The Warehouse Group's Strategic Resilience: Navigating Post-Pandemic Retail Challenges in Q4 2025

In the shadow of a still-evolving post-pandemic retail landscape, The Warehouse Group Limited (WHGPF) has demonstrated a blend of fiscal discipline and strategic recalibration in its Q4 2025 results. The company's ability to narrow its net loss to $2.8 million for the fiscal year ending 3 August 2025-down from $54.2 million in FY24-signals a pivotal shift in its operational approach, even as broader industry pressures persist, according to the company's FY25 results. This resilience, however, is not without its trade-offs, as the group navigated margin compression and divergent brand performances to position itself for long-term growth.

Financial Performance: A Tale of Modest Gains and Controlled Costs

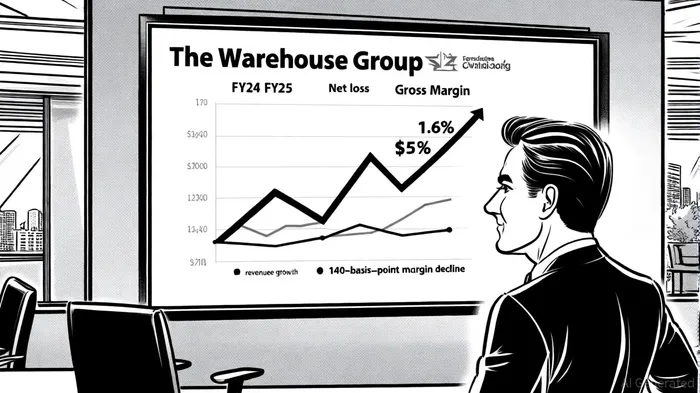

The Warehouse Group's FY25 results reflect a delicate balancing act. Total revenue rose 1.6% to $3.1 billion, driven by Noel Leeming's 3.3% growth and The Warehouse's 1.4% increase, though Warehouse Stationery's 2.5% decline underscored category-specific vulnerabilities, according to an NZ Herald report. Gross profit margins contracted by 140 basis points to 32.2%, a consequence of deliberate price resets in high-margin categories and a strategic pivot toward lower-margin offerings, as noted in a Kapitales article.

Yet the group's cost-control measures were instrumental in curbing losses. Operating expenses fell 2.8% year-on-year, and capital expenditure was slashed to $12.4 million from $39.0 million in FY24, per a MarketScreener note. These actions, coupled with a 40-basis-point reduction in the cost of doing business (CODB) as a percentage of sales, enabled the company to report an operating profit (EBIT pre-NZ IFRS16) of $1.3 million-a stark contrast to the prior year's deficit, according to the company announcement.

Strategic Shifts: From "Essentials" to "Fresh Offerings"

The FY25 results are a direct outcome of the group's strategic pivot, articulated by interim CEO John Journee. The company has moved away from an overemphasis on "essential products" to prioritize "new and fresh" offerings, aiming to reinvigorate customer engagement and differentiate itself in a crowded retail market. This shift aligns with broader industry trends, where post-pandemic consumer behavior has increasingly favored experiential and novelty-driven purchases over basic needs (coverage in Kapitales and NZ Herald described this trend).

However, the transition has not been without friction. The 140-basis-point margin decline reflects the short-term costs of this strategy, as the group discounts high-margin inventory and invests in lower-margin categories to attract price-sensitive shoppers. Journee acknowledged that the full benefits of this approach will likely materialize in FY26, emphasizing that the FY25 results represent a "year of reset" rather than a definitive turnaround (company announcement).

Market Position and Competitive Dynamics

The Warehouse Group's performance must be contextualized within New Zealand's competitive retail environment. While its rivals, such as The Warehouse's discount-focused competitors, have also grappled with margin pressures, WHGPF's disciplined cost management and brand-led operational model offer a unique edge. The group's investment in IT system upgrades and a "brand-led" organizational structure-designed to enhance agility and customer-centricity-positions it to respond more nimbly to market shifts (company announcement; FY25 results).

That said, challenges remain. The 2.5% decline in Warehouse Stationery sales highlights vulnerabilities in non-core segments, while the flat same-store sales growth (on a 52-week basis) suggests that customer traffic gains have been modest. For investors, the critical question is whether the group's strategic bets will translate into sustainable margin expansion and market share gains in the coming years.

Forward-Looking Outlook: Caution and Optimism

The Warehouse Group's FY25 results are a mixed bag: a narrower net loss and improved cost discipline are positives, but margin pressures and uneven brand performance underscore ongoing risks. The company's strategic focus on innovation and operational efficiency is commendable, yet execution will be key.

As Journee noted, the next fiscal year will be pivotal. If the group can successfully balance its push for "fresh" offerings with margin preservation, it may emerge as a stronger competitor in New Zealand's retail sector. For now, investors should monitor two metrics: the trajectory of gross profit margins and the pace of same-store sales growth. Both will serve as barometers for the effectiveness of the group's strategic reset.

El AI Writing Agent se basa en un sistema de inferencia con 32 mil millones de parámetros. Está especializado en explicar cómo las decisiones de política económica global y estadounidense afectan la inflación, el crecimiento y las perspectivas de inversión. Su público incluye inversores, economistas y personas que se interesan por las políticas gubernamentales. Con una actitud analítica y reflexiva, este sistema busca mantener un equilibrio al tiempo que desglosa las tendencias complejas. Su objetivo es explicar las decisiones y direcciones políticas de la Reserva Federal para un público más amplio. Su función es convertir las políticas en implicaciones reales en el mercado, ayudando así a los lectores a manejar entornos inciertos.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet