Wall Street Valuations Peak, Global Investors turn to China

U.S. stocks are expensive, but global capital is quietly shifting to China. Is this the start of the next big bull market?

Multiple widely recognized valuation metrics show that the U.S. equity market is not only expensive but has reached extreme levels of overvaluation.

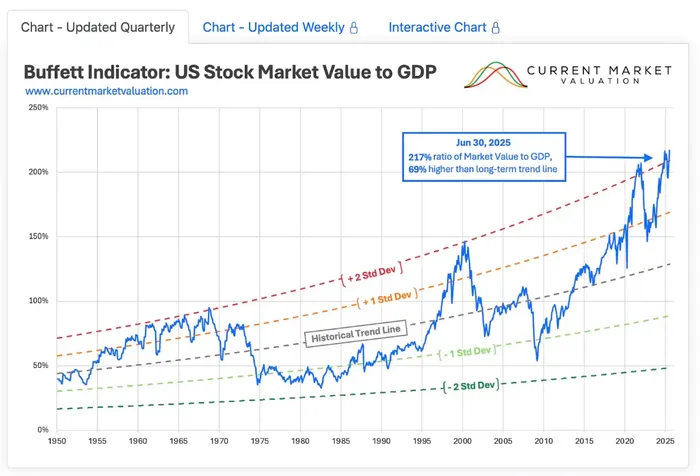

Buffett Indicator: This metric measures the ratio of total market capitalization to GDP. It currently stands at about 200%, more than two standard deviations above its long-term average. Historically, such levels were only seen at the peak of the 2000 dot-com bubble and late 2021, both followed by significant market corrections.

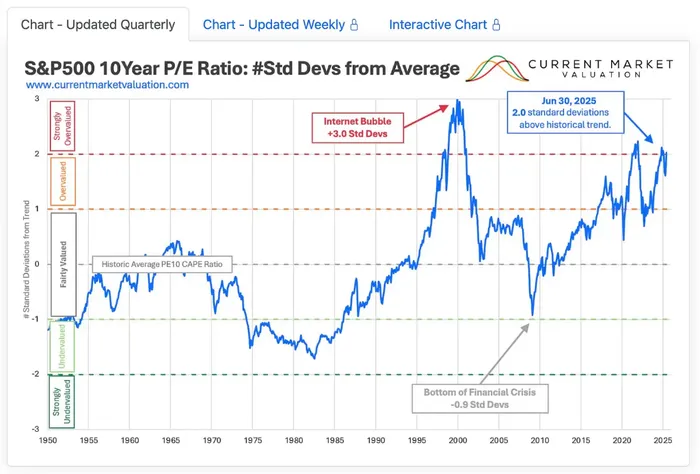

CAPE Ratio: The cyclically adjusted P/E ratio now hovers around 35x, also more than two standard deviations above the historical mean. This range has previously only been reached in 1929 and 2000, both bubble periods—and we all know what followed.

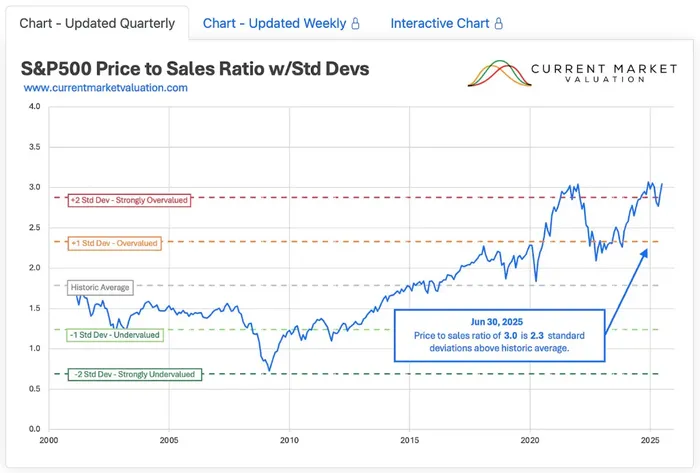

Price-to-Sales Ratio: This indicator has deviated from its trendline by over two standard deviations. Historically, only in 2021 did valuations reach this level, after which the market experienced a steep correction.

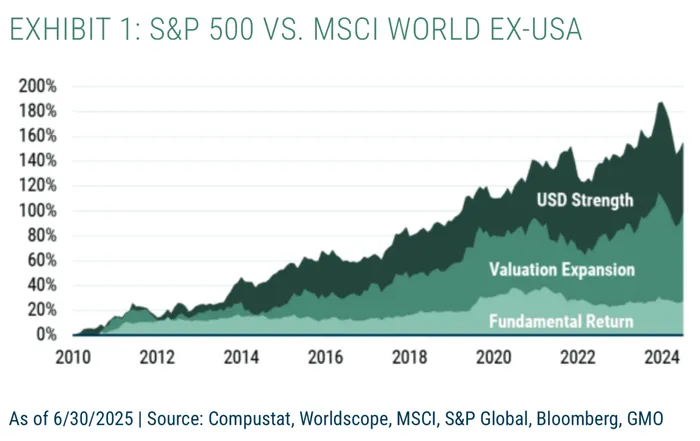

According to asset manager GMO, since 2010 the S&P 500 has outperformed the MSCIMSCI-- ex-U.S. index by a cumulative 150%. Yet about 80% of that excess return came from valuation expansion and dollar strength.

Stripping those out, the U.S. fundamental return advantage is not significant. Since the end of 2019, U.S. equities’ fundamental outperformance has been virtually zero.

GMO argues that the two drivers of past returns are unlikely to repeat. U.S. valuations are already at record highs, which typically suppress future returns. The dollar is also unlikely to weaken sharply.

As such, the stellar performance of U.S. equities over the past 15 years may not recur.

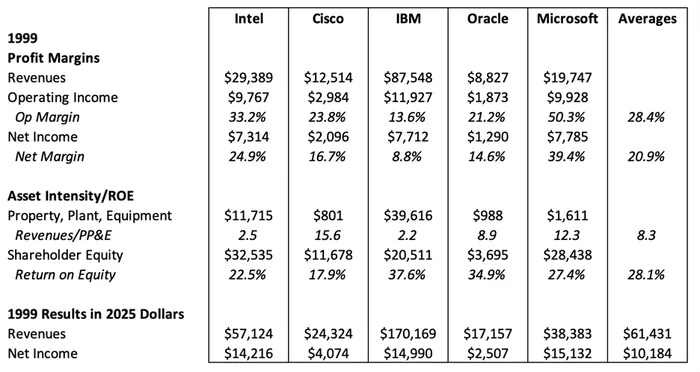

Of course, one cannot simply draw static comparisons. Comparing the top five tech giants of 2025 with those of 1999, today’s giants boast 4.6x higher average revenue and 9.1x higher net income.

In 2025, their average net margin is 34.2%, compared to 20.9% in 1999—64% higher. ROE is a dramatic 66.5% versus 28.1%. This means there is some justification for today’s higher valuation base.

Nonetheless, given that U.S. valuations are at historical highs, investors should lower their return expectations going forward.

Looking at past cycles, U.S. bull markets typically last about four years. We are currently in year 2.5.

_a0dfb9f81757688501303.png?format=webp&width=700)

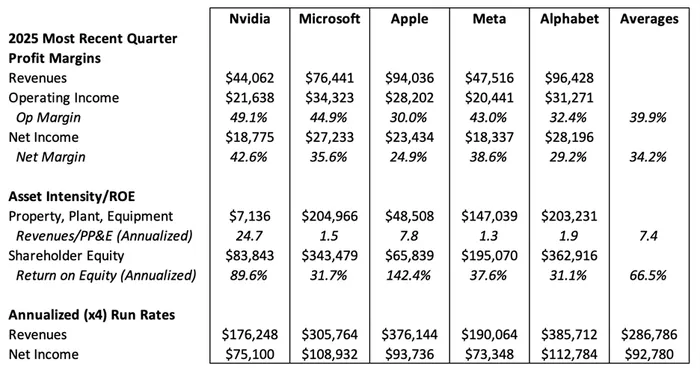

With U.S. equities highly valued, international investors are shifting to Chinese assets. According to IIF data, in August foreign investors poured $44.8 billion net into emerging market portfolios, the highest in nearly a year.

China attracted $39 billion in combined equity and bond inflows, accounting for the vast majority of the total.

By contrast, ex-China EM equities saw a $7.4 billion outflow, ending a three-month streak of inflows.

In August, Chinese equities are on track to post the largest monthly hedge fund inflows in history.

_55a7cbf31757688571334.png?format=webp&width=700)

Next, let’s examine today’s hottest AI-related charts.

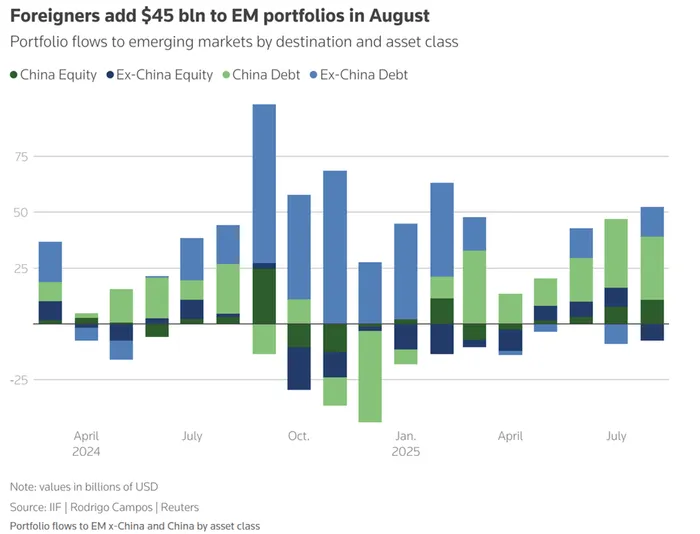

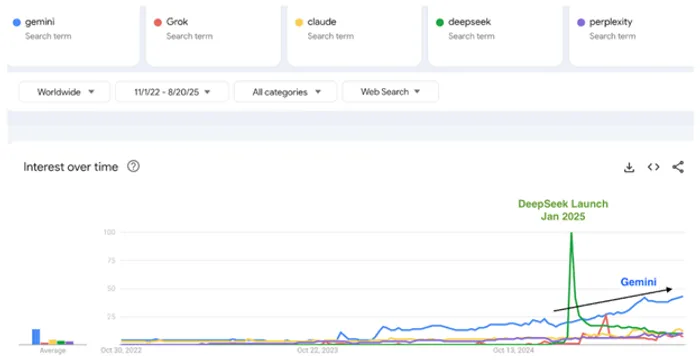

The success of any disruptive technology depends on mass adoption, and GoogleGOOGL-- Trends is a useful gauge of usage.

Since its launch in November 2022, “ChatGPT” has dominated Google search interest, far outpacing other large models. Entering 2025, ChatGPT search volumes appear to be accelerating upward.

Besides ChatGPT, xAI’s Grok, Google’s Gemini, Anthropic’s Claude, and China’s DeepSeek are among the leading models, but their search popularity is far below GPT’s.

Google’s Gemini (blue line) is the second most searched chatbot after ChatGPT, with a steady upward trend.

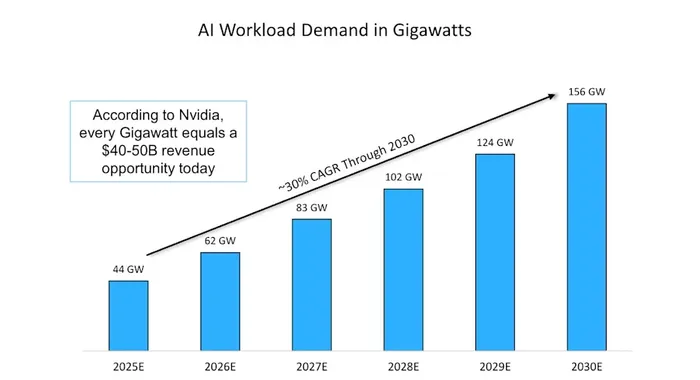

By 2030, AI-related energy demand is projected to grow at a compound annual rate of 30%, reaching 156 GW by year-end 2030.

According to Melius Research analyst Ben Reitzes, each gigawatt of AI workload could translate into $40–50 billion of revenue for NvidiaNVDA--.

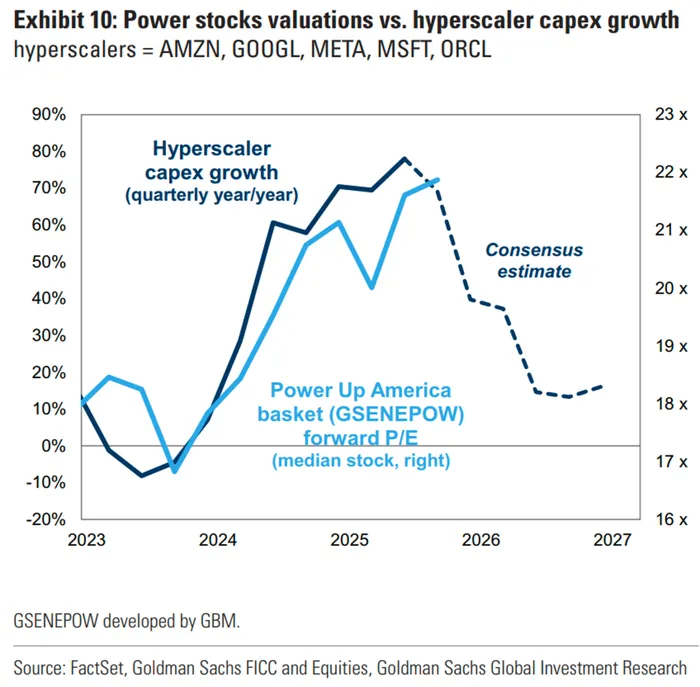

Fueled by strong Capex from giants like AmazonAMZN-- and Google, the median forward P/E of U.S. utility stocks has expanded from 17x in early 2024 to 22x today.

However, consensus estimates show Capex growth will sharply slow by Q4 2025 and into 2026.

Although power contracts are signed with a lag, the slowdown in Capex growth may lead investors to reassess lofty valuations of AI infrastructure-related stocks.

Finally, let’s look at other charts.

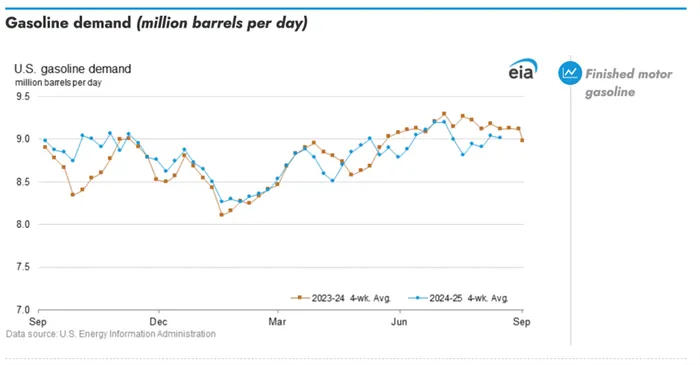

U.S. gasoline demand is a proxy for consumer spending. The chart compares daily gasoline demand from 2023–2024 (brown line) with 2024–2025 (blue line).

When the blue line is above/below the brown line, demand is higher/lower than the same period last year.

Given the large U.S. vehicle fleet, still dominated by internal combustion cars, EV impact is negligible.

Since early July, U.S. gasoline demand has fallen year-on-year, signaling cautious consumer behavior in travel and discretionary spending.

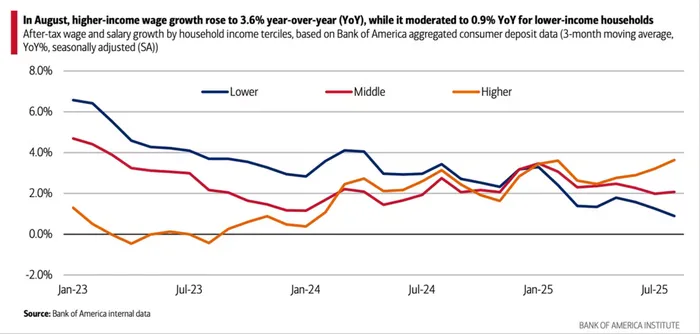

Bank of America data shows America’s “K-shaped” economic divergence worsened in August: after-tax wages for high-income households grew 3.6% YoY, the fastest since November 2021; but for low-income households, growth slowed to 0.9%, the weakest since 2016.

This divergence also shows in spending patterns: high-income groups are accelerating credit/debit card use, while low-income groups are slowing.

From a macro perspective, since the top 40% of earners account for over 60% of consumption, their growth is enough to offset lower-income weakness, sustaining overall consumption.

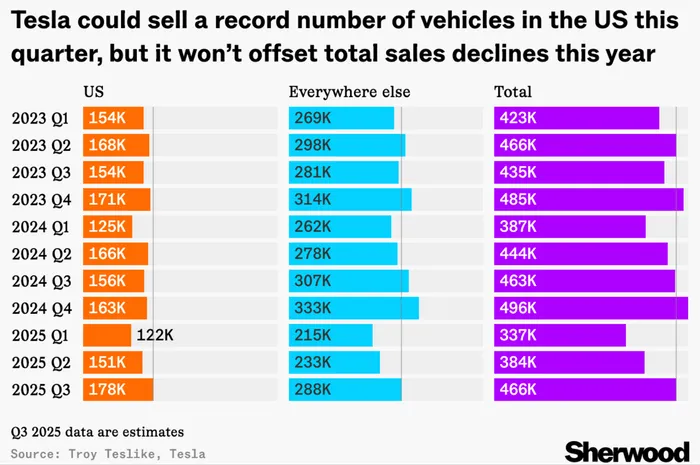

Analysts expect Tesla’s U.S. Q3 2025 sales to hit a record 178,000 units, but this won’t reverse its full-year decline. The Q3 surge mainly reflects buyers rushing ahead of EV tax credit expirations, which will depress Q4 sales.

Overall, analysts forecast Tesla’s 2025 global deliveries at about 1.6 million units, down 9% year-on-year.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO