Walmart Beats the Quarter—But Its Outlook Just Spooked Wall Street

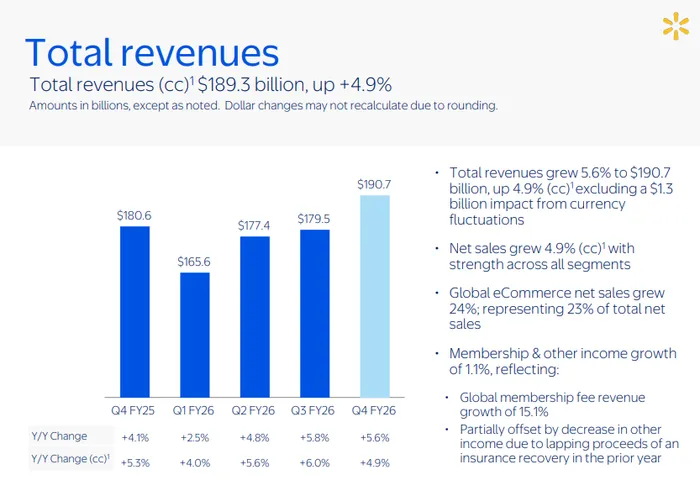

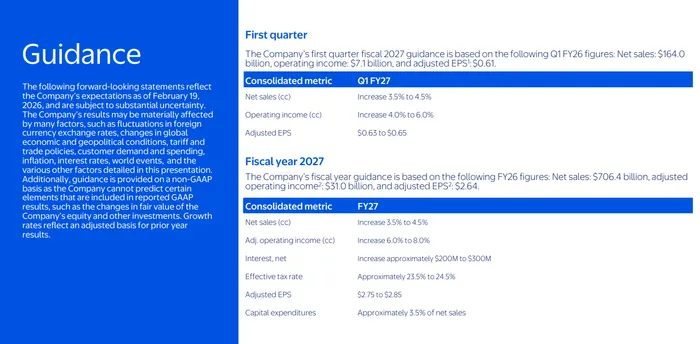

Walmart’s fiscal Q4 (holiday quarter) was a familiar “beat the quarter, miss the vibe” setup: results came in a touch better than expected, but the outlook did the real damage, sending shares down about 3% pre-market. On the headline numbers, WalmartWMT-- posted adjusted EPS of $0.74 versus $0.73 expected, and revenue of $190.66B versus roughly $190.4B expected, with consolidated revenue up 5.6% year over year. The problem is guidance. For next quarter, Walmart guided adjusted EPS to $0.63–$0.65 versus $0.68 expected, and for the year it guided adjusted EPS to $2.75–$2.85 versus $2.96–$2.97 expected, alongside constant-currency sales growth of 3.5%–4.5%. In other words: the engine is still running smoothly, but management is telling you not to expect a new top speed record.

Starting with the key operating metrics investors care about, U.S. comparable sales were strong at +4.6%, slightly above the +4.2% expectation and consistent with Walmart’s steady “share-gain in groceries plus improving discretionary” playbook. The quarter also showed healthy underlying demand: transactions rose 2.6% and average ticket increased 2.0%. Management highlighted that momentum continued into the period, with transaction growth led by digital and described the quarter as featuring broad-based share gains. On profitability, consolidated operating income grew faster than sales, up 10.8% (10.5% adjusted), reflecting a combination of higher gross margin, inventory discipline, some expense leverage, and better e-commerce economics driven by mix and efficiency.

Walmart U.S. was the anchor of the quarter and the clearest proof point that the omni strategy is still compounding. U.S. compCOMP-- sales were up 4.6% and U.S. e-commerce sales jumped 27%, led by store-fulfilled pickup and delivery plus continued growth in marketplace and advertising. Expedited store-fulfilled delivery channels grew more than 50%, which matters because it speaks to Walmart using stores as fulfillment nodes (convenience) without letting fulfillment costs run wild (profitability). Gross profit rate in Walmart U.S. increased 17 bps and operating income rose 6.6%, driven by stronger gross margin, disciplined inventory management, modest operating expense leverage, and improving e-commerce economics. Inventory in Walmart U.S. rose 2.9% with “healthy in-stock levels,” which is a subtle positive: it suggests they’re not starving the shelves to protect margin, but also not drowning in markdown risk.

One granular item worth flagging: Walmart noted that U.S. Health & Wellness comp sales reflected about a 200 bps headwind tied to “maximum fair pricing” implemented January 1. That implies a deliberate pricing action that pressured that subcategory’s comp contribution, likely in exchange for price perception, loyalty, or regulatory/plan dynamics. The takeaway is that core U.S. comp strength was solid even with that drag embedded, which makes the headline +4.6% look slightly more resilient than it appears at first glance.

Sam’s Club U.S. was good, though not quite as clean versus expectations. Comparable sales rose 4.0% versus about 4.4% expected, but the composition was constructive: sales strength was led by grocery and general merchandise, and comp performance was driven by increased transactions and unit volumes. E-commerce sales at Sam’s increased 23%, with continued strong growth in club-fulfilled pickup and delivery. Membership fee revenue grew 6.1%, supported by steady member counts, renewal rates, and Plus member growth. For the model, membership fees are the high-quality earnings stream, so continued growth there helps offset the fact that Sam’s comp was a touch light.

International was a standout on growth, with sales up 11.5% year over year to $35.9B, driven by China, Walmex, and Flipkart, and with strong momentum across both stores and e-commerce. International e-commerce grew 17% in Q4, and management pointed out that Flipkart’s “Big Billion Days” timing was a headwind to Q4 growth (benefiting Q3 instead), which is the kind of calendar noise that matters when you’re trying to handicap trendlines. On profitability, management cited operating income growth helped by lower e-commerce losses and lapping last year’s strategic investments. Translation: they’re still spending, but the incremental dollars are working harder, and the loss profile in the digital business is improving.

The “higher-margin engines” were a major highlight and one reason the quarter itself looked better than the stock reaction suggests. Walmart’s global advertising business grew about 37% in the quarter (with Walmart Connect in the U.S. up 41% ex-VIZIO), and full-year global advertising revenue grew 46% to nearly $6.4B. That’s material because retail media carries attractive margins and creates a flywheel with marketplace growth: more third-party sellers and more digital traffic increases ad inventory and ROI, which pulls in more ad dollars. Management also emphasized that membership fee revenue grew 15.1% globally in Q4, another signal that the ecosystem (memberships + marketplace + ads + delivery) is scaling.

So why the guidance disappointment if the quarter looked strong? It mostly comes down to margin and expense expectations in a choppy macro and cost environment. Walmart guided constant-currency net sales growth of 3.5%–4.5% for both Q1 and the full year, and guided adjusted operating income growth of 6%–8% (constant currency), which doesn’t scream “margin collapse.” But the EPS guide is below consensus, implying either incremental margin pressure, higher below-the-line expenses, or a more cautious stance on mix and investment. Notably, Walmart expects net interest expense to increase by roughly $200M–$300M, which is a direct EPS headwind in a higher-rate world. They also signaled capital expenditures around 3.5% of net sales, consistent with continued investment in automation, supply chain, and digital capabilities—great for the long term, less great if the market wants near-term EPS acceleration.

On tariffs and cost pressures, Walmart’s messaging is usually pragmatic: they don’t tend to posture; they tend to adjust. The company acknowledged the broader backdrop of inflation and tariff uncertainty as part of the cautious tone embedded in guidance. The practical implication is that tariffs can flow through as higher input costs in certain categories, forcing a choice among price, margin, and mix. Walmart’s scale, sourcing, and private brand capabilities typically allow it to manage tariffs better than most retailers, but “better than most” doesn’t mean “immune,” especially if tariff schedules change quickly or hit categories where the consumer is most price-sensitive. If oil stays bid and freight costs follow, that becomes an additional variable for both pricing and gross margin management.

AI commentary was more about direction than a single headline feature: management framed the retail environment as moving toward faster, more convenient, and more personalized experiences, which is exactly where AI gets deployed (search, recommendations, inventory forecasting, routing, labor scheduling, shrink analytics, and ad targeting). Reuters also characterized Walmart’s recent operating playbook as including an “AI transition,” and the quarter’s commentary on improved e-commerce economics and business mix fits that narrative: the tech isn’t just for show; it’s being used to drive efficiency, conversion, and fulfillment productivity. The lack of a flashy AI monetization line item is fine—Walmart’s AI ROI shows up in gross margin basis points and delivery economics, not in an “AI revenue” slide.

Finally, capital returns were a bright spot and an underappreciated part of the story given the guidance headline. Walmart authorized a new $30B share repurchase program and increased the annual dividend to $0.99 per share. The company generated $41.6B of operating cash flow and $14.9B of free cash flow, and it ended the quarter with $10.7B in cash against $51.5B of total debt. If management is going to be conservative on EPS guidance, pairing that caution with a large buyback authorization is a clear “we still like our own cash-generation profile” signal.

Bottom line: Walmart’s quarter validated the core thesis—share gains, strong digital growth, accelerating advertising, and improving e-commerce economics—across Walmart U.S., Sam’s, and International. The stock is down because the market wanted confident, upside-tilted guidance, and Walmart delivered a deliberately cautious outlook with visible headwinds (higher interest expense, continued investment spend, and tariff/inflation uncertainty) outweighing the quarter’s clean execution. If you’re looking for the swing factor from here, it’s whether advertising and e-commerce profitability keep improving fast enough to offset cost pressures and a more guarded macro setup—because the revenue engine is still doing its job.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet