Weekly BullsEye | This Stock Will Jump 50% This Year, And It's Still Not Too Late To Buy It

As the progression of electric vehicles slows down, and the future of traditional automobiles remains uncertain, many investors have started to waver in choosing whether to further their stakes in electric vehicles or revert to the traditional automobile industry. For this kind of investor, Vontier (VNT) may be an excellent choice.

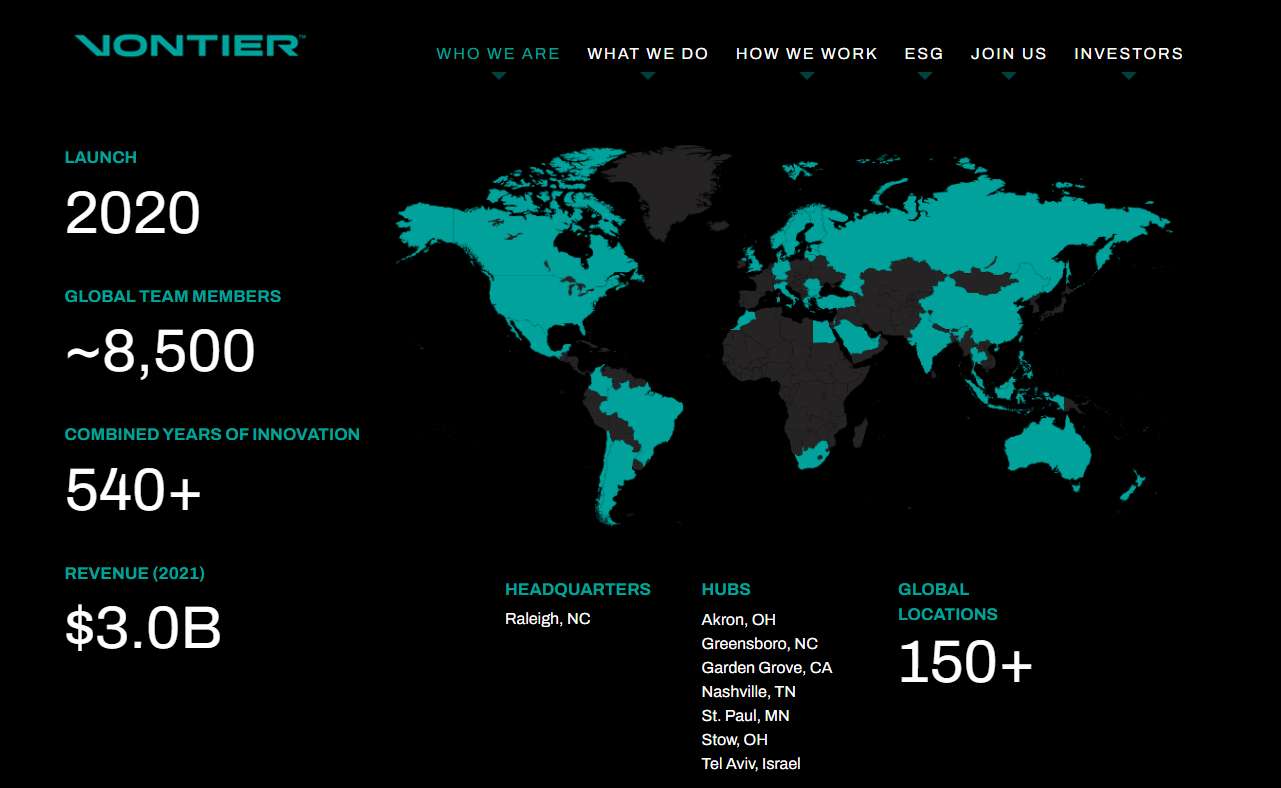

Vontier is a global industrial technology firm devoted to smarter transportation and mobility. Despite only being established in 2020, it now has branches in over 150 countries worldwide and a team of 8,500 employees.

Of course, when analyzing stocks, the size of the company is often just a minor factor; what we need to consider is the logic behind its potential growth.

if you drive a car, you could be a customer of Vontier's products

For Vontier, the strongest advantage could be its diverse range of products. This North Carolina-based company essentially provides software and hardware for every aspect of automotive-related services: it sells fuel pumps to gas stations and convenience stores, along with the corresponding card readers and sales software. It has created its charging devices and produces everything from electric vehicle charging interfaces to home charging stations.

It also sells all the tools needed for automobile repairs, offers a variety of car washing services, and even covers consultations and services related to auto asset management. In short, if you drive a car, you could potentially be a customer of Vontier's products.

This diverse range of products also ensures that Vontier will not worry about sales and revenue issues due to changing trends in the industry. It also provides a solid safety net for the company, increasing its resilience when dealing with emergencies or adverse external conditions.

Excellent Financials and Strong Resilience

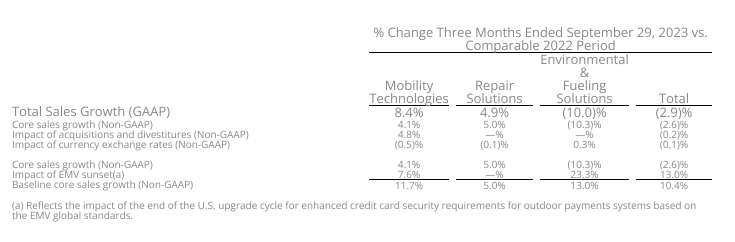

Vontier has demonstrated solid performance to date. In its most recent third-quarter report, the company's GAAP and core sales fell by 3% yearly to $765 million. However, showing resilience, Vontier's baseline core sales grew by 10%. This growth was consistent across all three of its business divisions. The company's operating profit margin stood at 18.5%.

Noteworthy is the fact that the company's most critical division, Environment & Fuelling Solutions (EFS), saw a 13% increase in baseline core sales. On the other hand, the Mobility Technologies segment, which is Vontier's second-largest, also witnessed an 8.4% rise in baseline core sales and a 12% increase in GAAP sales.

Apart from the statistics, Vontier's performance shows that it has been thriving in a favorable business environment, despite the current high interest rates. For example, the company's dispenser business saw significant growth. The fuel retail sector has been actively engaged in enhancing and refining its infrastructure, including everything from convenience stores and underground utilities to forecourts and car washes.

Excellent Business Model

Vontier was spun off from Fortive Corporation (FTV) in 2020, and Fortive itself was spun off from Danaher Corporation in 2016. Therefore, Vontier inherited the excellent business model from Danaher—Danaher Business System. This business model often uses lean manufacturing techniques to improve profit margins while promoting growth through small acquisitions.

Among industrial investors, DBS is seen as a gold standard, since shareholders have benefitted from it: Over the past five years, Danaher's stock price has risen 140%, surpassing the S&P 500 index's increase of 73%.

In fact, Vontier embodies the DBS business model intensely. Its portfolio includes companies such as DR and Invenco, and they are all acquired through this approach.

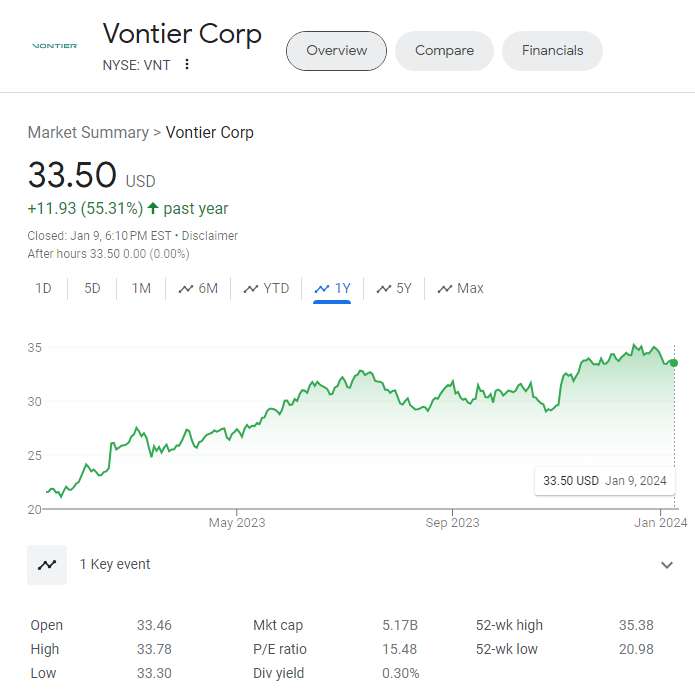

These series of acquisitions not only have not harmed the company's financial condition but have also enriched the mix of the company's products and further expanded its income sources. Also, under this model, Vontier's stock price has risen over 50% in the past year. Although the increase is not as rapid as Danaher's, it is indeed showing initial results.

Future Outlook

Over the next two years, Wall Street is predicting an annual growth rate of approximately 4% for Vontier's sales. The stock is pricing in revenue declines, but we see growth ahead, wrote UBS analyst Robert Jamieson. He rated the stock as buy and set a stock target of $38, a price that is 13% higher than the recent $33.50.

By 2024, Wall Street forecasts an operating profit margin of 22% for the company, which is also higher than the 16% average of industrial companies in the S&P 500 index. Over the next two years, Wall Street predicts an annual earnings growth of about 10%, and by 2025, earnings per share will reach $3.45.

Citi has also upped its price target on Vontier from $37 to $40 while maintaining its rating as buy. The analyst projects positive secular trends and fiscal policies for U.S. industrials moving into 2024, despite the potential challenges related to high interest rates and mixed macroeconomic indicators.

In fact, Vontier's valuation appears too low for such growth. Its P/E ratio for 2024 is only around 10.7x, less than the 18.2x of the S&P 500, the latter's earnings have grown at an average annual rate of about 12% in the past few years. Jamieson's $38 target will value Vontier's shares at 12x P/E ratio. If it can reach 15x, its value would rise to $52 per share, a 55% increase from the present level.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet