Wells Fargo Q1: Guidance Holds Firm as Credit Costs Surprise to the Upside Despite Revenue Miss

Wells Fargo’s first-quarter results for 2025 missed expectations on both revenue and net interest income, yet the report still offered signs of resilience in a tough environment. Investors had feared a more pronounced deterioration in credit or a downward revision in guidance amid rate compression and macro uncertainty, but the bank instead delivered lower-than-expected credit costs and reaffirmed its full-year outlook. CEO Charlie ScharfSCHF-- emphasized progress on efficiency, credit normalization, and capital returns, offering a reassuring tone even as the top-line trends disappointed.

EPS, Revenue, and Net Interest Income

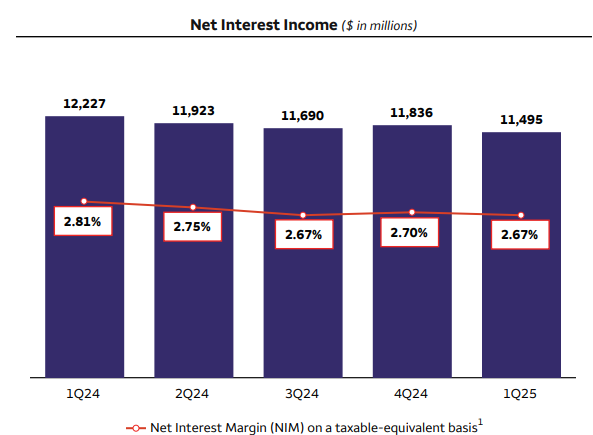

Wells Fargo posted EPS of $1.39, aided by $313 million in discrete tax benefits, though total revenue came in at $20.15 billion—short of the $20.73 billion consensus estimate. Net interest income declined 6% year-over-year to $11.5 billion, also missing the $11.81 billion forecast. The drop reflected pressure from lower floating-rate asset yields, shifts in deposit pricing and mix, and one fewer day in the quarter. Noninterest income held steady at $8.7 billion, with strength in asset-based fees and investment banking offset by weaker venture capital returns and trading.

Credit Costs and Asset Quality

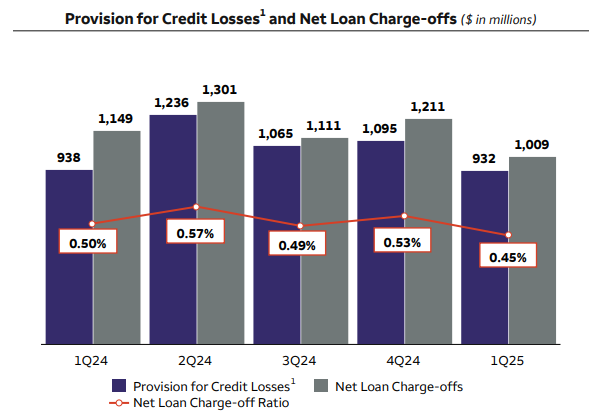

Credit performance was a relative bright spot. The provision for credit losses totaled $932 million, well below the $1.22 billion estimate. Net charge-offs were $1.01 billion, with commercial loan losses falling $192 million, primarily due to a sharp drop in commercial real estateACRE-- charge-offs—particularly in the office segment. The consumer charge-off rate edged up slightly to 0.86% on seasonal increases in credit card losses, though auto and other consumer portfolios improved. Nonperforming assets ticked up 4% sequentially to $8.2 billion, mostly due to increased commercial and industrial nonaccrual loans. Importantly, Wells FargoWFC-- reduced its allowance for credit losses to $14.6 billion, down 2% quarter-over-quarter, reflecting stability rather than stress.

Balance Sheet Trends and Capital Strength

Average loans declined 2% from the prior year to $908.2 billion, slightly below estimates, as weakness in commercial real estate and residential mortgages continued. Period-end loan balances were up modestly from Q4, aided by gains in commercial & industrial lending. Deposits also dipped slightly year-over-year to $1.34 trillion. The bank’s net interest margin was 2.67%, down from 2.72% a year ago. Capital levels remained strong, with a CET1 ratio of 11.1% and return on tangible common equity reaching 13.6%, above the 12.3% consensus.

Consumer Banking: Mixed Trends with Pockets of Strength

Consumer, Small and Business Banking revenue fell 2% as deposit costs rose, reflecting customer migration toward higher-yielding accounts. Credit card revenue increased 2% on higher balances, though card fees were pressured. Mortgage banking showed strength, with noninterest income of $332 million beating estimates, aided by better fee performance despite continued softness in loan balances. Auto lending revenue plunged 21% as the bank continued pulling back on lower-spread segments, while personal lending fell 10%. On the cost side, consumer banking expenses fell 2%, thanks to lower operating losses and efficiency efforts, partially offset by higher staffing and branch investments.

Corporate & Investment Banking: Steady with Highlights in CRE

Corporate and Investment Banking revenue rose 2% year-over-year. Banking revenue dipped 4% due to rate headwinds but was buoyed by improved debt capital markets activity. Commercial Real Estate revenue jumped 18%, benefiting from a gain on the sale of a non-agency servicing business and stronger capital markets flows. Markets revenue was largely unchanged, with strength in commodities and FX offset by weaker structured product and credit trading. Expenses in this segment rose 6%, driven by incentive compensation tied to stronger fee performance and operating cost inflation.

CEO Commentary and Guidance Reaffirmation

CEO Charlie Scharf struck an optimistic tone, highlighting a 16% YoY increase in EPS, strong capital returns, and fee growth across core businesses. He also emphasized the bank’s ability to manage costs while building momentum toward becoming a more respected institution. On trade policy, Scharf noted support for a resolution that would benefit the U.S. but warned of ongoing uncertainty. Crucially, Wells Fargo reaffirmed its 2025 outlook for net interest income to rise 1% to 3% from 2024 levels, and projected full-year noninterest expenses to remain around $54.2 billion—unchanged from prior guidance.

A Stabilizing Quarter Despite Headwinds

Despite headline revenue and NII misses, Wells Fargo’s Q1 report offered enough positives—particularly on credit and guidance—to be seen as better than feared. Investors worried about cracks in commercial real estate or a more cautious outlook may find relief in the steady tone of the results. While macro and policy risks remain, WFC’s focus on credit discipline, cost controls, and capital efficiency should offer a degree of protection as the operating environment stays volatile.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet