Workday Tops Estimates but Cautious Guidance, AI Focus Weigh on Shares

WATCH: Bitcoin $200K? The math behind the next crypto supercycle.

WorkdayWDAY-- reported fiscal second-quarter results last night that topped Wall Street expectations on most fronts, but the stock is under pressure in the pre-market, down around 5% and testing technical support near the August low of $206. The company posted double-digit revenue growth, an earnings beat, and stronger operating margins, yet investor reaction reflects disappointment with cautious forward guidance and concerns over the durability of growth. With Workday considered a bellwether for enterprise adoption of agentic AI, the quarter offered a mixed picture: strong demand for new AI-driven products and early renewals helped boost backlog, but management’s restrained guidance for the second half suggests an ongoing tug-of-war between opportunity and macro headwinds.

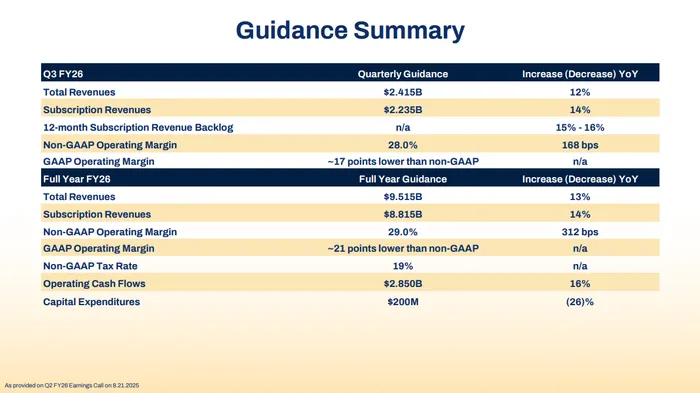

Headline numbers were solid. Workday reported adjusted earnings per share of $2.21, ahead of consensus estimates of $2.11. Revenue grew 12.6% year over year to $2.35 billion, in line with expectations, while subscription revenue increased 14% to $2.17 billion. Adjusted operating income of $680 million came in ahead of the $657 million consensus, equating to a 29% non-GAAP operating margin, a step up from the prior quarter. The 12-month subscription revenue backlog, or current remaining performance obligation (cRPO), rose 16.4% year over year to $7.91 billion, exceeding Workday’s 15–16% guidance range. That cRPO beat is notable because it demonstrates healthy demand and strong renewal activity, particularly around AI-related add-ons.

The performance of Workday’s agentic AI unit was a central focus. Management highlighted that more than 75% of new customer deals included at least one AI product, and net new ACV tied to AI more than doubled year over year. Products like talent optimization, recruiting agent, and contract intelligence saw strong uptake, while the Evisort acquisition continued to deliver outsized growth. The company also signed a definitive agreement to acquire Paradox, a conversational AI recruiting platform, which will bolster Workday’s capabilities in frontline hiring. Analysts were generally impressed with the breadth of AI adoption, noting 100% net new AI ACV growth and rising partner-sourced deals, which reached over 20% of new business for the second consecutive quarter.

Despite the solid quarter, investor skepticism was fueled by guidance. Workday raised its fiscal 2026 subscription revenue outlook to $8.82 billion, representing 14.2% growth, but the increase was almost entirely due to the pending Paradox acquisition. Without that contribution, the forecast would have remained flat, suggesting conservatism or uncertainty about organic momentum. For the third quarter, management guided to $2.235 billion in subscription revenue, essentially in line with consensus, and cRPO growth of 15.5%. Operating margin guidance of 29% is ahead of Street forecasts, but revenue conservatism overshadowed the profitability strength. Analysts stressed that management’s decision not to raise guidance to reflect the Q2 beat underscores unease about the second half.

Drivers of growth in the quarter included early renewals tied to AI adoption, continued momentum in financial management products, and a strong partner channel. International revenue grew 11%, with notable wins in EMEA and Asia, while U.S. revenue climbed 13%. The company also saw traction in government and higher education, though management acknowledged funding pressures at the state level and within universities, especially following recent federal budget adjustments. Headwinds remain in longer deal cycles, uneven macro conditions, and questions about how competitive the enterprise AI landscape will be as more players enter.

Analysts’ views reflected both optimism and caution. CantorCEPT-- Fitzgerald reiterated an Overweight rating with a $265 price target, highlighting attractive long-term risk-reward but acknowledging the lack of meaningful guidance raise. OppenheimerOPY-- cut its target to $270, citing uninspiring second-half expectations despite strong AI bookings. Canaccord reduced its target to $275 from $330 but maintained a Buy, arguing that Workday’s entrenched position, 97% retention, and trust factor will insulate it from AI disruption. BMO lowered its target slightly to $285 but praised the Paradox deal as a smart move to strengthen recruiting. MizuhoMFG-- was constructive, reiterating a $275 target and pointing to durable growth drivers such as financials, partner expansion, and AI adoption. KeyBanc cut its target to $285 but stressed that margin strength and cRPO beats remain encouraging.

The common thread in analyst commentary is that the quarter was solid, but guidance leaves open questions about Workday’s near-term trajectory. Bulls argue that the AI attach rate, strong renewal activity, and disciplined expense management point to sustainable growth, while skeptics point to the lack of an organic guidance raise as evidence of underlying caution. Investors may also be grappling with valuation: even after the recent pullback, Workday trades at a premium to many SaaS peers, which magnifies the impact of conservative guidance.

In the short term, technicals are coming into play, with shares testing the $206 level, the August low, as pre-market weakness follows cautious forward commentary. A break below that level could invite further downside, though bulls argue that risk-reward is increasingly attractive as Workday is building a track record of profitability and cash flow discipline alongside growth. Longer term, Workday’s AI strategy, deep enterprise relationships, and product expansion into financials and government make it a key player in the SaaS landscape. The next catalyst will be Workday Rising in September, where management is expected to lay out a more detailed roadmap for AI monetization and product integration.

In sum, Workday delivered a quarter that exceeded expectations on revenue, EPS, margins, and backlog, but failed to excite the market given conservative guidance. The AI narrative remains strong, with net new bookings more than doubling and new acquisitions expanding the company’s footprint. Yet the absence of a more meaningful guidance raise and macro headwinds in certain verticals keep investors cautious. Analysts remain largely supportive, with price targets cut modestly but ratings maintained, reflecting the view that while near-term uncertainty lingers, Workday’s long-term positioning as an enterprise AI leader remains intact. For now, sentiment will hinge on whether management can demonstrate second-half acceleration and deliver on the AI promise without sacrificing profitability.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet