The Volatile Dance of Mortgage Rates: Navigating Housing Investment Amid Fannie Mae's Shifts

The housing market's future is once again clouded by uncertainty as Fannie Mae's recent revisions to mortgage rate forecasts reveal a tug-of-war between optimism and caution. What began as a May outlook suggesting declining rates has now morphed into a June warning of higher borrowing costs, leaving investors, homebuyers, and mortgage-backed securities (MBS) holders scrambling to recalibrate strategies. The implications are profound: shifts in mortgage rates directly influence affordability, home sales, and the valuation of real estate assets. For investors, the path forward demands a nuanced understanding of these dynamics.

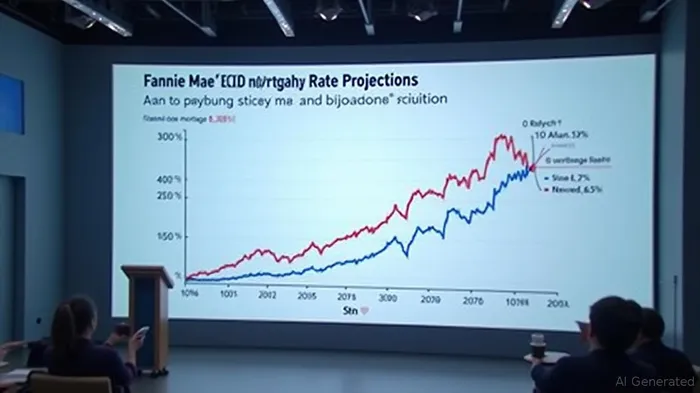

The Rate Revisions: A Tale of Two Forecasts

In May, Fannie Mae projected a modest decline in the 30-year fixed-rate mortgage to 6.1% by year-end 2025, buoyed by expectations of easing inflation and gradual economic cooling. This optimism fueled a revised forecast of 4.92 million home sales for 2025—a 60,000-unit increase from prior estimates. The logic was straightforward: lower rates would spark refinancing and boost purchase demand, particularly among first-time buyers squeezed by earlier high rates.

But by June, the narrative shifted. New economic data, including stubbornly sticky inflation and resilient wage growth, prompted Fannie Mae to raise its year-end 2025 rate forecast to 6.5%, with 2026 expectations inching down to 6.1%. The revised sales forecast now sits at 4.82 million units—a retreat from May's optimism. The message is clear: the Fed's path is uncertain, and mortgage rates remain hostage to inflation's whims.

Implications for Real Estate Investors

The seesaw in rate projections creates both opportunities and risks. Residential real estate stands to benefit if rates stabilize below 6.5%, as affordability improves and sales rebound. However, persistent inflation or a Fed policy surprise could prolong elevated rates, dampening demand. Investors in REITs, which often correlate with interest rates, face a dual challenge: lower rates might boost property values but also raise REIT borrowing costs. Conversely, higher rates could pressure occupancy rates but reduce competition for acquisitions.

The MBS market, meanwhile, is acutely sensitive to these shifts. When rates rise, MBS prices fall, but prepayment risk diminishes (as fewer borrowers refinance). The June revision suggests investors in MBS should focus on shorter-duration securities to mitigate interest rate risk. However, if rates dip back below 6%, refinancing could surge, reducing the value of older MBS holdings.

Data-Driven Insights

The data underscores how rates have become a key battleground. Since hitting a 20-year high of 7.08% in November 2022, the 30-year rate has oscillated between 6.5% and 7.0%, reflecting Fed policy and market speculation. Fannie Mae's June forecast now places 2025 rates at the upper end of this range, implying limited relief for borrowers.

Meanwhile, mortgage originations—a proxy for refinancing activity—are projected to grow to $1.99 trillion in 2025, up slightly from 2024 but still below pre-2022 levels. This suggests a market still grappling with elevated borrowing costs, even as Fannie's June forecast hints at a slower-than-expected retreat from high rates.

The Fed's Role in the Rate Outlook

Fannie Mae's revisions are inextricably tied to Federal Reserve policy. The central bank's pause at 5.50% since May 2023 has created ambiguity: will the Fed hike again, or cut? The June report assumes no rate cuts by year-end, a stance consistent with core inflation hovering near 3.8% in 2025. If the Fed remains patient, mortgage rates may edge lower in 2026. But if inflation surprises upward, rates could rise further, derailing housing recovery.

Actionable Investment Strategies

- For Residential Real Estate:

- Buy: Target markets with strong job growth and rental demand, such as tech hubs or energy-driven regions, where price declines have been modest.

Avoid: Overvalued coastal markets where price corrections are still underway.

For REITs:

- Focus: On diversified REITs with low leverage and exposure to essential sectors like industrial or healthcare.

Avoid: Residential-focused REITs reliant on refinancing, which could face rising borrowing costs.

For MBS Investors:

- Opt for: Shorter-duration MBS to limit interest rate risk.

Monitor: Prepayment speeds—if rates dip below 6%, consider hedging via interest rate swaps.

Hedging Against Rate Volatility:

- Pair long positions in real estate ETFs (e.g., IYR) with short positions in interest rate futures to offset rate-related risks.

Conclusion: Navigating the Crosscurrents

Fannie Mae's revised forecasts highlight the precarious balance between economic resilience and policy uncertainty. For investors, the key is to remain agile, prioritizing liquidity and diversification. While the June revision signals caution, the market's ultimate direction will hinge on inflation's trajectory and the Fed's next move. In this environment, portfolios should favor assets that thrive in low-rate scenarios while maintaining flexibility to pivot as new data emerges. The housing market's future is no longer a straight line—it's a winding path where preparedness is paramount.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet