Walmart Q2 Earnings: A Mixed Bag for the World’s Largest Retailer

WATCH: Bitcoin $200K? The math behind the next crypto supercycle.

Walmart’s second-quarter results painted a nuanced picture of the American consumer, global trade pressures, and the company’s evolving digital ambitions. As the world’s largest retailer, WalmartWMT-- is always a key barometer of household spending, but this quarter investors were equally attuned to its commentary on tariffs, which have begun to weigh more visibly on costs and margins. While top-line momentum remained solid, profit performance was clouded by legal expenses and insurance claims, creating a noisy bottom line. The company raised its full-year guidance, but the stock traded down around 3% in premarket, hovering near the psychologically important $100 level—a reminder that markets demand cleaner beats, not just steady execution.

Results Versus Expectations

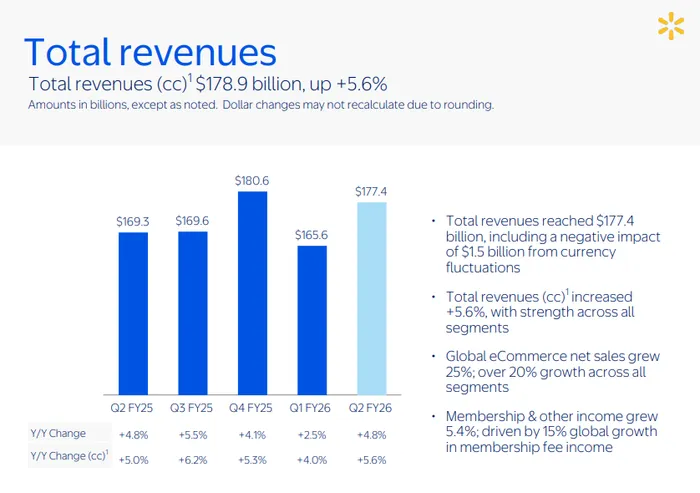

Walmart reported adjusted earnings per share (EPS) of $0.68, missing Wall Street consensus of $0.73–$0.74. Revenues grew 4.8% year-over-year to $177.4 billion, modestly ahead of analyst estimates at $176.2 billion. While the top-line performance highlighted Walmart’s continued share gains, particularly in grocery and e-commerce, the EPS miss broke a streak of quarterly beats dating back to May 2022. Importantly, the EPS shortfall was not solely operational—one-time legal expenses, restructuring charges, and higher-than-expected self-insured liability costs weighed on profitability. Walmart estimated these pressures reduced adjusted EPS growth by roughly 560 basis points.

Despite the miss, management lifted its guidance. For fiscal 2026, Walmart now expects net sales growth of 3.75–4.75% (versus prior 3–4%) and adjusted EPS of $2.52–$2.62, slightly above its previous range. Third-quarter guidance also came in ahead of expectations, with EPS guided to $0.58–$0.60 versus consensus at $0.57.

Key Metrics: Same-Store Sales, eCommerce, and Advertising

The U.S. business continued to anchor growth. Walmart U.S. comparable sales rose 4.6% ex-fuel, comfortably above analyst estimates of ~4%. Transactions grew 1.5% and average ticket increased 3.1%, suggesting customers are both visiting more often and spending more per trip. Grocery and health & wellness categories remained strong, while general merchandise—a category that lagged during peak inflation—showed signs of recovery.

eCommerce remained a standout: global eCommerce sales surged 25%, with Walmart U.S. posting 26% growth. Store-fulfilled delivery expanded nearly 50%, and about a third of online orders were expedited, a sign of the company’s logistical muscle. Importantly, profitability in the eCommerce segment improved. CFO John Rainey noted that Walmart doubled eCommerce profitability sequentially, marking a turning point as scale and efficiency gains feed through.

Advertising, Walmart’s stealth “agentic AI” play, continues to scale rapidly. Global advertising sales grew 46%, including the integration of VIZIO, while Walmart Connect in the U.S. expanded 31%. As Walmart connects its digital and physical ecosystems, advertising offers high-margin diversification. With VIZIO televisions funneling consumer engagement into its platform, Walmart is quietly building a data-rich advertising flywheel—one that investors increasingly view as its AI-powered growth lever.

Membership income also added resilience, climbing 15.3% globally. Walmart+ and Sam’s Club memberships continue to grow in both volume and renewal rates, reinforcing recurring revenue.

Tariffs, Margins, and the Inflation Backdrop

A major investor focus was tariffs and their impact on costs. Roughly a third of Walmart’s U.S. merchandise is imported, leaving it exposed to policy shifts in China, Mexico, Vietnam, and elsewhere. CFO Rainey acknowledged that tariff-impacted costs are “continuing to drift upwards”, though Walmart is managing the pain with a mix of early inventory pulls, selective pricing adjustments, and Rollback promotions. Notably, private label sales—often a bellwether for consumer trade-down—remained flat year-over-year, suggesting shoppers are holding steady despite cost pass-throughs.

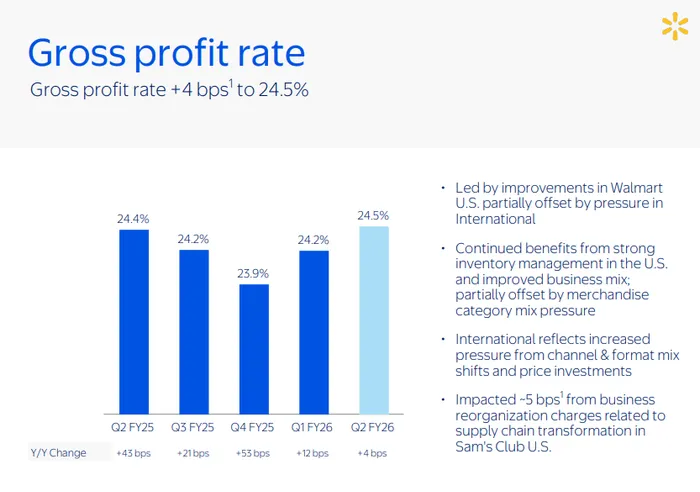

Gross margin improved by 4 basis points, led by Walmart U.S., but underlying profitability was pressured. Operating income fell 8.2% reported, though it grew modestly on a constant currency adjusted basis. The hit from legal settlements, restructuring, and insurance claims underscores how fragile margins can be in a high-volume retail model.

Stock Reaction and Market Sentiment

Despite raising guidance, Walmart’s shares slipped around 3%, as investors focused on the EPS miss and “noisy” profit line. At ~$100, the stock is testing a psychological support level. The market’s response suggests that while revenue strength and strategic progress are applauded, short-term earnings clarity still drives valuation. Competitor dynamics also color sentiment—Target remains under pressure, highlighting Walmart’s relative strength, but investors may worry about margin sustainability in an environment of sticky tariffs, rising wages, and volatile consumer demand.

Strategic Takeaways

CEO Doug McMillon emphasized Walmart’s “people-led, tech-powered” strategy, underscoring AI-driven digital experiences and continued share gains. The company’s push into advertising, coupled with improved eCommerce economics, positions Walmart as more than just a low-margin retailer. The ability to monetize traffic through data, logistics, and digital media will be critical in sustaining profitability as tariffs and operating costs rise.

For the consumer, the quarter offered a reassuring read: shoppers remain resilient, spending consistently across categories despite inflationary and tariff headwinds. Walmart’s scale and efficiency continue to allow it to absorb cost shocks better than peers.

Bottom Line

Walmart’s Q2 was a mixed bag—solid revenue growth, resilient consumer trends, and powerful digital momentum were offset by noisy one-time costs and tariff headwinds. The company missed on EPS for the first time in over two years, but raised its full-year outlook, reflecting confidence in its trajectory. For investors, the key questions now are whether tariff pressures deepen, and whether advertising and eCommerce profitability can offset these margin headwinds.

The stock’s slide shows little tolerance for anything less than clean execution. Yet strategically, Walmart is signaling that its long-term value creation increasingly lies not just in groceries or low prices, but in digital platforms, advertising, and AI-powered consumer engagement. That evolution, more than the $0.05 EPS miss, will define Walmart’s investment case in the years ahead.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet