Wall Street Outlook for 2026: A Bumpier Road Ahead as the AI-Led Cycle Endures and Policy Distortions Linger

By the time investors turn the page to 2026, one reality is hard to ignore: this is no longer a "clean" cycle. After three consecutive years of double-digit returns, the stock market is due for a reality check. Does AI truly deserve such a high premium, or could bubble concerns loom further ahead? Against that backdrop, the most striking commonality across JPMorganJPM--, Morgan StanleyMS--, Goldman SachsGS--, and CitiC-- is not optimism or caution per se, but nuance. The U.S. economy is slowing, yet far from stalling. Equities look expensive, yet not unmoored from fundamentals. AI is powerful, yet increasingly fragile as a single pillar of confidence.

What makes 2026 particularly challenging is that the baseline is relatively benign, while the alternative paths are unusually wide. As JPMorgan puts it, "while a baseline forecast is relatively easy to construct, it is the alternative scenarios that deserve the most attention." That framing captures the moment well. Growth, inflation, and earnings may all behave "well enough" on average—but the ride there is unlikely to be smooth.

The U.S. Economy: Slower, Constrained, but Still Standing

At the macro level, the U.S. economy enters 2026 with less momentum than headline asset prices might suggest. Tariffs, immigration restrictions, and a maturing AI investment cycle are all exerting drag. Yet none, on their own, appear sufficient to tip the economy into recession.

JPMorgan's base case sketches a distinctive rhythm: real GDP growth slows toward a roughly 1% pace by late 2025, rebounds above 3% in the first half of 2026, and then fades again to a 1–2% range as temporary fiscal supports wane. That rebound is not driven by a classic cyclical upswing, but by timing effects—most notably tax refunds linked to the One Big Beautiful Bill Act (OBBBA), which are expected to arrive in early 2026 due to delayed IRS withholding adjustments.

Citi, looking at the global picture, strikes a similar tone of resilience without acceleration. Global growth around 2.7% is hardly inspiring, but after four years of repeatedly defying pessimistic forecasts, it carries a quiet credibility. Purchasing managers' indexes reinforce the message: services-heavy economies like the U.S. continue to outperform, while manufacturing-intensive regions lag. Perhaps more tellingly, PMIs have shown "little imprint from the Trump administration's tariffs," suggesting adaptation rather than breakdown.

The real constraint on U.S. growth is not demand, but supply—specifically labor. Immigration restrictions loom large here. JPMorgan notes that net immigration appears to have fallen sharply enough to trigger an outright decline in the working-age population, a development that would have been almost unthinkable a decade ago. Even if participation rates rise, labor supply remains tight. The result is an unusual combination: very slow job growth, yet only a modest increase in unemployment.

In this framework, monthly payroll gains of roughly 50,000 are consistent with an unemployment rate peaking around 4.5% and then stabilizing. That dynamic caps GDP growth, but also limits the risk of mass layoffs. GoldmanGS-- Sachs echoes this view, arguing that labor-market weakness—driven by immigration limits, federal layoffs, and labor-saving AI—should keep inflation pressures contained, even if growth softens further.

Inflation, Tariffs, and the Fed's Narrow Path

Inflation remains the most delicate variable in the 2026 outlook, not because it is expected to surge, but because it constrains policy flexibility. Tariffs are central to this story. JPMorgan estimates that dramatic increases in U.S. tariffs generated more than $29 billion per month in revenue between June and October, with much of the cost initially absorbed by retailers. That absorption phase is ending.

As tariff costs are increasingly passed through to consumers in late 2025 and early 2026, year-over-year inflation is expected to rise through mid-2026. Even so, JPMorgan expects CPI inflation to peak below 4%, helped by lower oil prices and easing shelter inflation, before falling back toward 2% by year-end. Citi's analysis reinforces the idea that tariffs have acted as a one-off supply shock for the U.S., rather than a persistent inflation engine.

This matters enormously for the Federal Reserve. Goldman Sachs frames the labor market as the key: "We believe the labor market holds the key to the pace and scale of Fed easing into 2026, so long as inflation remains anchored." If labor weakness persists and tariff-driven inflation proves transitory, additional rate cuts become plausible—even likely.

Morgan Stanley leans into this interpretation more forcefully. They argue that fiscal policy, monetary policy, and deregulation are now aligned in a way "that rarely happens outside of a recession." That alignment allows markets to shift focus away from macro fear toward asset-specific narratives, particularly AI. In their view, rate cuts in 2026 are not a rescue operation, but a late acknowledgment that policy has remained too restrictive for too long.

Citi, however, remains more skeptical of a strong reacceleration. While Fed cuts are likely, they see limited upside in aggregate investment, noting that some of the strength in 2025 reflected front-loading ahead of tariffs and a reallocation toward AI-related projects rather than a broad-based capex boom.

U.S. Equities: Expensive, but Still Earnings-Driven

Few topics generate as much debate as U.S. equity valuations. A third consecutive year of double-digit gains naturally invites bubble rhetoric. Yet across the banks, there is a shared reluctance to frame the current market as irrational.

JPMorgan poses the question directly: "Are stocks too expensive?" Valuations are undeniably rich, but the justification lies in earnings. Four consecutive quarters of double-digit profit growth, achieved despite policy rates above 4%, a softer consumer, and fewer cyclical tailwinds, are difficult to dismiss. Structural changes—such as the index's shift toward high-margin growth sectors—also argue for higher multiples than historical averages might suggest.

Morgan Stanley is the most bullish of the group, projecting the S&P 500 to reach 7,800 over the next 12 months. Their confidence rests on earnings growth, tax relief from the OBBBA, AI-driven efficiency gains, and eventual Fed easing. From their perspective, the market has already endured a quiet cleansing. As Mike Wilson notes, by April the S&P 500 had been down 20% from peak, while the average stock was down more than 30%. That, in their telling, marked the end of a rolling recession—and the beginning of a new bull market.

Goldman Sachs offers a cooler assessment. Market concentration is extreme—the top 10 stocks account for roughly 40% of S&P 500 market cap—but history suggests such dominance can persist for decades without triggering crisis. The greater risk, in their view, is earnings disappointment rather than valuation compression. If profits fail to meet elevated expectations, today's multiples become harder to defend.

Citi sits somewhere in between. They see the S&P 500 reaching 6,900 by mid-2026 and expect a choppier phase of the bull market. Still, they remain constructive over the medium term, pointing to Fed cuts, earnings broadening, and continued support for the AI trade as key pillars.

AI: Structural Transition, Not a Classic Bubble

If there is one theme that binds all four outlooks together, it is AI. Importantly, none of the banks describe AI as a traditional bubble. Yet none are complacent either.

JPMorgan's characterization is particularly apt: "Bubbles burst into nothing, but the AI theme is building real infrastructure." Data center capex already amounts to roughly 1.2–1.3% of GDP, and business adoption is accelerating. AI spending is translating into real demand for chips, cloud services, and software, lending credibility to the investment cycle.

Morgan Stanley underscores the scale still ahead. Of an estimated $3 trillion in data-center-related capex, less than 20% has been deployed. That implies sustained investment well into 2026 and beyond—but also rising financing needs. Increased debt issuance by the tech sector is expected to widen investment-grade spreads, introducing stress into parts of the credit market even as equity narratives remain upbeat.

Goldman Sachs emphasizes durability. Hyperscalers have repeatedly exceeded AI capex expectations and have largely financed investment internally. Still, reliance on debt is increasing, making balance-sheet quality more important than ever. Citi, meanwhile, flags AI as both a key upside driver and a non-trivial downside risk. Adoption will not be linear, and valuation setbacks are possible even if the long-term productivity story remains intact.

Perhaps the most important takeaway is that AI is no longer optional for markets. Tech sectors account for an outsized share of earnings and capex growth. That makes the broader market more sensitive to any stumble—be it power constraints, hardware obsolescence, or slower-than-expected monetization.

Beyond Equities: Rates, FX, and Commodities

Outside equities, the outlook becomes more fragmented. In fixed income, Morgan Stanley expects a rally in the first half of 2026 as central banks pivot from inflation control to equilibrium management, followed by a rebound in yields later in the year. Goldman and Citi broadly agree that easing cycles create opportunities across duration, particularly in front-end Treasuries and select credit.

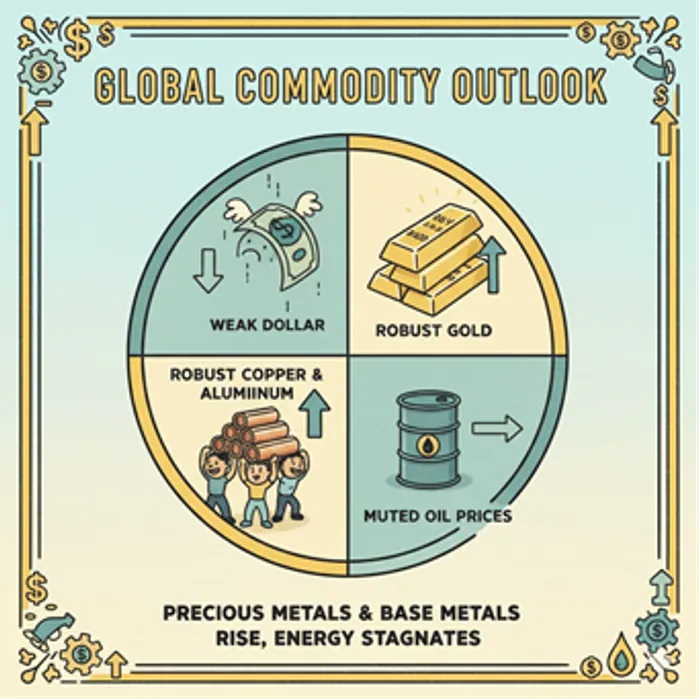

Currency views diverge more sharply. Morgan Stanley expects a choppy U.S. dollar—weakening early in 2026 before rebounding around midyear. Citi, by contrast, maintains an out-of-consensus bullish dollar view, arguing that U.S. reacceleration risks are underpriced and that much of the good news is already reflected in the euro.

In commodities, oil is the least controversial call. Most expect prices to hover around $60, with OPEC+ acting as a backstop against collapse. Gold is more divisive. Goldman and Morgan Stanley see support from rate cuts and physical demand, while Citi questions upside from elevated levels, framing gold as a tough call rather than a conviction trade. On base metals, enthusiasm is broader: copper and aluminum benefit from both AI-related power demand and the energy transition.

The Takeaway: Manage the Range, Not Just the Mean

Across these four institutions, the message is consistent in spirit if not in detail. The U.S. economy in 2026 is likely to slow, but not crack. Inflation should ease, but policy distortions—from tariffs to immigration—will linger. Equities may continue higher, but with greater volatility and less tolerance for disappointment. AI remains a structural force, but also a source of fragility as expectations race ahead of visibility.

Perhaps the most useful insight comes from JPMorgan's closing thought: after a modest surge in growth and inflation, both "slowly slide to subdued levels by the end of 2026." That is not a bearish conclusion—but it is a warning. The era of effortless upside is likely behind us. What replaces it is a market that rewards selectivity, balance, and an appreciation for how quickly sentiment can shift when narratives meet constraints.

In that sense, 2026 is less about predicting a single outcome than about respecting the width of the path. The baseline may be calm, but the edges are sharp—and the journey there is unlikely to be smooth.

Crypto market researcher and content strategist with 3 years of experience in digital asset analysis and market commentary. Skilled at transforming complex blockchain data and trading signals into clear, actionable insights for investors. Experienced in covering Bitcoin, Ethereum, and emerging ecosystems including DeFi, Layer2, and AI-related projects. Passionate about bridging professional market research with accessible storytelling to empower readers and investors in the fast-evolving crypto landscape.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet