Vale Stock Gains 48% in a Year: Should You Buy, Sell or Hold?

Vale S.A. VALE stock has gained 47.9% in a year, beating the industry’s 44% growth, the broader Zacks Basic Materials sector’s 33.4% gain and the S&P 500’s 21.5% rise.

It has also outpaced peers such as Rio Tinto RIO, BHP Group BHP and Fortescue Ltd FSUGY, which have gained 40.1%, 39.1% and 33.6%, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Vale is trading at a forward 12-month price/sales multiple of 1.65X, lower than the industry’s 1.79X. It also remains more attractively valued than Rio Tinto, Fortescue and BHP, which trade at higher multiples of 1.87X, 2.75X and 3.27X, respectively.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Let us delve deeper into the company’s long-term prospects before assessing whether to buy, hold or sell the stock.

Vale’s Q4 Results Show Strong Volume-Led Performance

VALE delivered solid fourth-quarter results, with net operating revenues rising 9.2% year over year to about $11 billion. The Iron Solutions segment generated $8.4 billion in revenues, up 3%, supported by a 5% increase in volumes and a 3% improvement in realized iron ore fines prices.

The Base Metals segment’s net operating revenues surged 36% year over year to $2.69 billion. Copper revenues gained 62% to $1.57 billion on 9% higher volumes and a 20% rise in average realized prices for copper. Nickel revenues were up 24% year over year to $1.32 billion, attributed to a 5% increase in sales volume and higher byproduct prices that offset the 7% decline in average realized prices.

Vale’s pro-forma adjusted EBITDA was up 17% year over year to $4.8 billion on stronger copper and by-products reference prices and higher sales volumes of iron ore and copper. Proforma EBITDA margin was 43.7% in the fourth quarter compared with 40.7% in the year-ago quarter. Adjusted earnings per share surged 70% to 34 cents.

Vale’s 2025 Production Beats Guidance

Vale’s iron ore production for 2025 was around 336 Mt, higher than its original guidance of 325-335 Mt. Copper output was around 382.4 kt in 2025, also above the guided 340-370 kt. Nickel output was reported at 177.2 kt compared with the company’s original target of 160-175 kt. Iron ore and copper output reached the highest levels since 2018, and nickel production was the strongest since 2022.

VALE’s Projects Support Long-Term Output Growth

The company has budgeted capital expenditure for the Iron Ore Solutions business at $4 billion in 2026 and $3.9 billion from 2027 onward. It plans to increase its iron ore production capacity to 335-345 Mt in 2026 and 360 Mt by 2030.

The Vargem Grande 1 (VGR1) project and the Capanema Maximization project are expected to play a key role in attaining these targets, each expected to add about 15 Mtpy of capacity. Additional initiatives, including Compact Crushing at S11D and Serra Sul, are also set to boost capacity from the second half of 2026.

Vale is also investing heavily in the base metals business to benefit from the global energy transition. It expects to invest $1.6 billion in 2026 and about $2 billion annually from 2027.

In 2026, Vale's copper production is expected to be between 350 kt and 380 kt, and reach 420-500 kt as of 2030 and 700 kt by 2035. This suggests a 7% CAGR during 2024-2035, higher than the 4% peer average. Projects like the Bacaba, Salobo Coarse Particle Flotation, Alemão and Cristalino will aid in this growth.

Vale recently signed an agreement with Glencore Canada (Glencore) to jointly evaluate a potential brownfield copper development project at their adjacent properties in the Sudbury Basin, with an expected start-up in 2030.

For 2026, Vale expects its nickel production to be between 175 kt and 200 kt, reflecting replenishment projects in Canada, exposure to Pomalaa and Morowali, and the start-up of the second furnace at Onça Puma. For 2030, nickel production is anticipated at 210-250 kt, with input from projects such as Thompson Ultramafics, Sorowako HPAL, partnership projects and offtake.

VALE Cost Cuts Strengthen Margin Profile

Vale continues to focus on cost control, with fixed costs reduced to $5.8 billion in 2025 from $6.3 billion a few years ago, and a further decline to $5.7 billion is targeted for 2026. It has managed to lower all-in costs by 3% in its iron business, 77% in the copper business and 27% in the nickel business in 2025, marking the second consecutive year of cost reduction.

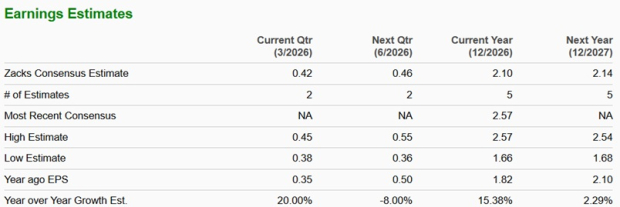

Vale’s Earnings Estimates Trend Higher

The Zacks Consensus Estimate for Vale’s earnings for both fiscal 2026 and fiscal 2027 has moved up over the past 60 days. This is shown in the chart below.

Image Source: Zacks Investment Research

The consensus estimate for Vale’s 2026 earnings is pegged at $2.10 per share, suggesting 15.4% year-over-year growth. The same for 2027 indicates growth of 2.3%.

Image Source: Zacks Investment Research

Vale Offers Sector-Leading Dividend Yield & Returns

The company’s current dividend yield of 4.37% is higher than the sector’s 2.03%. VALE’s return on equity, a profitability measure of how prudently it is utilizing its shareholders’ funds, is 20.16%, higher than the sector’s average of 11.55%.

VALE Faces Operational and Market Risks

VALE has encountered some operational challenges, including pit overflows at the Fábrica and Viga mines earlier this year, which led to temporary suspensions. Vale recently announced that three requests for asset freezes, filed on a preliminary basis and totaling R$ 2.846 billion, have been denied by the respective competent courts. Only one decision remained pending, related to an asset freeze request in the amount of R$ 200 million. The company’s guidance, however, remains unchanged.

Iron ore prices are currently at around $105 per ton, up 3% in a year. However, rising supply from Australia and Brazil, along with new output from projects like Simandou and softer demand from China, could pressure prices going forward.

VALE Stock Outlook: Hold for Now

VALE’s strong production performance, expanding project pipeline, growing base metals exposure and disciplined cost structure underpin its long-term investment case. Existing investors may consider holding the stock to benefit from its growth initiatives, improving earnings outlook and attractive dividend yield.

However, new investors might prefer to wait for greater clarity on iron ore price trends before initiating positions. Vale currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BHP Group Limited Sponsored ADR (BHP): Free Stock Analysis Report

VALE S.A. (VALE): Free Stock Analysis Report

Rio Tinto PLC (RIO): Free Stock Analysis Report

Fortescue Ltd. Sponsored ADR (FSUGY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet