Warning! SanDisk’s 1,200% Surge Masks an Unchanged Memory Cycle

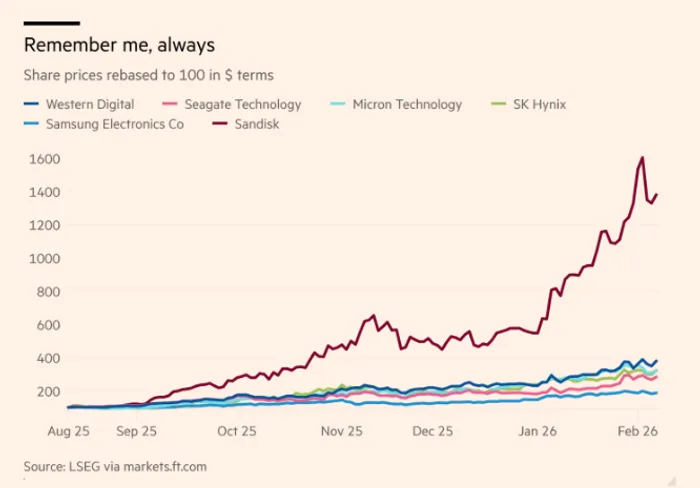

The memory chip industry has become the brightest star in equity markets. Over the past six months, SanDiskSNDK-- shares have surged by 1,200%, while other storage leaders—including Western DigitalWDC--, SeagateSTX--, MicronMU--, SK Hynix, and Samsung Electronics—have at least doubled, making them among the best performers in the S&P 500.

However, the Financial Times warns that the industry’s deeply cyclical nature has not disappeared, and investors may be repeating the same mistakes seen during the 2022 cycle reversal.

According to the FT , AI-driven demand for storage is the core force behind the current rally. As memory prices continue to rise, SanDisk has shifted from cash burn in 2024 to generating nearly $1 billion in free cash flow in the most recent quarter. Yet the storage industry is historically highly cyclical: demand can swing rapidly, while capacity adjustments lag, often resulting in sharp price volatility.

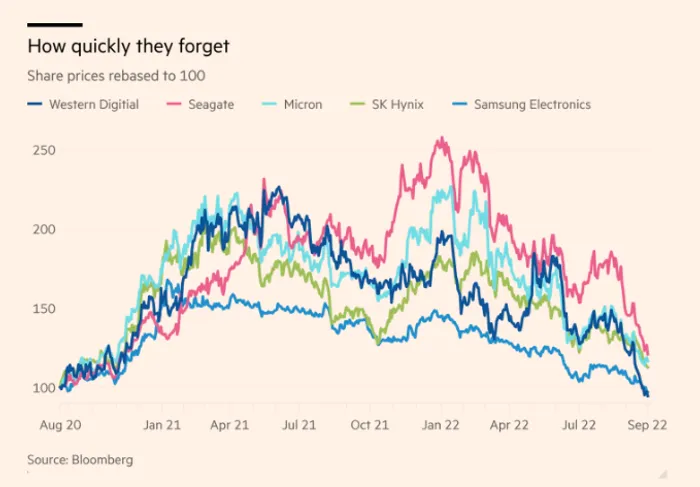

Industry veterans caution that “investors’ memories are too short.” Historical data show that from mid-2020 to early-2022, shares of Western Digital, Seagate, Micron, and SK Hynix all rose more than 100%, only to give back those gains entirely within nine months. Similar boom-bust cycles occurred in 2014 and 2018. Today’s optimism risks ignoring these recurring lessons.

Hyperscaler Ordering and Capacity Expansion May Trigger Another Oversupply Cycle

Industry analysts point out that the current memory market is displaying structural risks similar to those seen in 2022. In an effort to win contracts from cloud hyperscalers, suppliers often purchase memory capacity in advance—before securing firm orders—to demonstrate supply capability. Not all suppliers ultimately win these contracts, leading to aggregate orders that exceed real demand.

At the same time, hyperscalers themselves frequently overestimate future needs. When they later adjust orders downward, excess inventory quickly turns into severe market oversupply. Industry sources cited by the FT note that order volumes have already doubled or even tripled, with capacity expanding in parallel. Samsung’s recent announcement of a significant increase in DRAM capacity has further intensified potential supply-side pressure.

Is This Cycle Different?

While cyclical risks remain, some analysts believe the AI-driven expansion could last longer than previous cycles. Jonathan Goldberg of Digits to Dollars Advisory commented:

“Look at history over the past five years—markets eventually correct. This cycle has greater amplitude, so prices may keep rising. Many semiconductor investors who weren’t around five years ago say this time is different. The truth is, the cycle hasn’t changed.”

On the other hand, advances in high-bandwidth memory (HBM) are viewed as a potential structural differentiator. This specialized high-performance DRAM segment is currently dominated by Samsung, SK Hynix, and Micron. Ben Bajarin of Creative Strategies noted:

“This cycle is largely driven by HBM. HBM is more differentiated and won’t become commoditized in the near term… I believe memory revenue has already bottomed and is recovering.”

Markets now sit at the intersection of technological upgrades and cyclical forces, with HBM supply-demand dynamics likely to play a decisive role in shaping the duration and trajectory of this cycle.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet