Wendy's Q3 2025: Contradictions Emerge on Franchisee Cash Flow, Value Offerings, Breakfast Strategy, U.S. System Health, and International Expansion

Date of Call: None provided

Financials Results

- Revenue: $442.5M adjusted revenue, down $1.1M YOY

- EPS: $0.24 adjusted EPS, versus $0.25 prior year (down $0.01)

- Gross Margin: Global company-operated restaurant margin 12.4% (Q3)

- Operating Margin: U.S. company-operated restaurant margin 13.1%, down 250 bps YOY

Guidance:

- Full-year global system-wide sales expected down 3–5%.

- Adjusted EBITDA expected $505–$525M; adjusted EPS $0.82–$0.89.

- Free cash flow raised to $195–$210M (up $35M at midpoint).

- CapEx + build-to-suit expected $135–$145M; U.S. build-to-suit reduced ≈$20M.

- Net unit growth 2–3% (international >9%); ~100 U.S. openings but system optimization may push to low end.

- U.S. company-operated margin ~14% ±50bps; commodity inflation ≈5%, labor ≈4%.

Business Commentary:

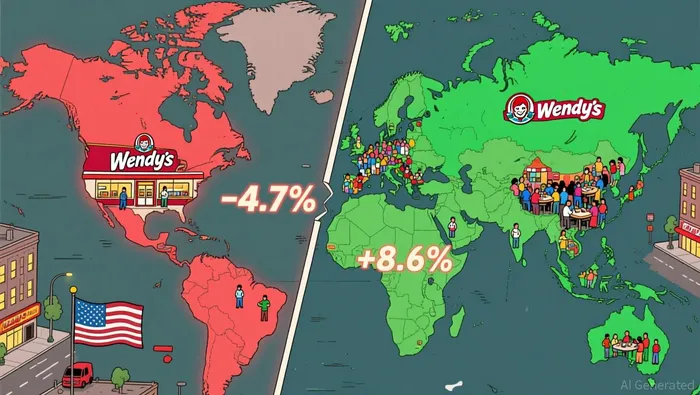

* International Growth and U.S. Challenges: - Wendy's global system-wide sales declined by2.6%, with U.S. same restaurant sales dropping by 4.7%, while international sales grew by 8.6%. - The decline in U.S. sales was due to heightened industry competition and consumer pressure, while international growth was supported by new restaurant openings and increased same restaurant sales.

- Project Fresh Initiatives:

- Wendy's launched Project Fresh, a comprehensive turnaround plan focusing on brand revitalization, operational excellence, system optimization, and capital allocation.

This strategic shift aims to attract new customers, elevate the customer experience, increase AUVs, and improve restaurant profitability.

Digital and Delivery Growth:

- Wendy's digital sales in the U.S. increased by

14.9%, reaching an all-time high digital mix of20.3%. Growth in digital and delivery was driven by enhancements in customer experience, such as improved training and geolocation data accuracy, which lowered cancellation rates and refunds.

Chicken Tenders Launch Success:

- Wendy's debuted its new chicken tenders, with strong demand leading to some restaurants selling out before national media support.

- The successful launch reflects improved operational execution and focused programming, contributing to enhancing the customer experience and brand perception.

Sentiment Analysis:

Overall Tone: Neutral

- Management highlighted strong international momentum (Q3 international system-wide sales +8.6%, net unit growth >9%), raised free cash flow guidance, and affirmed full-year targets, while acknowledging U.S. same-restaurant sales pressure (U.S. SRS -4.7%) and a company turnaround (Project Fresh) to revitalize brand, optimize the system and prioritize AUV growth to restore U.S. performance.

Q&A:

- Question from David Palmer (Evercore ISI): Franchisee cash flow and balance sheet levels today; quick wins within Project Fresh to help franchisee cash flow?

Response: U.S. franchisees are generally healthy with pockets of stress; Project Fresh will improve restaurant economics by evaluating underperforming units (operational fixes, transfers or closures) to unlock capital for reinvestment, and the chicken tenders launch is an early quick win.

- Question from Jeffrey Bernstein (Barclays): Primary factors for Wendy’s underperformance vs burger peers; are $5/$8 meals sufficient to protect value share?

Response: Pressure is concentrated on lower‑income consumers; the Biggie Bag and $8 JBC performed well—$8 drove frequency but not new guests—so strategy will combine price and quality messaging to better convey value.

- Question from Brian Mullan (Piper Sandler): Any guardrails for expected U.S. closures next year and the impact on franchise rental income?

Response: Estimate mid‑single‑digit percent of U.S. restaurants could close; closures will be decided programmatically with franchisees and may push net unit growth toward the low end of guidance; rental/income effects evaluated case‑by‑case.

- Question from Rahul Krotthapalli (J.P. Morgan): Clarify ‘grow U.S. AUVs over development’ — net vs. gross development and timing for bridging company/franchise performance?

Response: Gross U.S. development remains on track but net unit growth is expected at the low end of the 2–3% guide; focus is long‑term AUV growth via operational excellence and training, with scaling and benefits expected into 2026.

- Question from Dennis Geiger (UBS): Franchisee feedback on company‑owned outperformance and timing to scale actions across the franchise system?

Response: Franchisee feedback has been positive; the company is working with franchisees now to scale proven company‑store operational initiatives and expects to see benefits in 2026.

- Question from Chris O'Cull (Stephens): Details on the Creed & Company engagement and the analytics/capabilities being implemented?

Response: Conducting a large customer segmentation study to define brand essence and identify attributes that drive purchase decisions, informing menu, marketing and positioning to improve long‑term effectiveness.

- Question from Margaret‑May Binshtok (Wolfe Research): Color on recent beverage platform work and any sequential breakfast performance improvement?

Response: Launched cold brew/cold foam and a sparkling energy lineup that performed in line without media support; breakfast remains pressured industry‑wide but the beverage innovations enhance breakfast offering.

- Question from Danilo Gargiulo (Sanford C. Bernstein): How will breakfast be handled given focus on fewer things better—optional or mandated?

Response: Nationwide breakfast remains core, but franchisees with very low breakfast sales have been allowed case‑by‑case operating hour flexibility or opt‑outs to redeploy labor and improve profitability.

- Question from Jake Bartlett (Truist Securities): How to think about Q4 momentum and is Tendies national media the primary push for the quarter?

Response: Reaffirmed full‑year guide; simplified programming into Q4 with chicken tenders (Tendies) launched and national media starting next week—Q4 is expected to be the trough with momentum into 2026.

- Question from Eric Gonzalez (KeyBanc Capital Markets): Do you still charge franchisees closure fees and are those embedded in EBITDA outlook?

Response: Historically closures incurred fees but current intent is to approach closures collaboratively without automatic fees, asking franchisees to reinvest proceeds in remaining restaurants; actions will be handled case‑by‑case and evaluated with franchisees.

- Question from Brian Bittner (Oppenheimer): What specific uses for redirected capital to drive AUV growth and is it corporate or franchisee capital?

Response: Shifting capital from build‑to‑suit toward technology and marketing to drive AUVs—examples include digital menu boards, kitchen view improvements and analytics—corporate investments will support franchisee execution.

- Question from Gregory Frankfort (Guggenheim Securities): How many properties do you own the land for and would you consider monetizing land to fund revitalization?

Response: About 645 properties with land ownership; monetization of land under closed restaurants is on the table as a way to create capital for reinvestment, to be evaluated case‑by‑case.

Contradiction Point 1

Franchisee Cash Flow and System Optimization

It involves expectations regarding franchisee financial health and the scope and timing of system optimization initiatives, which can impact both immediate and long-term operating performance.

Could you clarify the franchisee cash flow and balance sheet status, and identify quick wins in Project Fresh to improve cash flow? - David Palmer (Evercore ISI)

2025Q3: The U.S. franchisee system remains healthy, but there are pockets under pressure. System optimization is crucial to enhance restaurant-level economics. - Ken Cook(CFO)

Can you discuss key consumer metrics and areas of greatest customer experience improvement? - David Palmer (Evercore ISI)

2025Q1: We are focused on operational excellence and customer experience by deploying tools like delivery scales and label printers to improve order accuracy. We measure customer satisfaction, and early results show improvements. - Kirk Tanner(CEO)

Contradiction Point 2

Value Offerings and Consumer Behavior

It reflects differing perspectives on the effectiveness of value offerings and the impact of consumer behavior on sales performance, which are critical for strategic decision-making and investor expectations.

What factors contributed to Wendy's underperformance relative to QSR burger peers, and how is the company addressing value offerings? - Jeffrey Bernstein (Barclays)

2025Q3: The back half of the year is as expected. Lower-income consumers face pressure. Wendy's offers compelling value with the Biggie Bag and $8 meal deals. The latter did not attract new customers effectively, indicating a need to enhance value communication. - Ken Cook(CFO)

Kirk, how is QSR positioned currently, and are you confident in the Biggy Bear-led platform or does it need refreshing or a shift in value marketing emphasis? - Jeffrey Bernstein (Barclays Bank)

2025Q1: We are planning prudently for the full year. Our strategy includes a balanced approach with innovation, value, and customer experience enhancements. We will execute our 100 days of summer program to drive traffic and offer value every week. Our approach is to balance value, innovation, and hospitality to win in the current environment. - Kirk Tanner(CEO)

Contradiction Point 3

Breakfast Performance and Strategy

This contradiction involves Wendy's approach to its breakfast offerings and their strategic importance, which affects overall sales and customer engagement.

Can you provide an update on the beverage platform's progress and market reception, particularly breakfast performance? - Margaret-May Binshtok (Wolfe Research)

2025Q3: Breakfast continues to underperform but offers room for growth. - Ken Cook(CFO)

What are the Q4 highlights, 2024 progress, and updated capital allocation policy? - Kirk Tanner (The Wendy's Company)

2024Q4: The morning daypart contributed to U.S. growth with sales up over 4%. - Kirk Tanner(CEO)

Contradiction Point 4

U.S. Franchisee Health and System Optimization

This contradiction is related to the health of Wendy's U.S. franchisee system and its optimization, which is crucial for future profitability and expansion.

Can you address franchisee cash flow and balance sheet metrics, and identify quick wins in Project Fresh to improve them? - David Palmer (Evercore ISI)

2025Q3: The U.S. franchisee system remains healthy, but there are pockets under pressure. System optimization is crucial to enhance restaurant-level economics. - Ken Cook(CFO)

What are your 2025 sales and profit outlook, CapEx plans, and cash flow expectations? - Ken Cook (The Wendy's Company)

2024Q4: Our U.S. franchisee system has performed well in the past few years with extensive growth in unit level profitability. - Ken Cook(CFO)

Contradiction Point 5

International Expansion and Franchisee Demand

It involves differing expectations for international growth and domestic demand, which impact strategic planning and resource allocation.

Can you provide estimates on the number of U.S. closures expected from the system optimization initiative? - David Palmer (Evercore ISI)

2025Q3: We are off to a good start with over 60% of our new units coming from international markets. We are confident in our global and U.S. pipeline. We remain focused on driving restaurant-level economics and engaging with franchisees to support growth. - Kirk Tanner(CEO)

Can you provide the unit development outlook, including franchisee demand and pipeline? - Dennis Geiger (UBS Investment Bank)

2025Q1: We are off to a good start with over 60% of our new units coming from international markets. We are confident in our global and U.S. pipeline. We remain focused on driving restaurant-level economics and engaging with franchisees to support growth. - Kirk Tanner(CEO)

Discover what executives don't want to reveal in conference calls

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet