Is Wells Fargo Well-Positioned to Sustain Its Capital Return Strategy?

Wells Fargo & Company WFC maintains a disciplined capital distribution approach, aiming to return value to shareholders through dividends and share repurchases.

After clearing the Federal Reserve’s 2025 stress test, the company raised its common stock dividend by 12.5% in July 2025, to 45 cents per share. Over the past five years, the company has increased its dividend six times.

WFC has a five-year annualized dividend growth rate of 29.3% and a payout ratio of 29%. The company currently offers a dividend yield of 2.4%. Rather than pursuing aggressive hikes, the company has prioritized a steady and sustainable dividend policy, which strengthens its long-term financial position and supports investor confidence.

Wells Fargo & Company Dividend Yield (TTM)

Apart from dividends, Wells FargoWFC-- has been actively executing share repurchases. In April 2025, its board of directors authorized an additional $40-billion share repurchase program, following the $30-billion authorization announced in July 2023. As of Dec. 31, 2025, the company had remaining authority to repurchase up to $29.7 billion of common stock.

As of Dec. 31, 2025, Wells Fargo’s long-term debt was $174.7 billion. However, short-term borrowings were $251 billion. The company has a strong liquidity position, with a liquidity coverage ratio of 119% as of Dec. 31, 2025, which has exceeded its regulatory minimum of 100%. Its liquid assets (including cash and due from banks, as well as interest-earning deposits with banks) totaled $174.2 billion as of the same date.

The bank also maintains long-term issuer investment-grade credit ratings of A+, A1 and BBB+ from Fitch, Moody’s and S&P Global, respectively. Thus, given the solid credit profile and liquidity position, Wells Fargo will be able to meet its near-term debt obligations, even if the economic situation worsens.

WFC’s consistent dividends, active share repurchases and disciplined payout strategy reflect strong capital management and financial stability. Backed by solid liquidity and a steady earnings base, it is well-positioned to sustain capital distribution activities and reinforce investor confidence in its long-term prospects.

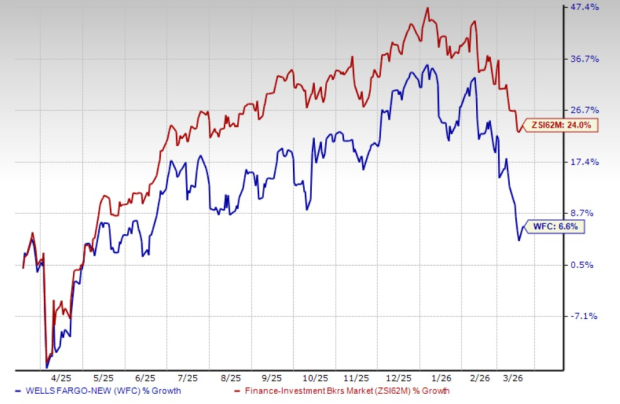

WFC’s Price Performance & Zacks Rank

Wells Fargo shares have rallied 6.6% in the past year compared with the industry’s growth of 24%.

Price Performance

Image Source: Zacks Investment Research

At present, WFCWFC-- carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

How Do WFC’s Peers Maintain Disciplined Capital Distribution?

Similar to WFC, its peers, The PNC Financial Services Group, Inc. PNC and Citigroup, Inc. C, are well-positioned to continue maintaining a disciplined capital distribution approach, supported by a solid liquidity position and consistent earnings strength.

In July 2025, PNC Financial announced a 6% increase in its quarterly dividend to $1.70 per share. Over the past five years, the company has raised its dividend five times, delivering an annualized growth rate of 7.8%.

PNC also has a share repurchase plan in place. As of Dec. 31, 2025, nearly 35 million shares remained available under the authorization. Management expects to repurchase $600-$700 million worth of shares in the first quarter of 2026.

Citigroup hiked its dividend 7.1% to 60 cents per share post clearing the Fed's 2025 stress test. Over the past five years, the company has increased its dividend three times with an annualized dividend growth rate of 3.4%.

Beyond dividends, C has a share repurchase program in place. As of Dec. 31, 2025, $6.8 billion worth of authorization remained available.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Wells Fargo & Company (WFC): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

The PNC Financial Services Group, Inc (PNC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet