Wells Fargo Beats Earnings… But the Stock Still Drops: What Investors Saw (and Didn’t Like)

Wells Fargo’s fourth-quarter earnings print was a classic “beat the profit line, miss the revenue line” setup — and in a tape where bank stocks have already enjoyed a strong 2025 run, that combination was enough to spark a mild sell-the-news reaction. Shares were down roughly 2% after the release as investors latched onto the top-line shortfall and slightly light net interest income versus consensus. The broader context matters here: expectations for the money-center banks were extremely high coming into earnings season, and JPMorgan’s choppy reception the day prior reinforced that the market wants clean beats, strong guidance, and zero loose threads. Wells didn’t exactly deliver a disaster, but it did deliver just enough “not perfect” to give traders a reason to lock in gains.

On the headline numbers , Wells FargoWFC-- reported Q4 EPS of $1.62, below the $1.66–$1.67 consensus range, while revenue came in at $21.29B versus expectations around $21.65B. The more relevant figure for how management framed the quarter was the adjusted result: earnings of $1.76 per share, which beat consensus by roughly $0.10, reflecting the exclusion of a notable severance expense item. Net income was $5.36B on a reported basis, but excluding the $612M pre-tax severance cost, net income would have been $5.8B. The bank posted a 12.3% ROE and 14.5% ROTCE, with an efficiency ratio of 64%, reflecting real progress on expense discipline even as it continues to invest in the franchise.

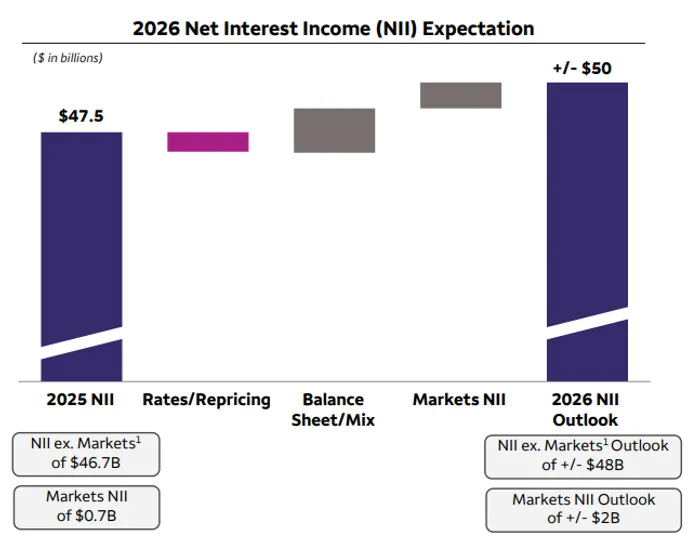

Net interest income was slightly soft versus the Street, which helped drive the negative reaction. Wells posted Q4 NII of $12.331B compared with estimates around $12.43B–$12.46B. Still, NII was up 4% year over year, driven by higher loan and investment securities balances, improved Markets results, and fixed-rate asset repricing — partially offset by deposit mix changes. NII excluding Markets was $12.0B (+3% YoY), while Markets NII was $358M (+$178M), showing that some of the year-over-year lift came from market-related tailwinds. Loan yields continue to roll over modestly, with total average loan yield at 5.78%, down 38 bps YoY and down 19 bps sequentially, reflecting the reality that the bank is operating in a lower-rate environment where repricing is not universally friendly. Deposit costs were a bright spot, with average deposit cost at 1.44%, down 29 bps YoY and down 10 bps from Q3 — a helpful offset in protecting spreads.

Loan growth and balance sheet momentum were strong enough to support management’s bullish tone, even if the market reaction didn’t fully cooperate. Average loans rose 5% year over year to $955.8B and increased 3% sequentially, led by commercial and industrial lending, auto, and credit cards, with securities-based lending in Wealth also contributing. On the flip side, commercial real estate and residential mortgage loans continued to decline, which is not surprising given industry-wide caution around CRE office and a still-choppy mortgage demand backdrop. Average deposits rose 2% YoY to about $1.4T and were up 3% sequentially, reflecting growth across Wealth and the corporate/institutional franchises. In management’s commentary, the theme was clear: Wells believes it is entering 2026 with improved momentum and fewer constraints, citing progress on operational remediation and a stronger platform to compete for growth.

By segment, the results showed broad-based improvement in consumer-facing categories, while some commercial lines were more mixed due to the rate environment and internal portfolio transfers. In Consumer Banking and Lending, revenue rose 7% YoY, with Consumer/Small Business Banking up 9% on lower deposit pricing and higher balances. Credit Card revenue rose 7% on higher loan balances and card fees, and Auto revenue increased 7% on loan growth. Home Lending was down 6% due to lower NII on reduced balances, and Personal Lending slipped 5% as lower balances and spread compression weighed. Importantly, the bank also noted a transfer of approximately $8B of loans and $6B of deposits tied to certain business customers from Commercial Banking to Consumer/Small Business Banking, which boosted the consumer segment and reduced reported growth in the commercial segment.

Commercial Banking revenue declined 3% year over year, with net interest income down 11% due to lower rates and the segment transfer, partially offset by lower deposit pricing and higher loan balances. Noninterest income, however, rose 18%, driven by higher revenue from tax credit investments and equity investments, which helped cushion the rate-driven NII pressure. Corporate and Investment Banking revenue was roughly flat, with Banking down 4% on lower investment banking revenue and lower rates, Commercial Real Estate down 3% on lower rates and the impact of a servicing business sale earlier in the year, and Markets up 7% driven by equities, commodities, and structured products (offset by weaker credit/rates/FX). Wealth and Investment Management was a standout, with revenue up 10% as NII climbed 16% on lower deposit pricing and higher balances, while noninterest income grew 9% on stronger asset-based fees tied to market levels.

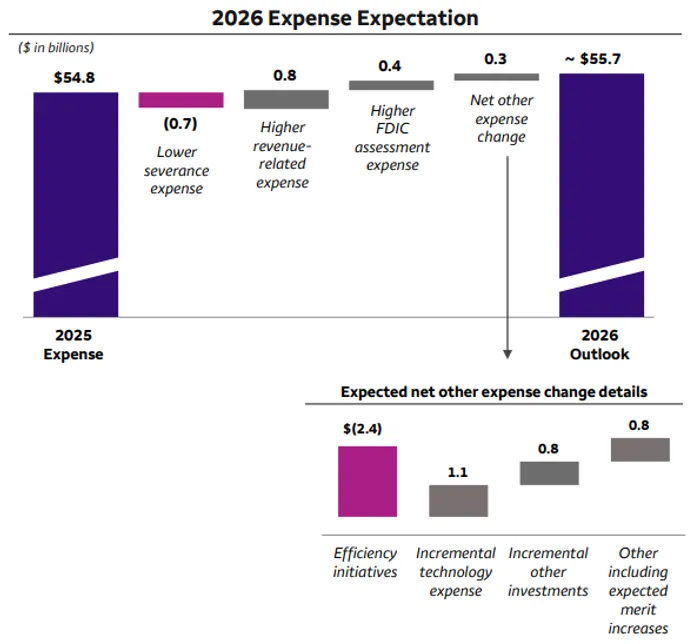

Expenses were one of the cleaner parts of the report, and management is attempting to frame 2026 as “disciplined, but still investing.” Q4 noninterest expense was $13.7B, down 1% YoY, with efficiency initiatives and lower operating losses helping offset higher advertising and technology costs. Personnel expense was basically flat as higher revenue-related compensation (notably in Wealth) was offset by efficiency savings and lower severance. For 2026, Wells guided to total expenses of roughly $55.7B versus a 2025 baseline of $54.8B — modestly higher year over year — with the bridge reflecting lower severance (a tailwind), but higher revenue-related costs, higher FDIC assessments, and continued investment spend. The key takeaway: Wells is still extracting savings, but it’s reinvesting a meaningful portion into technology and growth initiatives rather than running expense down aggressively.

Credit quality remains stable overall, with some pockets worth watching but no obvious blow-up signals. Provision for credit losses was $1.04B in Q4, and net charge-offs were $1.0B, down $165M, with net charge-offs at 0.43% of average loans annualized. Consumer net charge-offs rose modestly to 75 bps (annualized), driven by higher credit card and auto charge-offs and lower mortgage recoveries, while commercial net charge-offs increased to 22 bps driven by CRE and C&I. Nonperforming assets rose to $8.5B (0.86% of total loans), up slightly, driven by increases in CRE and C&I nonaccrual loans. The office CRE reserve metrics actually improved on the margin: CRE office allowance coverage declined, and the CRE office ACL fell, but that’s partly because charge-offs have already happened and balances have shifted — not necessarily because the office market has suddenly turned into a growth story.

So why is the stock down if the quarter wasn’t “bad”? The simplest answer is expectations. With bank stocks up sharply through 2025, investors have been positioned for a high-quality earnings season where revenue, NII, and guidance all need to deliver. Wells missed on headline revenue and came in slightly light on NII versus consensus, which is enough to trigger profit-taking when valuations have expanded and the market is looking for reasons to de-risk. The other factor is that management’s NII framework for 2026 is constructive but not explosive: the bank expects NII excluding Markets to rise year over year on balance sheet growth and mix shift, but rates and repricing remain a real headwind, and Markets NII is a swing factor. That’s not a red flag — it’s just not the kind of clean, upside surprise that forces shorts to cover and longs to chase.

Bottom line: Wells Fargo delivered a solid quarter operationally, highlighted by improving growth across key consumer and commercial lines, disciplined expense management, and stable credit performance. The revenue and NII misses were modest, but in a “priced for perfection” environment, modest misses still matter. The biggest areas to monitor going forward are (1) whether loan growth remains durable without sacrificing credit quality, (2) whether consumer charge-offs in cards and autos continue creeping higher, and (3) how effectively Wells converts its post-asset-cap freedom into real share gains without letting expenses drift too far above the guided path. For now, the selloff looks more like a valuation-reset and headline-driven reaction than a “something is broken” moment — but as this earnings season is already proving, the market is not handing out participation trophies.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet