Walmart’s Beat Sparks a Rebound — But Is This the Start of a Rally Back to All-Time Highs?

Walmart delivered a solid Q3 FY26 performance that showcased steady consumer demand, strengthening eCommerce capabilities, and accelerating advertising momentum, even as tariffs drove a noticeable uptick in general merchandise inflation. Revenue and EPS topped expectations, and management raised its full-year guidance across both net sales and operating income. Yet despite the clean headline numbers, shares initially slipped to $98 before rebounding back above the key $100 psychological level—a reflection of the recent downward trend in WMT’s stock and the market’s heightened sensitivity to consumer-related names. The question now is whether this report is strong enough to shake off the recent pullback and set the stage for a retest of the all-time highs.

Walmart reported Q3 revenue of $179.5 billion, beating the $177.4 billion consensus. U.S. comparable sales rose 4.5% (ex-fuel), ahead of the 3.8% forecast, while adjusted EPS of $0.62 topped estimates by two cents. eCommerce remained a standout, growing 27% globally and 28% in Walmart U.S., contributing roughly 440 basis points to U.S. comp growth and underscoring Walmart’s structural shift toward a higher-mix digital model. These results reaffirm the company’s position as the dominant value-and-convenience retailer at a time when macro conditions remain uneven and discretionary spending trends continue to shift.

A major theme in the quarter was tariff-driven inflation. Walmart U.S. like-for-like inflation accelerated to 1.3% (from 1.1% in Q2), with general merchandise inflation rising 170 bps YoY—a 200 bp sequential acceleration—driven largely by tariff-related cost pressures. Grocery inflation eased modestly to 1.3% (from 1.5%), but general merchandise is where tariffs visibly hit. That dynamic matters: Walmart customers have been gravitating toward grocery and essentials for several quarters, and rising ticket sizes have been more volume-driven than price-driven. With tariffs pushing general merchandise prices higher, Walmart saw further mix-shifts into its core food categories, where margins are thinner but volume consistency is stronger.

Despite this backdrop, U.S. gross margins improved modestly thanks to mix gains, marketplace growth, and supply-chain efficiency. The company also cited improved profitability in eCommerce—something that has historically weighed on margins. This suggests Walmart is not only absorbing tariff pressures but also using its scale and EDLP strategy to maintain customer loyalty. The acceleration in grocery share gains reinforces the point: consumers continue to consolidate spending at Walmart, particularly middle-income households seeking value.

Sam’s Club delivered another solid quarter, with 3.8% ex-fuel comp growth, driven by traffic gains and strong membership income. The club channel continues to shine in a higher-inflation environment, and Sam’s performance compares favorably with Costco's recent reports, where traffic growth remained strong but gasoline price normalization weighed on comps. Walmart International posted 10.8% growth (+11.4% in constant currency), with Flipkart, China, and Walmex delivering standout results. The PhonePe share-based compensation charge weighed on reported operating income, but on an adjusted basis International operating income rose nearly 17% in constant currency.

One of the most important—and structurally bullish—drivers of Walmart’s margin story is advertising. Global ad revenue surged 53% (including VIZIO), with Walmart Connect U.S. up 33% and Flipkart ads up 34% during Big Billion Days. Advertising continues to transform Walmart into a higher-margin, tech-powered retailer, mirroring trends seen at Amazon, where advertising is now one of the most profitable revenue streams. Investors increasingly view Walmart’s retail media network as a key strategic asset, particularly as consumer behavior shifts online and third-party marketplace growth accelerates.

AI was not broken out explicitly in the release, but its fingerprints are everywhere: faster delivery speeds, improved inventory optimization, and better ad targeting all depend on AI-powered logistics, forecasting, and personalization engines. Walmart’s marketplace growth, improved eCommerce margins, and 70% growth in expedited delivery fulfillment strongly imply continued returns from its automation and AI investments. This echoes comments from Amazon’s last quarter, where AI-enhanced fulfillment tipped the eCommerce unit into margin expansion.

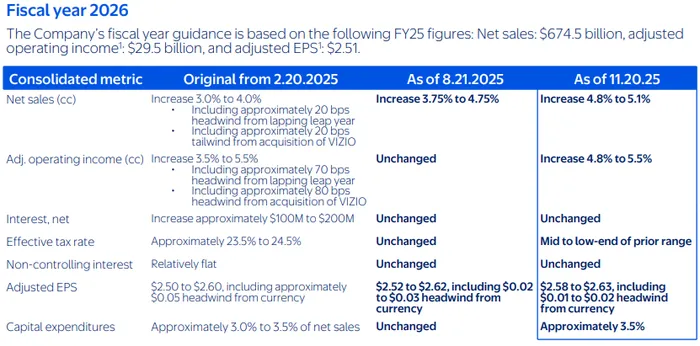

Guidance was another bright spot. Walmart raised its FY26 net sales outlook to 4.8–5.1% growth (cc), up from 3.75–4.75%, and expects adjusted operating income to grow 4.8–5.5% (cc). Adjusted EPS is now expected to land between $2.58 and $2.63, roughly in line with consensus at the midpoint. The reiteration of modest FX headwinds and the clear upward revision in underlying growth assumptions suggest management sees no material consumer pullback—something retailers like Target and Dollar General have been more cautious about. Walmart’s ability to raise guidance despite tariff-driven cost inflation stands in contrast to some peers: Target has been dealing with weaker discretionary demand, Dollar Tree continues to experience margin pressures from shrink and freight, and even Costco’s general merchandise sales have shown softness relative to food and sundries.

On the stock side, the immediate post-earnings reaction was choppy. Shares briefly slipped to $98 before stabilizing back above $100. This volatility is partially due to Walmart’s recent downward trend—uncharacteristic for the stock, which has been one of the most stable large-cap consumer names. The reaction also reflects broader concerns around tariff-driven inflation, discretionary softness, and the still-uncertain holiday spending backdrop. But the rebound off $98 suggests buyers are willing to defend the stock at the century mark. A sustained push back toward the $105–$107 zone would signal that the market is ready to give Walmart credit for its accelerating eCommerce, strengthened guidance, and resilient customer traffic. Beyond that, any attempt to revisit the all-time highs will depend on whether consumers maintain spending momentum into December and how tariffs impact general merchandise elasticity.

Overall, Walmart’s Q3 delivered a steady, strategically constructive quarter: strong comps, rising traffic, margin stability despite tariffs, booming advertising growth, and higher guidance. It wasn’t a blowout quarter like Nvidia’s or Amazon’s, but it was the kind of durable, broad-based performance that reinforces Walmart’s position as the most reliable retail operator heading into year-end. If shares can hold the $100 level and shake off the recent downtrend, this earnings report could serve as the catalyst that re-anchors the long-term bull case.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet