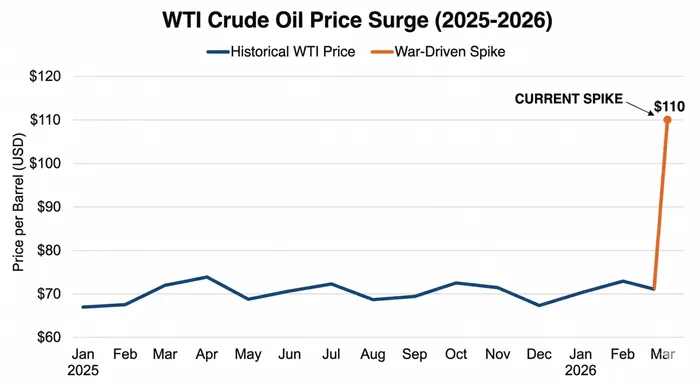

WTI Hits $110: The Gulf Oil Crisis Finally Arrives, but How Far Can the Price Go?

The war in Iran has undeniably raised the risk of a global economic shock, and the energy markets are acting as the immediate tripwire. Disruptions to supplies of oil and gas have triggered double-digit price increases, pushing WTIWTI-- past the $110 per barrel threshold. The immediate catalyst is the halt of tanker traffic in the Strait of Hormuz, a critical global choke point that typically handles roughly 20% of the world's oil and natural gas. While this sudden price spike is alarming and naturally evokes fear among market participants, my outlook remains grounded in optimism for the long term, presenting a distinct dual-horizon setup for traders. The short-term price action will remain volatile and aggressively bullish as geopolitical risk premiums get priced in—creating ideal conditions for momentum plays—but structural market forces will eventually force a retreat. We are not facing a catastrophic, permanent realignment of energy costs, meaning structural short positions could become highly lucrative once the immediate supply shock is digested.

The Immediate Pain: Retail Gasoline, Interest Rates, and Midterm Elections

The ripple effects of oil pushing past $110 are immediately visible at the consumer level. In the United States, a 10% increase in crude oil prices typically translates into higher pump prices, potentially adding 25 cents to a gallon of gasoline within a couple of weeks. This is an unwelcome development given that gasoline prices had been near four-year lows at the beginning of the year. The psychological weight of gasoline prices on American consumers is immense, burning into their perception of inflation far more than the falling costs of everyday items like bread or eggs.

Consequently, this presents a severe political vulnerability for President Trump. We are currently eight months out from the midterm elections, a period where the incumbent president's party generally struggles. Baseline expectations already point to Republicans potentially losing the House of Representatives, and rising costs at the pump will absolutely not aid Trump's narrative on economic affordability. Furthermore, polling indicates that public support for the conflict in Iran diminishes rapidly as it drags on and as gasoline prices climb.

Monetary policy is also caught in the crossfire. Inflation is currently running about a percentage point above the Federal Reserve's 2% target. While gasoline had previously been weighing down inflation, a reversal in energy costs—especially when non-housing services inflation remains sticky—gives policymakers reason to pause. Following the initial shock, there has been a noticeable repricing in the markets regarding the timing of the next Fed rate cut, making a June reduction less likely and reinforcing a wait-and-see mentality within the Federal Open Market Committee.

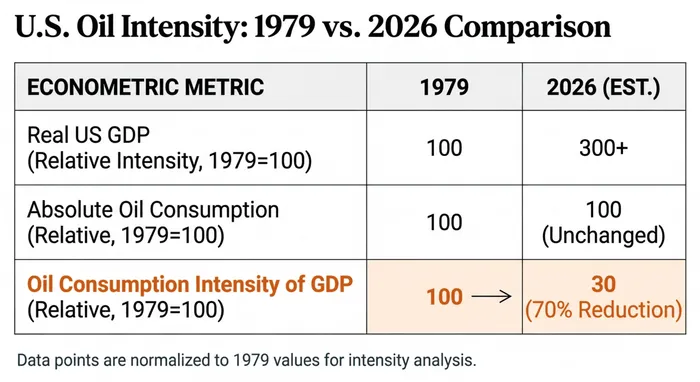

The Historical Buffer: Why 2026 is Not 1979

According to Ainvest analysis, a historical perspective is crucial to understanding why panic is unwarranted. It is easy to draw parallels to 1979, where the Iranian revolution triggered a massive oil shock that doubled prices and exacerbated double-digit inflation, leading to a destructive wage-price spiral. However, the architecture of the modern economy is entirely different. Since 1979, US real GDP has more than tripled, yet absolute oil consumption remains essentially unchanged. This means the intensity of oil as an input in the US economy has plummeted by roughly 70%, severely limiting the degree to which an energy shock can fracture the broader economic system.

Furthermore, the United States is operating from a position of relative strength. Thanks to the shale revolution, the US is highly self-sufficient in oil and even exports natural gas to Europe. The US economy also benefits from a massive strategic buffer. By the end of February 2026, the US Strategic Petroleum Reserve (SPR) held approximately 415.4 million barrels, reflecting a 5% year-over-year increase from recent lows. This reserve stands ready to be deployed to smooth out extreme price dislocations. Europe, while more vulnerable, is also better positioned than in the past; it does not have to decouple from a single massive provider the way it did with Russia, and it is currently exiting winter, reducing immediate heating demands.

Navigating the Inflation Threat Amid Mixed Economic Data

If this conflict stretches into months, the broader impact on inflation must be carefully monitored, particularly against a backdrop of recent macroeconomic data that has shown pockets of weakness, such as softer non-farm payroll figures. The European Central Bank estimates that a sustained 14% rise in oil prices adds half a percentage point to inflation and shaves 0.1% off GDP growth. This creates a brutal dilemma for the ECB, which may hesitate to hike interest rates to combat inflation while the European economy remains fragile.

In the United States, however, stagflation is not currently viewed as a material risk. The US economy entered this year with significant fiscal tailwinds, including tax refunds and favorable depreciation schedules for businesses. Even if a prolonged energy shock shaves a point off the IMF's previously estimated 2.4% US growth rate, the baseline trajectory remains stronger than much of the developed world. While the dollar has resumed its safe-haven status—potentially complicating the Trump administration's goal of narrowing the trade deficit via a weaker currency—the overall economic machinery is well-equipped to absorb this blow without spiraling into a 1970s-style recession.

The Path Forward: Price Projections and Market Fundamentals

According to Ainvest analysis, The current spike is heavily driven by headline fear, creating extreme divergence in institutional forecasts based on various disruption scenarios. For traders constructing options strategies or setting limit orders, mapping these institutional price targets is essential. At the extreme bullish end, Goldman Sachs warned on March 8 of an "Emergency" scenario, projecting WTI could hit $150 by the end of the month if the Hormuz disruption is not eased. Similarly, J.P. Morgan established a "Risk Ceiling" of $120—a scenario triggered if the conflict persists beyond three weeks—while Schroders modeled a $100 to $120 range for a 4-5 week restriction of the Strait.

However, base-case scenarios and structural targets highlight the massive downside risk once the geopolitical dust settles. UBS recently revised its base target to $90+ due to the near-closure of Hormuz. Yet, earlier baseline forecasts underscore the fundamental oversupply: Goldman Sachs' Q2 base stood at $76 just before the $100 breach, and Standard Chartered pegged Q1 at $74. Most tellingly, J.P. Morgan's "Structural" target—representing the fair value based strictly on supply and demand without the war—sits at a mere $60. For tactical positioning, this massive delta between the $150 emergency ceiling and the $60 structural floor suggests that while riding the upward momentum is the immediate play, preparing for a violent mean reversion will be the ultimate strategic trade.

Conclusion

The shockwaves from the Middle East have legitimately rattled the global markets, pushing WTI above $110 and threatening near-term inflation metrics. However, traders must differentiate between acute geopolitical pain and chronic economic illness. The US economy is fundamentally decoupled from the oil-dependent vulnerabilities of the 1970s, shielded by massive strategic reserves and record-breaking domestic production. While elevated volatility and rising pump prices are guaranteed in the short term—offering tactical long opportunities—the overwhelming consensus points to a structural oversupply that will eventually force prices violently down. Keep a close eye on the duration of the conflict to manage your trailing stops, but do not let historical panic dictate modern portfolio strategies.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet