Advanced Drainage Systems: Navigating Earnings Challenges Amid Infrastructure Tailwinds and Margin Expansion Potential

Advanced Drainage Systems (ADS) reported its Q2 FY2026 earnings with a mixed performance: while revenue rose 1.8% to $829.88 million, net income declined to $1.84 per share from $2.06 in the prior year. Adjusted earnings, however, held steady at $1.95 per share, reflecting management's focus on operational resilience[4]. This outcome underscores the company's ability to navigate macroeconomic headwinds while positioning itself to capitalize on the transformative growth of the U.S. water infrastructure sector.

Infrastructure Tailwinds: A Structural Catalyst

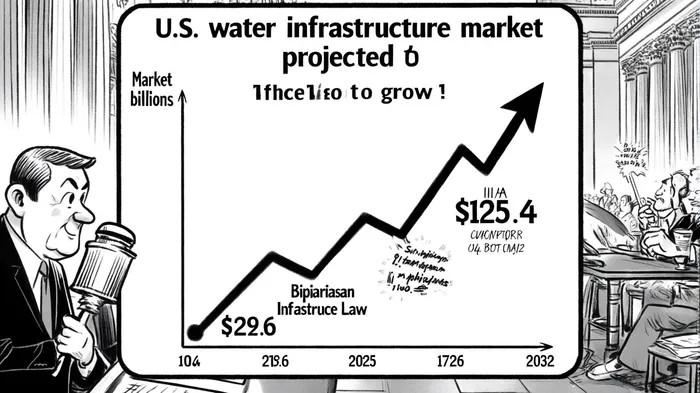

The U.S. water infrastructure and management market is on a clear upward trajectory. According to a report by PSMarketresearch, the sector is projected to grow from $125.4 billion in 2025 to $179.6 billion by 2032, driven by aging systems, climate change, and policy support[1]. The Bipartisan Infrastructure Law, which allocates over $50 billion for water projects, and the Infrastructure Investment and Jobs Act (IIJA), expected to fund $27.68 billion in 2025 for water and sewer systems, are pivotal in this expansion[2]. These policies are not merely fiscal stimuli but represent a generational shift in infrastructure priorities, with municipalities increasingly adopting public-private partnerships (PPPs) to bridge funding gaps[1]. For ADS, a leader in sustainable water management solutions, this creates a fertile environment for long-term growth.

Margin Expansion: Strategic Execution and Operational Discipline

ADS's Q2 results highlight its ability to maintain profitability despite external pressures. The company achieved an Adjusted EBITDA margin of 33.5% in Q1 FY2026, up from 30.6% in FY2025[3]. This margin expansion is a direct outcome of its strategic focus on high-value product mix and material conversion innovations. By prioritizing segments like Infiltrator and Allied Products-accounting for 44% of revenue and contributing to 30.6% of FY2025 Adjusted EBITDA-the company has demonstrated its capacity to leverage technological differentiation[3].

Moreover, ADS's emphasis on replacing conventional drainage solutions with sustainable, high-margin alternatives aligns with broader industry trends. As utilities grapple with the dual challenges of financing capital improvements and adhering to stricter environmental regulations, ADS's innovative offerings-such as geosynthetic-reinforced containment systems-position it to capture incremental market share[1].

Balancing Near-Term Pressures with Long-Term Potential

While Q2 earnings reflect a slight contraction in net income, the broader picture is one of strategic fortification. The company's FY2026 revenue guidance of $2.8 billion to $3.0 billion signals confidence in its ability to scale amid a $3.7 trillion infrastructure investment gap identified by the ASCE 2025 Report[4]. This gap, coupled with the adoption of flexible financing mechanisms like PPPs and value capture models, ensures a sustained pipeline of opportunities for ADS[2].

However, investors must remain cognizant of near-term risks, including input cost volatility and project execution challenges. ADS's recent performance, though resilient, underscores the need for continued operational discipline. The company's focus on gross margin expansion-achieved through product innovation and cost optimization-will be critical in translating infrastructure tailwinds into durable profitability.

Conclusion: A Compelling Long-Term Investment

ADS's Q2 results, while modest, reflect a company adept at navigating a complex macroeconomic landscape. The confluence of structural infrastructure demand, policy-driven capital flows, and its own operational excellence creates a compelling case for margin expansion. As the U.S. water sector enters a decade of unprecedented investment, ADS is well-positioned to deliver value to shareholders-provided it maintains its focus on innovation and disciplined execution.

Comentarios

Aún no hay comentarios