Unraveling $4 Trillion Stock Crash: Tariff Turbulence & Market Mayhem

On Monday, U.S. equities experienced one of the worst trading days of 2025.

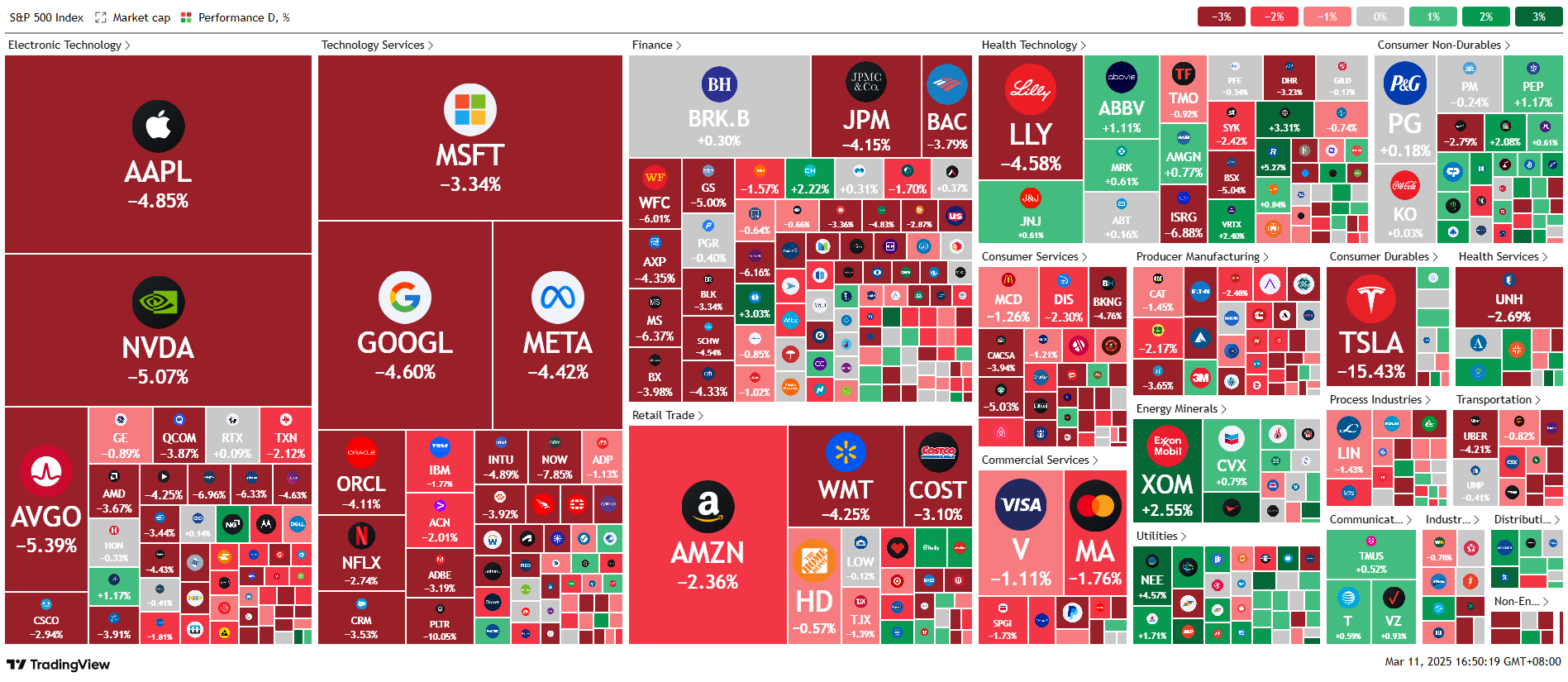

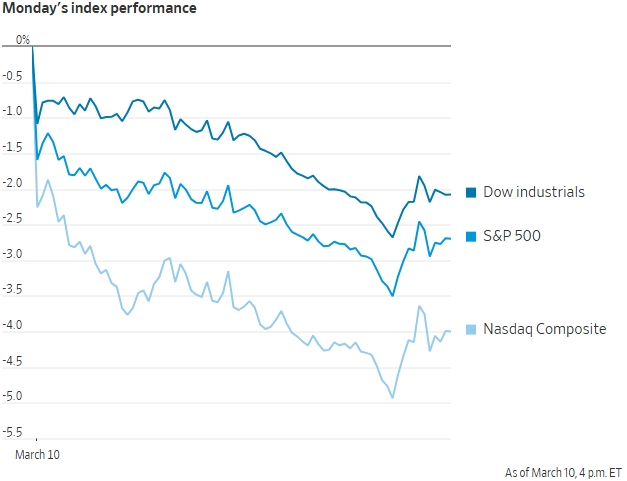

Major indexes fell sharply, with the S&P 500 down 2.7% from 5770.20 to 5614.56, (a loss of approximately $1.3 trillion in market value in a single day), the NASDAQ Composite sliding 4% (its worst single-day decline since September 2022), and the Dow Jones Industrial Average dropping over 2%, as investors grappled with a cocktail of tariff uncertainty, recession fears, and profit-taking after a prolonged period of high valuations.

The selloff wiped out trillions of dollars in market value and sent volatility indexes soaring, signaling a sudden shift in investor sentiment. Here's the in-depth analyze on what caused this free-fall.

Tariff-Driven Uncertainty

A major catalyst behind the downturn has been the renewed imposition of aggressive tariffs by the Trump administration. Market participants have been rattled by conflicting signals on trade policy, especially amid tariffs on key trading partners such as Canada, Mexico, and China.

The radical policy itself paired with rapid policy shifts and back-and-forth moves have led many to question the long-term impact on both domestic earnings and global supply chains. According to analysts, the huge amount of uncertainties created by the tariff wars are causing boards and C-suites to reconsider the pathway, both policy wise and financial wise, forward.

Recession Fears and Economic Policy

Investors' concerns have deepened with President Trump's ambiguous comments regarding the possibility of a recession during a recent interview with FOX news.

When questioned about his outlook, Trump acknowledged a "period of transition," a remark that many interpreted as tacit acceptance of short-term pain for longer-term gains. Analysts noted that the Trump administration are signaling a highly likelihood that they are willing to accept short-term market suffering and even a recession.

This lack of clear reassurance has compounded worries over a slowing economy, with major banks downgrading their growth forecasts and signaling increased risks of recession.

According to the US Bureau of Economic Analysis, Economic data further fueled the sell-off:

1. GDP Growth Slows: The U.S. Bureau of Economic Analysis reported third-quarter GDP growth at 2.8%, down from 3.0% in the prior quarter and below the 3.1% economists had forecasted. This slowdown, driven by weakening consumer spending and declining business investment, heightened fears of an economic slowdown.

2. Persistent Inflation: The PCE index, the Federal Reserve's preferred inflation measure, rose to 2.6% year-over-year, with core PCE (excluding food and energy) climbing to 2.9%. Both figures remain well above the Fed's 2% target, suggesting that inflationary pressures persist. This raised expectations of continued monetary tightening, unsettling markets.

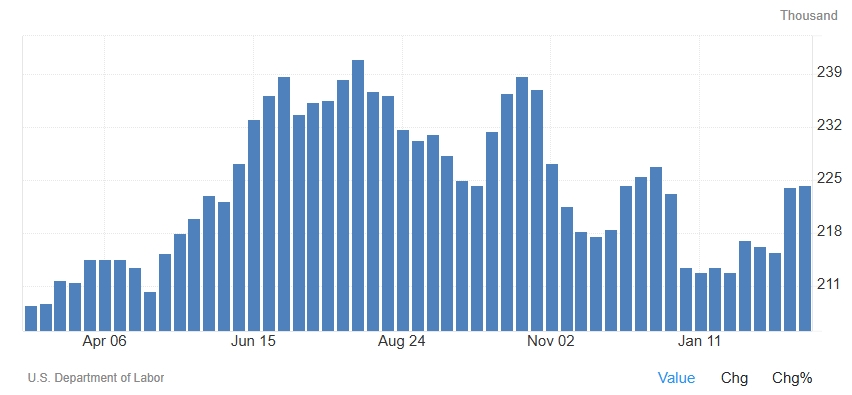

3. Rising Jobless Claims: The Labor Department reported initial jobless claims increased to 224,000, up from 212,000 the previous month and exceeding the 220,000 anticipated by analysts. While still modest, this uptick hinted at a softening labor market, amplifying recession concerns.

These economic signals—slower growth, stubborn inflation, and a weakening jobs picture—created a backdrop of uncertainty, prompting investors to reassess their optimism about the economy's trajectory.

Technical Factors and Market Sentiment

Beyond policy, technical factors have played a role in Monday's crash. After a prolonged period of overvaluation, particularly in tech stocks that have enjoyed soaring gains in recent years.

In the weeks leading up to March 10, investors had grown increasingly risk-averse, as evidenced by the Cboe VIX spiking to around 30, its highest level since the global markets rout in early August. The market correction appears to have been inevitable. Profit-taking, driven by rapid swings in sentiment, forced a sharp rebalancing.

Declining Treasury yields, with the 10-year Treasury yield dropping 9 basis points to 4.225% and the 2-year yield falling 8 basis points to 3.921%, further underscored the market's flight from risk, reinforcing a sense of widespread uncertainty.

Geopolitical Tensions: Global Uncertainty Rises

Geopolitical developments further rattled markets, amplifying fears of economic disruption on a global scale.

1. Middle East Conflict: Escalating tensions in the Israel-Hamas conflict, with reports of Iran bolstering support for proxy groups, sparked concerns of a broader regional war and stoking inflation fears and adding pressure on energy-sensitive sectors.

2. U.S.-China Trade Friction: The U.S. imposed new sanctions on Chinese semiconductor firms, prompting China to restrict exports of rare earth minerals essential for tech manufacturing. This escalation has threatened global supply chains and corporate profitability.

These geopolitical risks drove investors toward safe-haven assets like gold and U.S. Treasuries, reflecting heightened market anxiety.

Analysts' Perspectives

Analysts offer a spectrum of interpretations regarding the crash:

Goldman Sachs (David Kostin, Chief U.S. Equity Strategist): Kostin attributed the market's weakness to tariff-related uncertainties and disappointing economic data. He warned that without a resolution to trade disputes, the S&P 500 could face further downside risks.

Morgan Stanley (Mike Wilson, Chief Investment Officer): Previously cautiously optimistic, Wilson revised his outlook. Citing the GDPNow forecast and tech sector vulnerabilities, he predicted a potential 10-15% correction amid heightened volatility.

JPMorgan Chase Strategist: JPMorgan strategist emphasized algorithmic trading's role in exacerbating the sell-off, arguing that the market's reaction was overblown relative to fundamentals.

Bank of America's Head of Global Research: Head of BOA global research pointed to the Federal Reserve's reluctance to ease monetary policy amid persistent inflation as a key factor weighing on investor sentiment.

Independent Analyst Robert Kiyosaki: Known for contrarian views, Kiyosaki warned of a "cataclysmic decline" due to overvaluation and global challenges, urging investors to seek refuge in gold.

Short-Term vs. Long-Term Viewpoints:

While some market strategists argue that the crash is primarily a short-term correction, driven by overextended valuations and the need for profit-taking, others caution that the policy uncertainty and the underlying fragility of economic fundamentals could lead to further downside. An Analyst from trading firm, commented, "The market is already starting to price in the slowdown, it's too soon to tell if this is the start of a recession" .

The Role of Investor Sentiment:

Many point to the rapid shift in investor sentiment as a key factor. A senior investment strategist observed a "big sentiment shift" where the momentum from growth stocks turned negative almost overnight. This shift, combined with heightened risk aversion, has accelerated the selloff, particularly in the tech sector

Global Spillover and Safe-Haven Demand:

International investors are also reacting. As U.S. markets fell, global equity indexes mirrored the downturn, and investors sought refuge in bonds and other safe assets. This "flight to safety" has been characterized by falling Treasury yields and increased demand for government debt, suggesting that the market is bracing for further economic headwinds.

Conclusion

Monday's stock market crash serves as a stark reminder of the fragility inherent in today's economic environment. With aggressive tariffs, mixed messaging from political leaders, and significant technical corrections converging, the market's descent reflects both short-term recalibration and deeper structural concerns. As investors and analysts continue to digest these developments, the prevailing sentiment is maintaining cautious, with the hope that forthcoming policy clarifications and improved economic indicators might eventually restore confidence.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet