Western Digital's Hyperscaler Momentum Boosts Revenue Visibility

Western Digital Corporation’s WDC deepening collaborations with hyperscaler customers are improving its visibility into fiscal 2026 and beyond. For the fiscal second quarter, Western DigitalWDC-- (also denoted as WD) generated $3.02 billion in revenues, up 25% year over year, driven primarily by strong data center demand and increased adoption of high-capacity hard disk drives (HDDs).

Revenues from the Cloud segment accounted for 89% of the total revenues, reaching $2.7 billion and growing 28% year over year. This underscores the company’s increasing business with hyperscalers, which are scaling infrastructure to support AI training and inference workloads.

As AI and cloud adoption accelerate, demand for higher-density storage continues to rise. Western Digital is meeting this demand through close collaboration with hyperscale customers, delivering reliable, high-capacity drives with strong performance and a strong total cost of ownership. The company is advancing areal density gains, accelerating its HAMR and ePMR roadmaps and driving adoption of higher-capacity and UltraSMR drives.

Western Digital Corporation Price, Consensus and EPS Surprise

Western Digital Corporation price-consensus-eps-surprise-chart | Western Digital Corporation Quote

During the quarter, it shipped more than 3.5 million latest-generation ePMR drives, supporting up 32TB UltraSMR capacities, underscoring strong customer adoption. It shipped a total of 215 exabytes to customers, marking a 22% year-over-year increase.

The company also announced UltraSMR-enabled JBOD platforms in partnership with software ecosystem partners, broadening UltraSMR adoption. These platforms offer significantly higher storage density than conventional drives, delivering hyperscale-level performance while enabling more efficient and sustainable large-scale data analytics, highlighted WDCWDC--. Firm purchase orders with its top seven customers are secured through 2026, supported by multi-year commercial agreements with three of the top five customers extending into 2027 and 2028.

Looking ahead, the company’s guidance for fiscal third-quarter revenues of $3.2 billion, representing approximately 40% year-over-year growth at the midpoint, underscores sustained momentum. However, Western Digital needs to watch out for intense competition in this space from Seagate Technology Holdings Plc STX and flash-based alternatives such as Everpure PSTG.

Let’s Study How Hyperscaler Momentum Is Aiding Rivals

Seagate is one of the closest competitors to WD. STX is seeing steady growth in high-capacity nearline drive demand across global cloud customers and continued improvement at the enterprise edge — a momentum it expects to sustain given the robust build-to-order pipeline.

In the last reported quarter, the data center segment accounted for 79% of total revenues, at $2.2 billion, representing a 5% sequential increase and 28% year-over-year growth. Seagate shipped 190 exabytes of HDD storage, up 26% year over year and 5% sequentially. The data center market accounted for 87% of shipments, driven by sustained demand from global cloud customers and sequential growth in enterprise OEM markets. The company shipped 165 exabytes to data center customers, up 4% sequentially and 31% year over year.

Demand remains strong, especially from global cloud customers, and is expected to more than offset the typical March-quarter seasonality in the edge IoT markets. For the fiscal third quarter, it expects revenues of $2.9 billion (+/- $100 million). At the midpoint, this indicates a 34% year-over-year improvement.

Everpure’s expanding hyperscaler business is emerging as a meaningful driver of its growth strategy, as demand for high-performance, energy-efficient storage accelerates amid the proliferation of AI and large-scale cloud workloads.

PSTG expects fiscal 2027 revenues to be between $4.3 billion and $4.4 billion, indicating 18.8% year-over-year growth at the midpoint, with operating profit of $780-$820 million expected to rise about 26%. A key driver behind this outlook is the continued expansion of its hyperscaler business, especially in the second half of the fiscal year. PSTG also highlighted that the hyperscaler business performed better than expectations in fiscal 2026.

In fiscal 2026, the company focused on scaling its hyperscaler line of business and now anticipates significantly higher shipments and revenues in fiscal 2027 compared with the prior year.

WDC Price Performance, Valuation and Estimates

In the past month, shares have gained 13% compared with the Zacks Computer-Storage Devices industry’s rise of 12.1%.

Image Source: Zacks Investment Research

In terms of forward price/earnings, WDC’s shares are trading at 24.4X, up from the industry’s 17.63X.

Image Source: Zacks Investment Research

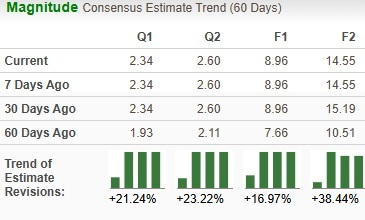

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised up 17% to $8.96 over the past 60 days.

Image Source: Zacks Investment Research

Currently, Western Digital sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

Everpure, Inc. (PSTG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet