector holds latent opportunities for risk-rebalance. AGNC's 14.8% dividend yield[4] remains a compelling draw for income-focused investors, particularly as the S&P 500's yield lags at 0.7%[1]. However, sustainability hinges on AGNC's ability to navigate valuation dislocations. The company's recent deployment of $509 million in equity through at-the-market programs into higher-yield MBS[3] suggests a strategic pivot toward capitalizing on wider spreads. Analysts project further gains if interest rates continue to decline, though this outcome remains contingent on macroeconomic stability[3].

Peer comparisons highlight divergent risk profiles. RITM, trading at a P/B ratio of 0.81[7], appears undervalued relative to AGNC's 1.21 P/B[5], reflecting differing investor perceptions of leverage and spread sustainability. NLY'sNLY-- GAAP leverage ratio of 7.1x[8] and economic leverage of 5.8x[8] position it as a more balanced player, while STWD's precarious liquidity underscores the sector's fragility. For AGNC, the path forward requires a delicate balancing act: maintaining leverage to amplify returns while mitigating duration risk through dynamic hedging and regulatory tailwinds, such as potential bank-sector demand for agency MBS[3].

Conclusion: A Case for Cautious Optimism

AGNC's underperformance is not a death knell but a symptom of sector-wide recalibration. The mortgage REIT's high dividend yield and strategic pivot toward higher-yield MBS offer a compelling case for risk-rebalance, particularly for investors with a medium-term horizon. However, the path to value creation remains fraught with interest rate uncertainty and liquidity constraints. As the sector navigates these headwinds, AGNC's ability to adapt its leverage and hedging strategies will determine whether it emerges as a resilient player or a cautionary tale in the evolving mortgage finance landscape.

Comentarios

Aún no hay comentarios