Zscaler Stock Plunges 34% in Three Months: Time to Exit or Hold Tight?

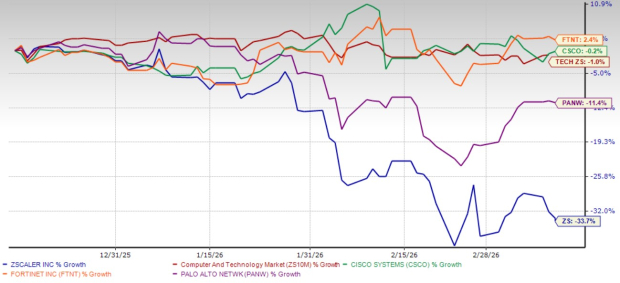

Zscaler, Inc. ZS shares have plunged 33.7% over the past three months, underperforming the Zacks Computer and Technology sector’s decline of 1%. Compared to key competitors like Cisco Systems, Inc. CSCO, Fortinet, Inc. FTNT and Palo Alto Networks, Inc. PANW, Zscaler’s slump appears even more pronounced. In the trailing three months, FortinetFTNT-- has risen 2.4%, while shares of Cisco SystemsCSCO-- and Palo Alto NetworksPANW-- have declined 0.2% and 11.4%, respectively.

Zscaler Three-Month Price Return Performance

Image Source: Zacks Investment Research

The sharp contrast raises a tough question: Is it time to move on from ZscalerZS--, or is there still long-term value in retaining the stock?

The plunge in Zscaler stock can be attributed to macroeconomic headwinds, including inflation, elevated interest rates and cautious enterprise IT spending. Increasing competition in the Zero Trust cybersecurity space and the company’s historically high valuation also contributed to its vulnerability during market corrections.

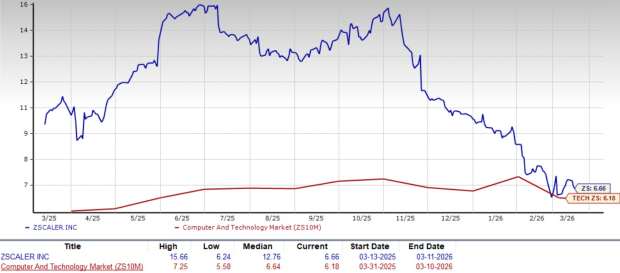

Zscaler holds a premium valuation, reflected in its Zacks Value Score of F. This is further reinforced by its Forward 12-month P/S ratio of 6.66, higher than the sector’s average of 6.18.

Zscaler Forward 12-Month Price-To-Sales Ratio

Image Source: Zacks Investment Research

Compared with its key competitors, Zscaler trades at a lower P/S multiple than Palo Alto Networks and Fortinet, while at a higher multiple than Cisco Systems. At present, Palo Alto Networks, Fortinet and Cisco Systems have forward 12-month P/S ratios of 10.76, 8.00 and 4.89, respectively.

We consider that the ongoing macroeconomic headwinds and lofty valuations are short-term pressures that do not diminish Zscaler’s long-term growth potential. We believe that while near-term issues are weighing on the stock, there’s still a strong fundamental case for staying invested.

Zscaler’s Investments Could Fuel Long-Term Growth

Zscaler remains at the forefront of the cybersecurity space through its innovative efforts. The company’s three main growth areas — AI Security, Zero Trust Everywhere and Data Security Everywhere — have together crossed the $1 billion annual recurring revenue (ARR) milestone, growing faster than the company’s overall business.

AI Security’s ARR is expected to exceed $500 million in fiscal 2026 as enterprises adopt AI Guard and agentic operations. Zero Trust Everywhere has already attracted more than 550 enterprises, achieving its goal of 390 enterprises quarters ahead of the initial target date. Data Security Everywhere is witnessing strong upsell opportunities as most customers use only a few modules today. These three pillars are likely to create strong, diversified drivers for Zscaler’s future growth.

Zscaler is taking an early lead in AI security, a fast-growing area of enterprise demand. The company processed nearly 1 trillion AI transactions in calendar 2025, showing how quickly enterprises are adopting AI. To address new risks like prompt injection and model poisoning, Zscaler launched AI Guard, which is now being tested by large customers.

Its Agentic Operations portfolio is also gaining traction and is expected to contribute significantly to AI Security ARR in fiscal 2026. With the integration of recently acquired Red Canary’s AI technology, Zscaler is building a differentiated AI-powered security operations center solution, positioning itself as a trusted vendor for securing AI applications.

Zscaler’s Z-Flex program is helping the company win bigger and more strategic multi-year deals. Introduced just four quarters ago (the third quarter of fiscal 2025), Z-Flex already delivered more than $290 million in total contract value bookings in the second quarter of fiscal 2026, a 65% sequential increase. The program gives customers the flexibility to adopt multiple modules over time under predictable pricing, making it easier to expand usage. This model encourages long-term commitments, strengthens customer relationships, and supports sustainable growth in fiscal 2026 and beyond.

Zscaler’s Strong Financial Performance

Despite macroeconomic pressures, Zscaler’s financial results remain impressive. In the second quarter of fiscal 2026, revenues soared 26% year over year to $816 million, with emerging products growing at a faster rate than core offerings. Non-GAAP earnings jumped approximately 29.5% to $1.01 per share.

Zscaler’s growing customer base underscores its strong market positioning. At the end of the second quarter, it had 728 customers generating $1 million or more in annual recurring revenues (ARR), with Fortune 500 and Global 2000 companies comprising a substantial portion. At the end of the second quarter, more than 45% of the Fortune 500 companies and approximately 40% of the Global 2000 companies are using Zscaler’s solutions.

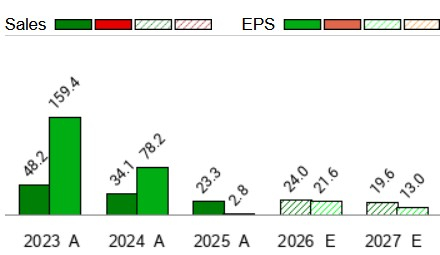

Zscaler is poised to benefit from enterprise migration to cloud environments, the increasing adoption of AI-driven cybersecurity and a recovery in IT spending. Its focus on large-scale enterprise deals and innovation pipeline is expected to drive accelerated growth in 2026 and beyond. The Zacks Consensus Estimate for fiscal 2026 and 2027 indicates strong double-digit revenue and earnings per share growth.

Sales And EPS Growth Estimates

Image Source: Zacks Investment Research

Final Thoughts: Hold ZSZS-- Stock for Now

Although Zscaler faces challenges related to macroeconomic uncertainties and premium valuation, the company’s heavy investment in AI, innovative cybersecurity capabilities and growing adoption of its solutions make the stock worth retaining at present.

Zscaler currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Fortinet, Inc. (FTNT): Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

Zscaler, Inc. (ZS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet