Weekly BullsEye | Concerning About Stock Market Sell-off? Here Is A Stock That Could Protect Your Returns

As the 3 major indices continue to hit all-time highs, many investors are starting to worry about how to protect their returns if the stock market starts to take a breather in the future. Don't worry, we have you covered for such an eventuality.

Taking profits is, of course, always a good idea, but also reinvesting your capital into some stocks with excellent long-term growth prospects is a viable option, and one such stock that fits the bill is retail giant Costco.

Membership Growth and Retention

Membership fees are one of the main sources of revenue for Costco, and the company demonstrated robust growth in its membership base in FQ1-2024, with paid household members up 7.6% and cardholders up 7.1% compared to FQ1-2023.

Renewal rates for Costco membership cards were a staggering 92.8% in the US and Canada and 90.5% in the rest of the world. This serves as an indicator of how sticky the company's customer base is, which is not only exemplary of the fantastic job Costco is doing but also the durability of its growth.

For every 1,000 members added to the Costco membership Ecosystem in a given month, there are 928 sticking with the company for the next month's service (in the US and Canada). Such customer stickiness can bolster an investor's confidence in the future growth prospects of the company.

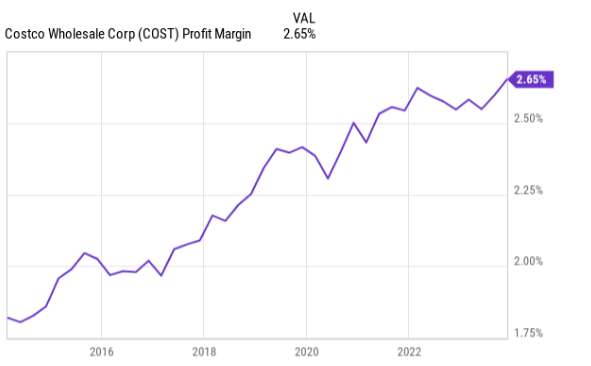

Profitability

Costco's e-commerce business showed improvement in FQ1 2024, with a 6.1% increase in sales compared to the previous year. The company has made a strong push into this space over the last year, and it seems to be paying off. It also shows that despite being a traditional brick and mortar retailer, the company is committed to adapting to consumer preferences by capturing online growth.

We consider these as the main drivers of revenue for the company and ultimately expect revenue to grow at a CAGR of 6.2% over the next five years.

This growth rate also implies $327B of revenue by FY2028, assuming retention stays roughly the same as it was in FQ1 2024. Meanwhile, thanks to Costo's emphasis on cost control measures through volume purchasing (i.e., buying in bulk from suppliers), the company has managed to maintain a steady profit margin.

The best illustration of this is that, over the past decade, through a global pandemic and inflation rates not seen since the 1970s, Costco's profitability has steadily increased. And this profitability combined with its member retention rate is exactly what justifies its high P/E multiples in the past.

As a result, Costco plans to open 33 new locations in Fiscal 2024. This is reflective of the company's confidence in its business model and growth prospects and also means more revenue growth for the company as it seeks out new locations and customers.

If you ask us, we would say this is unequivocally positive for shareholders.

The Upcoming Earnings Release

Given the healthy state of the economy and consumer spending remains high, Costco's sales YoY growth is expected to be between 6% and 7% in the next quarter. This implies that Costco's revenue should be slightly below or slightly above $59B, with an estimated EPS of $3.98 (projected net profit margin of 3%). The actual numbers could be even higher, as Costco has managed to beat market expectations in 16 out of the last 20 quarters.

However, no matter how you look at it, the future of Costco is extremely reliable, and the next earnings report will help the company continue to prove its reliability to the public.

Still, given the current stock price of Costco, we believe it would be best to wait for a while before making a move unless you have a particularly strong sentiment for this stock.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet