WhiteFiber IPO: Mini CoreWeave Going Public, Will Nvidia Flavor Help Shares Skyrocket?

Investors are finally welcoming what they see as a genuine AI stock IPO following the success of CoreWeaveCRWV--. WhiteFiberWYFI--, an AI infrastructure solution provider and a subsidiary of crypto company Bit DigitalBTBT--, is set to go public on August 7 under the ticker WYFI. While Figma gained attention during its debut partly thanks to its AI narrative, WhiteFiber presents a fully AI-focused business. This could attract stronger demand and lead to a compelling valuation, especially given its partnership with NvidiaNVDA-- and ambitious growth plans.

The cloud infrastructure firm aims to raise $125 million by offering 7.8 million shares at a price range of $15 to $17, giving it a fully diluted valuation of approximately $558 million.

What is WhiteFiber

WhiteFiber is a wholly owned subsidiary of Bit Digital (BTBT), a digital asset mining and Ethereum treasury company with growing AI and HPC capabilities. Bit Digital transferred the entirety of its HPC operations into WhiteFiber, which will remain a controlled company, retaining 80% of the voting power even after the IPO.

WhiteFiber initially offered cloud services through a third-party data center in Iceland. Its AI infrastructure journey accelerated with the acquisition of Enovum in Montreal, Canada, in October 2024, providing control over a 4 MW (gross) AI data center. A 12 MW expansion is scheduled for completion and operation in the fourth quarter of this year. In the United States, the company plans to launch a 24 MW data center in North Carolina, expected to go online in the first quarter of 2026, with additional facilities under consideration. In total, WhiteFiber aims to achieve 76 MW of HPC capacity by the end of next year.

In comparison, CoreWeave had 420 MW of active capacity as of the end of March 2025. That figure is roughly 5.5 times WhiteFiber’s projected capacity by the end of 2026. The gapGAP-- underscores the scale difference, but management remains optimistic about accelerating WhiteFiber’s data center development.

Executives see substantial potential ahead, with 1,300 MW of projects currently under review. Of that, 800 MW are tied to non-binding and exclusive letters of intent, indicating that further expansion may come sooner than expected.

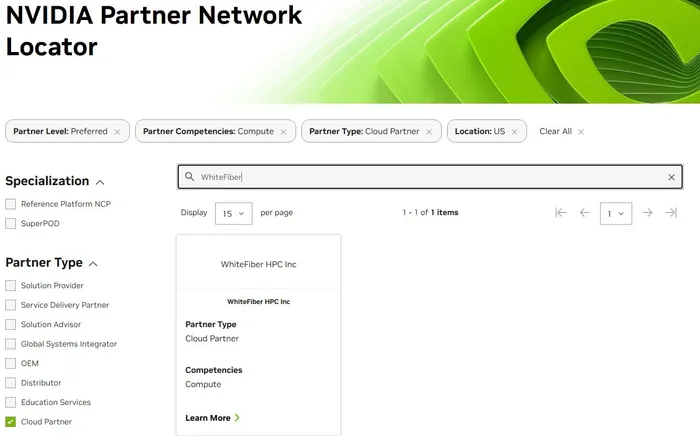

WhiteFiber is an authorized NVIDIA Preferred Partner through the NVIDIA Partner Network, which also includes CoreWeave and Applied DigitalAPLD--. All three companies were among the first recipients of the NVIDIA GB200 system in April, gaining early access to the latest high-performance GPU. As of June 30, 2025, WhiteFiber had deployed around 4,500 NVIDIA GPUs, with approximately 4,000 of them under contract.

The company has also established partnerships with Super Micro ComputerSMCI--, is a communications service provider authorized by Dell, and has an official agreement with Hewlett PackardHPE-- Enterprise. These alliances bolster the infrastructure buildout and strengthen WhiteFiber’s positioning within the AI cloud ecosystem.

Strong Financial Growth with a Short Track Record

WhiteFiber’s revenue is broken down into three main segments: cloud services that support GenAI workloads, colocation services where customers lease physical space, and equipment leasing to external clients.

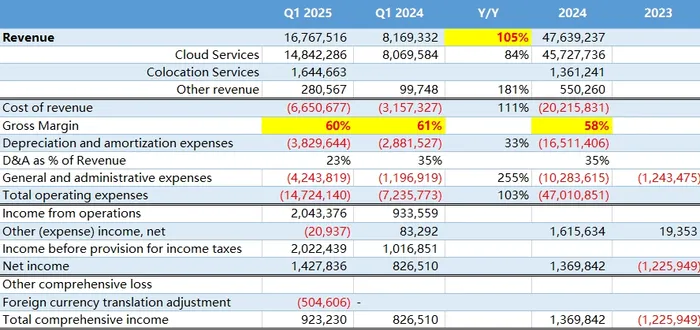

In the first quarter of 2025, WhiteFiber reported revenue of $16.8 million, representing 105% year-over-year growth. Cloud services surged by over 80%, while colocation revenue also showed strong momentum. The gross margin came in at 60%, which is lower than CoreWeave’s 70% plus margin, but still notable given WhiteFiber is in its early ramp-up stage. The company is already profitable, reporting net income of $1.4 million, equal to 8.5% of revenue, with no recorded spending on sales, marketing, or R&D.

It’s important to note that WhiteFiber only began its AI operations in October 2023, when Bit Digital signed its first binding agreement with a customer for GPU workloads. This means the company’s financial history is limited, and 2024 essentially marks its first full year of operating as an AI business. As a result, the long-term strategic vision remains underdeveloped.

Although headquartered in New York, the majority of WhiteFiber’s cloud operations are based in Iceland, which accounted for 89% of Q1 revenue, totaling $14.8 million. Following the Enovum acquisition, 10% of revenue came from Canada. With new infrastructure underway in both Canada and the U.S., future revenue distribution is likely to diversify. That said, a continued reliance on Iceland poses potential risks, especially considering currency fluctuations that may affect profitability.

Valuation Looks Attractive but Risks Remain

Investors may view WhiteFiber as an early-stage AI infrastructure company, one with bold plans but limited historical data. While the company presents a solid growth narrative and initial profitability, caution is warranted due to its immature stage and the inherent risks of rapid expansion.

WhiteFiber is valued at around $558 million, translating to a price-to-sales ratio of 8.3 based on annualized Q1 revenue. By comparison, CoreWeave is valued at roughly 13 times its annualized Q1 sales, while Applied Digital trades at around 24 times. At this range, WhiteFiber appears reasonably priced, and the IPO valuation could offer upside. If investors assign a P/S ratio of 15, WhiteFiber’s value could approach $1 billion, an 80% premium to its IPO range.

One factor that could fuel investor excitement is Nvidia’s ongoing support for its partners. Nvidia currently holds stakes in both CoreWeave and Applied Digital. If the chipmaker decides to invest in WhiteFiber in the future, that could significantly boost sentiment and price action. In that case, WhiteFiber might emerge as a risky but compelling opportunity, depending on how the stock performs in its debut session.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO